How Quanta’s AI Infrastructure Push and New Utility Deals At Quanta Services (PWR) Has Changed Its Investment Story

Quanta Services, Inc. PWR | 0.00 |

- Earlier in April, Quanta Services used its 2026 Investor Day to position itself as a key enabler of AI-driven infrastructure, outlining a US$2.40 trillion addressable market through 2030 across data centers, grid modernization and industrial reshoring.

- Management also indicated it expects to surpass its 2026 EPS target and pursue 15%–20% annual growth through 2030, underpinned by recently secured utility contracts with NiSource and AEP.

- We’ll now examine how Quanta’s ambition to outpace its 2026 EPS target could reshape its existing power supercycle investment narrative.

The latest GPUs need a type of rare earth metal called Neodymium and there are only 31 companies in the world exploring or producing it. Find the list for free.

Quanta Services Investment Narrative Recap

To own Quanta Services, you need to believe that the power grid “supercycle” will stay intact as AI, data centers and reshoring drive heavy infrastructure spend, and that Quanta can convert this demand into sustained earnings growth despite its high valuation and elevated debt. The 2026 Investor Day reinforces that long-term story and spotlights NiSource and AEP wins, but does not materially change the near term risk that any slowdown in utility and data center capital spending could expose.

The upcoming Q1 2026 earnings release on April 30 is the most relevant near term checkpoint for this new AI-focused narrative. Management’s Investor Day ambition to outpace its 2026 EPS target and grow 15%–20% annually through 2030 will now be measured against reported results and updated guidance, giving investors an early read on whether the enlarged US$2.40 trillion addressable market is translating into backlog quality, margin resilience and disciplined capital allocation.

Yet against this upbeat framing, investors should also be aware that the biggest near term risk is still...

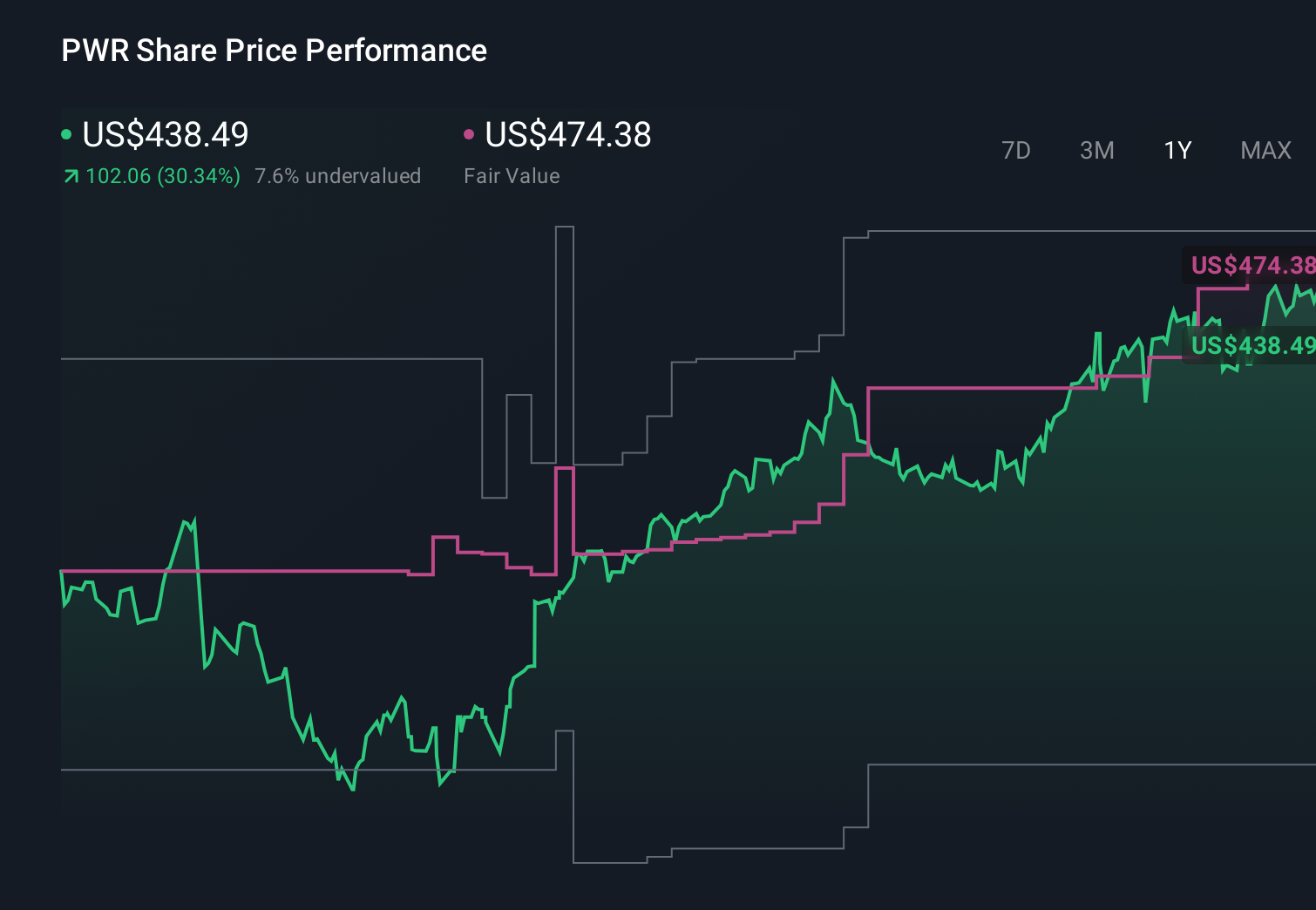

Quanta Services' narrative projects $42.8 billion revenue and $2.1 billion earnings by 2029.

Uncover how Quanta Services' forecasts yield a $593.30 fair value, in line with its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already assuming roughly US$32.5 billion of revenue and US$1.6 billion of earnings by 2028, yet they still warned that heavy dependence on large multi year projects could magnify any project delays or cancellations, reminding you that even bullish AI infrastructure headlines might not fully resolve concerns about earnings volatility.

Explore 4 other fair value estimates on Quanta Services - why the stock might be worth as much as $593.30!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Quanta Services research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Quanta Services research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Quanta Services' overall financial health at a glance.

Want Some Alternatives?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find 60 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 26 elite penny stocks that balance risk and reward.

- This technology could replace computers: discover 25 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.