How Rising Net Interest Income But Softer EPS May Reshape Bank OZK’s (OZK) Earnings Narrative

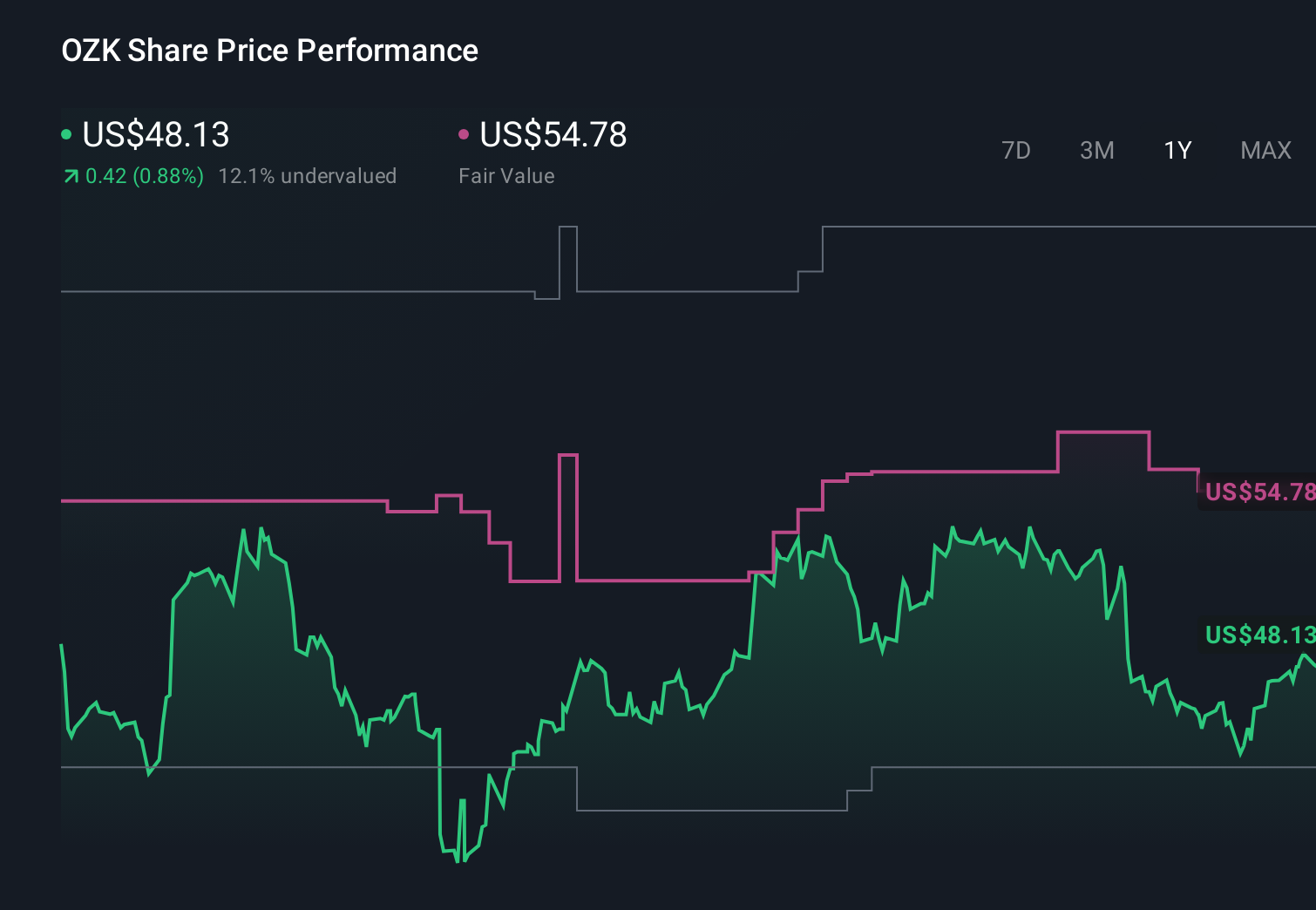

Bank OZK OZK | 0.00 |

- In April 2026, Bank OZK reported past first-quarter results showing net interest income of US$385.57 million, up from US$374.51 million a year earlier, while net income eased to US$163.36 million and diluted earnings per share from continuing operations slipped to US$1.44.

- This mix of higher lending income but softer overall profitability highlights how funding costs, credit expenses, or non-interest items may be affecting the bank’s earnings quality.

- We’ll now examine how Bank OZK’s higher net interest income but lower earnings per share might influence its existing investment narrative.

Find 50 companies with promising cash flow potential yet trading below their fair value.

Bank OZK Investment Narrative Recap

To own Bank OZK, you need to believe its specialized real estate lending and Sun Belt focus can keep producing solid returns without credit quality slipping. The latest quarter’s higher net interest income but slightly lower earnings per share does not appear to change the near term story that the key catalyst is disciplined growth in higher yielding loans, while the biggest risk remains credit losses or margin pressure if commercial real estate or funding costs worsen.

Among recent announcements, the 2.17% increase in the common dividend to US$0.47 per share stands out alongside the softer Q1 earnings. While payouts do not guarantee future performance, the higher dividend in the face of modest earnings slippage frames an interesting contrast with concerns about margin pressure and loan growth, and it may influence how you weigh the appeal of OZK’s income profile against the underlying earnings trends shown in the latest results.

Yet, despite the higher dividend, investors should be aware that rising funding costs and commercial real estate exposures could still...

Bank OZK's narrative projects $2.1 billion revenue and $727.8 million earnings by 2029. This requires 9.8% yearly revenue growth and about a $37 million earnings increase from $690.7 million today.

Uncover how Bank OZK's forecasts yield a $52.33 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were already assuming slower revenue growth to about US$1.9 billion and thinner margins by 2029, so Q1’s softer earnings may push their more pessimistic view on credit and expenses even further, which is worth comparing with your own expectations.

Explore 3 other fair value estimates on Bank OZK - why the stock might be worth over 2x more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Bank OZK research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Bank OZK research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank OZK's overall financial health at a glance.

Looking For Alternative Opportunities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Capitalize on the AI infrastructure supercycle with our selection of the 37 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 18 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.