How Roku's (ROKU) User Growth and Stable Pricing Strategy Are Shaping Its Investment Story

Roku, Inc. Class A ROKU | 94.62 | +7.24% |

- Between 2022 and 2024, Roku increased its active user base from 70 million to 90 million, kept hardware and service prices steady despite inflation, and expanded its sports content offerings, while maintaining financial momentum and drawing continued market attention.

- An interesting insight is that Roku’s patient approach to pricing during the inflation period and its push into high-engagement sports programming have started to deliver tangible financial and operational benefits, setting it apart from competitors who opted to raise prices.

- We'll explore how Roku's substantial user growth, fueled by its stable pricing strategy, could impact the company's broader investment outlook.

AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Roku Investment Narrative Recap

To be a Roku shareholder, you have to believe in the long-term potential of TV streaming, Roku's ability to drive high-margin advertising growth, and the edge it gains by growing its user base while resisting price hikes. The recent news on user growth and stable pricing reinforces Roku’s differentiation but does not materially change the biggest short-term catalyst, continued advertising revenue gains, or alter the risk from tough competition among smart TV platforms.

Of the recent announcements, Roku’s partnership with Amazon Ads is particularly relevant. It expands Roku's reach to over 80 million U.S. connected TV households, directly supporting its advertising revenue catalyst while increasing its attractiveness to major brands and ad buyers.

By contrast, one area investors should be aware of involves the risk that rising competition from ecosystem giants could erode Roku’s household penetration and affect...

Roku's narrative projects $6.1 billion in revenue and $372.1 million in earnings by 2028. This requires 11.4% yearly revenue growth and a $433.6 million increase in earnings from the current level of -$61.5 million.

Uncover how Roku's forecasts yield a $103.27 fair value, a 9% upside to its current price.

Exploring Other Perspectives

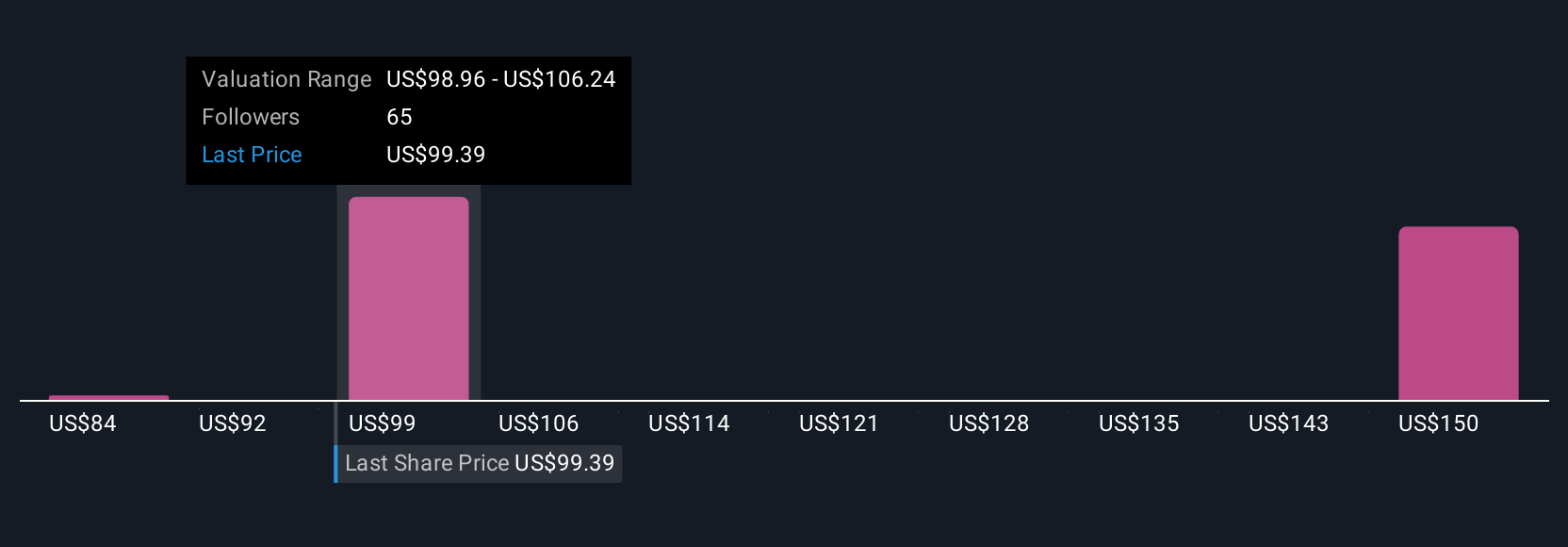

Ten fair value estimates from the Simply Wall St Community for Roku range from US$84.40 up to US$157.81. While opinions vary, persistent rivalry with Amazon, Google, and Apple remains a key challenge shaping future company performance; review these varied viewpoints before making your own call.

Explore 10 other fair value estimates on Roku - why the stock might be worth as much as 67% more than the current price!

Build Your Own Roku Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Roku research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Roku research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Roku's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.