How Russell Growth Index Additions And Style Shift At Southern Copper (SCCO) Has Changed Its Investment Story

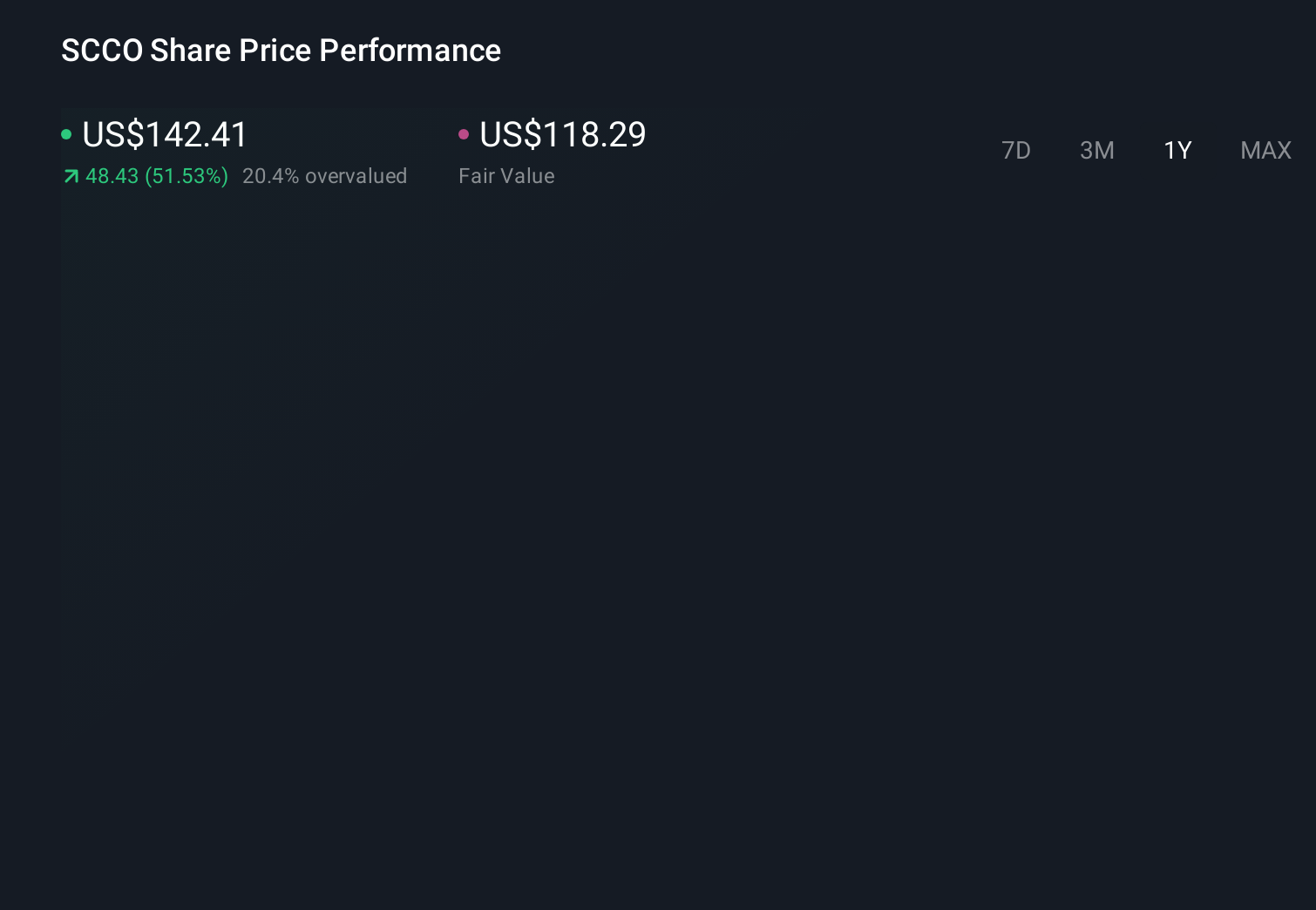

Southern Copper Corporation SCCO | 0.00 |

- In late June 2026, Southern Copper Corporation (NYSE:SCCO) was removed from two Russell defensive/value indexes but added to multiple Russell growth benchmarks, including the Russell 1000 Growth and Russell Top 200 Growth.

- This simultaneous shift out of defensive/value indexes and into several growth benchmarks, alongside a positive Earnings ESP signal, points to a changing market perception of Southern Copper’s profile.

- Now we’ll assess how Southern Copper’s inclusion in major Russell growth benchmarks could influence its existing investment narrative and risk balance.

We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Southern Copper Investment Narrative Recap

To own Southern Copper today, you need to believe in the long term case for copper and the company’s ability to manage costs, community issues and large capex plans. The shift into Russell growth benchmarks highlights a market view that SCCO looks more growth oriented, but it does not materially change the near term focus on execution at key projects and controlling operating costs, which remain central risks to the story.

The most relevant recent announcement alongside this index move is Southern Copper’s positive Earnings ESP of +2.38%, which points to analyst optimism about the next quarterly report. Taken together with its migration into growth indexes, this reinforces the current earnings trajectory as an important catalyst, while the company’s heavy US$15,000,000,000 plus capex pipeline still requires close monitoring for any sign of cost escalation or project delays.

Yet behind the growth label, investors should be aware that community disruptions and project delays could still...

Southern Copper's narrative projects $16.5 billion revenue and $6.0 billion earnings by 2029. This requires 4.3% yearly revenue growth and about a $1.0 billion earnings increase from $5.0 billion today.

Uncover how Southern Copper's forecasts yield a $163.13 fair value, a 4% downside to its current price.

Exploring Other Perspectives

While the index move tilts SCCO toward a growth label, the most pessimistic analysts still assume revenue could shrink about 1.4 percent a year and earnings sit near US$4.9 billion, reminding you that views on project delays and price pressure can differ sharply and may shift again as this new growth classification filters into fresh research.

Explore 4 other fair value estimates on Southern Copper - why the stock might be worth as much as 33% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Southern Copper research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Southern Copper research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Southern Copper's overall financial health at a glance.

Contemplating Other Strategies?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 15 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.