How Salesforce’s Russell Top 50 Exit Amid Agentforce Momentum Has Changed Its Investment Story (CRM)

Salesforce.com, inc. CRM | 0.00 |

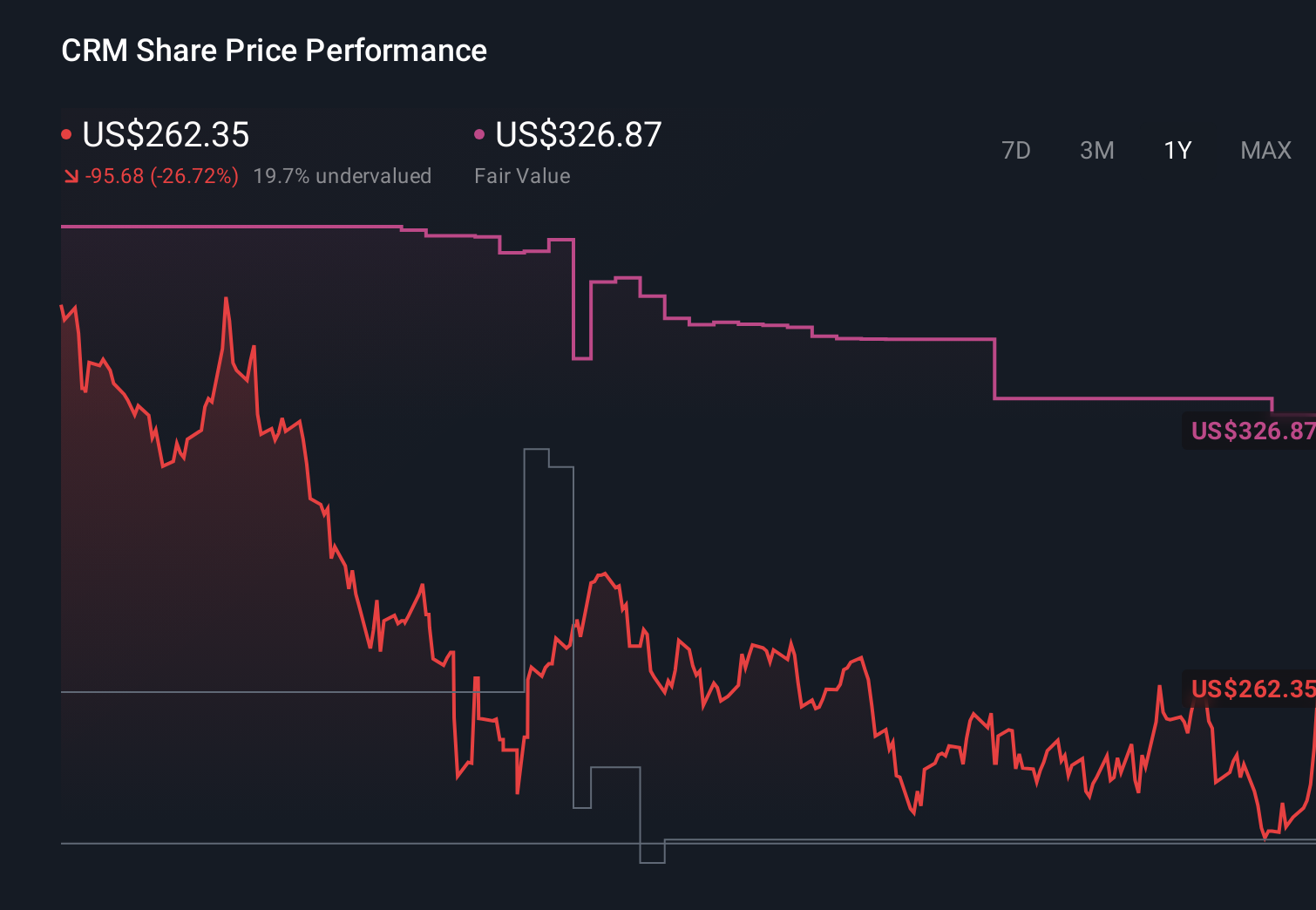

- In late June 2026, Salesforce was removed from the Russell Top 50 Index just as it reported stronger earnings, rapid Agentforce growth, and new AI-focused partnerships across sectors like healthcare and Formula 1.

- This combination of index-related selling pressure, improving operational momentum, and rising scrutiny around AI disruption and data security is now reshaping how investors assess Salesforce’s role in the evolving enterprise software landscape.

- We’ll now explore how Salesforce’s removal from the Russell Top 50 Index influences its investment narrative amid accelerating Agentforce adoption.

We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Salesforce Investment Narrative Recap

To own Salesforce today, you need to believe that its AI and agentic platform can deepen customer lock‑in faster than AI disruption and pricing pressure erode its core CRM franchise. The immediate catalyst is execution around Agentforce and Data Cloud adoption, while the biggest risk is rising concern over AI driven commoditization and data security, now underscored by the Klue integration breach. Salesforce’s removal from the Russell Top 50 Index mainly affects technical trading, not this fundamental debate.

The recent Formula 1 partnership with Visa Cash App Racing Bulls is especially relevant here, because it turns Agentforce 360 into a high visibility real world showcase for AI agents, data and Slack working together in a complex live environment. For investors tracking whether Salesforce’s AI narrative is translating into concrete usage and higher contract value, deployments like this, alongside examples such as Petty Products on Agentforce Revenue Management, go straight to the heart of the current catalyst.

Yet beneath the AI success stories, the Klue related data exposure raises questions investors should be aware of around how third party integrations could impact...

Salesforce’s narrative projects $56.7 billion revenue and $10.2 billion earnings by 2029. This requires 9.8% yearly revenue growth and a $2.2 billion earnings increase from $8.0 billion today.

Uncover how Salesforce's forecasts yield a $255.28 fair value, a 61% upside to its current price.

Exploring Other Perspectives

Before this news, the most optimistic analysts were assuming revenue could reach about US$58.9 billion with US$11.6 billion in earnings, while also treating AI driven customer lock in as a powerful growth engine, which sharply contrasts with the more cautious view that AI and integrations like Klue might instead heighten security and disruption risks.

Explore 31 other fair value estimates on Salesforce - why the stock might be worth just $200.00!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Salesforce research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Salesforce research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Salesforce's overall financial health at a glance.

No Opportunity In Salesforce?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Capitalize on the AI infrastructure supercycle with our selection of the 51 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.