How Strong Q1 Results and Higher Guidance at Ralph Lauren (RL) Have Changed Its Investment Story

Ralph Lauren Corporation Class A RL | 379.87 | -1.37% |

- Ralph Lauren Corporation recently reported stronger-than-expected results for its first fiscal quarter ended June 28, 2025, with net sales rising to US$1,719.1 million and net income reaching US$220.4 million, while the company also raised its full-year fiscal 2026 revenue and margin guidance.

- Management highlighted continued investments in direct-to-consumer channels, digital innovation, and global expansion as key drivers of the upgraded outlook, even as they noted ongoing macroeconomic and tariff-related uncertainties.

- Next, we'll explore how Ralph Lauren's raised full-year guidance and focus on brand expansion could reshape its long-term investment narrative.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

Ralph Lauren Investment Narrative Recap

To invest in Ralph Lauren, one has to believe in the company’s ability to grow its brand through direct-to-consumer channels, digital initiatives, and global reach, even as potential tariff and macroeconomic pressures remain front of mind. The company’s upgraded guidance and strong first-quarter results reinforce its position, but investors should consider that currency volatility remains the most important near-term risk, and the updated outlook does not materially alter this. Recent results support ongoing optimism, but foreign exchange headwinds could still impact reported growth in the quarters ahead.

Among recent company developments, Ralph Lauren’s move to raise its full-year fiscal 2026 guidance, calling for low-to-mid single digit revenue growth and improved operating margins, lines up most directly with the current focus on margin expansion through cost management and direct channel gains. This announcement provides valuable context for assessing how the brand’s evolving business mix may contribute to earnings resilience, especially as the broader retail sector faces global economic uncertainties.

However, despite the company’s positive trajectory, investors should be aware of continuing currency risks that could dampen results if the US dollar strengthens unexpectedly...

Ralph Lauren is projected to reach $8.2 billion in revenue and $980.3 million in earnings by 2028. This outlook is based on an assumed annual revenue growth rate of 5.1% and represents a $237.4 million increase in earnings from the current $742.9 million.

Uncover how Ralph Lauren's forecasts yield a $330.33 fair value, a 10% upside to its current price.

Exploring Other Perspectives

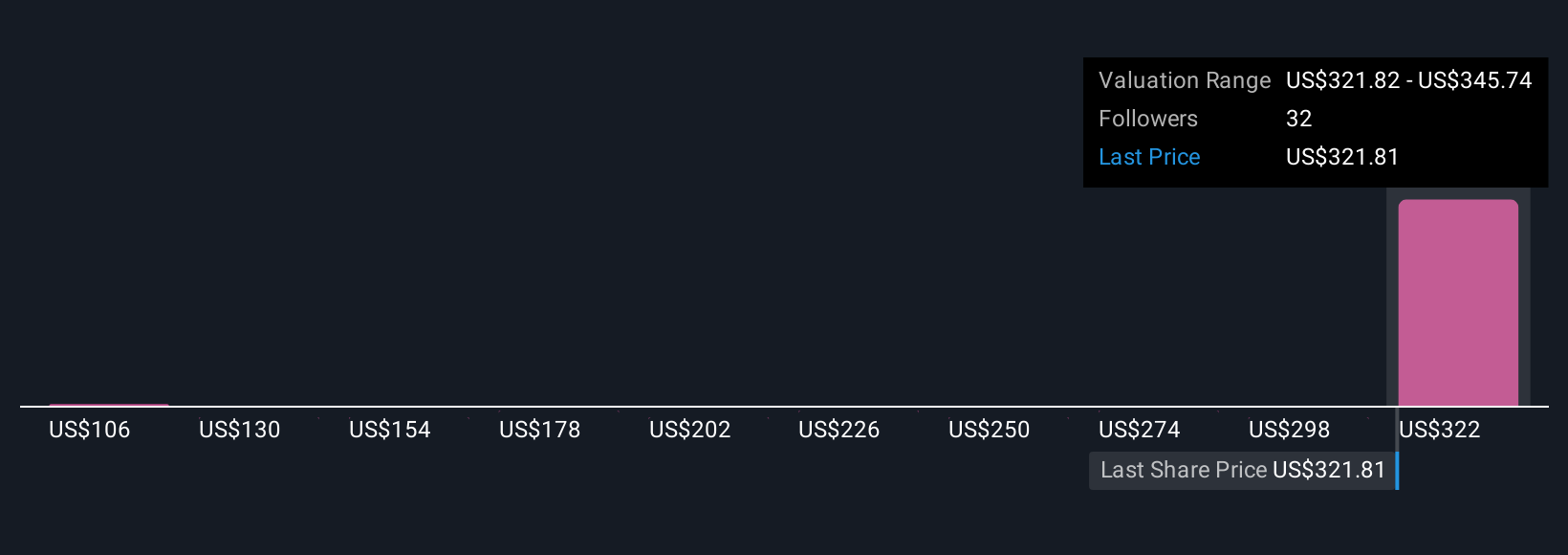

Six community-sourced fair value estimates for Ralph Lauren range from US$106.47 to US$371.67, reflecting wide differences in investor opinion. With currency fluctuations still a key risk, your view on global markets could shape your outlook on Ralph Lauren’s potential, see what the Community thinks and consider how you might interpret the company’s prospects.

Explore 6 other fair value estimates on Ralph Lauren - why the stock might be worth less than half the current price!

Build Your Own Ralph Lauren Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Ralph Lauren research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Ralph Lauren research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ralph Lauren's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 18 early-stage AI stocks could fund your retirement.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.