How Sunrun’s 16 GW Home-Grid Partnership With Tesla Has Changed Its Investment Story (RUN)

Sunrun Inc. RUN | 0.00 |

- On 24 June 2026, Sunrun, Renew Home and Tesla Energy Operations announced an agreement to aggregate millions of home energy devices into more than 16 gigawatts of flexible capacity for hyperscalers and utilities across key U.S. power markets.

- This collaboration creates what the companies describe as the country’s largest distributed power plant, aiming to unlock idle residential batteries and smart devices to relieve grid congestion, support data center growth, and expand customer rewards programs.

- We’ll now examine how this plan to aggregate over 16 gigawatts of flexible residential capacity could influence Sunrun’s existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Sunrun Investment Narrative Recap

To own Sunrun, you need to believe residential solar and storage can keep scaling profitably despite incentive risk, capital intensity, and competition. The biggest near term catalyst is growth in higher margin storage and grid services, while the most pressing risk remains policy and tax credit uncertainty alongside financing needs. The 16 GW aggregation agreement reinforces the grid services story but does not remove those funding and regulatory pressures.

The news sits alongside Sunrun’s continued push to monetize its long term contracts through securitizations, including the US$584 million of Class A notes issued across 2025 and the US$584 million-plus raised again in 2026. Those deals highlight both the opportunity and the dependency on healthy capital markets as Sunrun layers new grid capacity offerings on top of its existing contracted cash flows.

Yet beneath this upside, investors should be aware that...

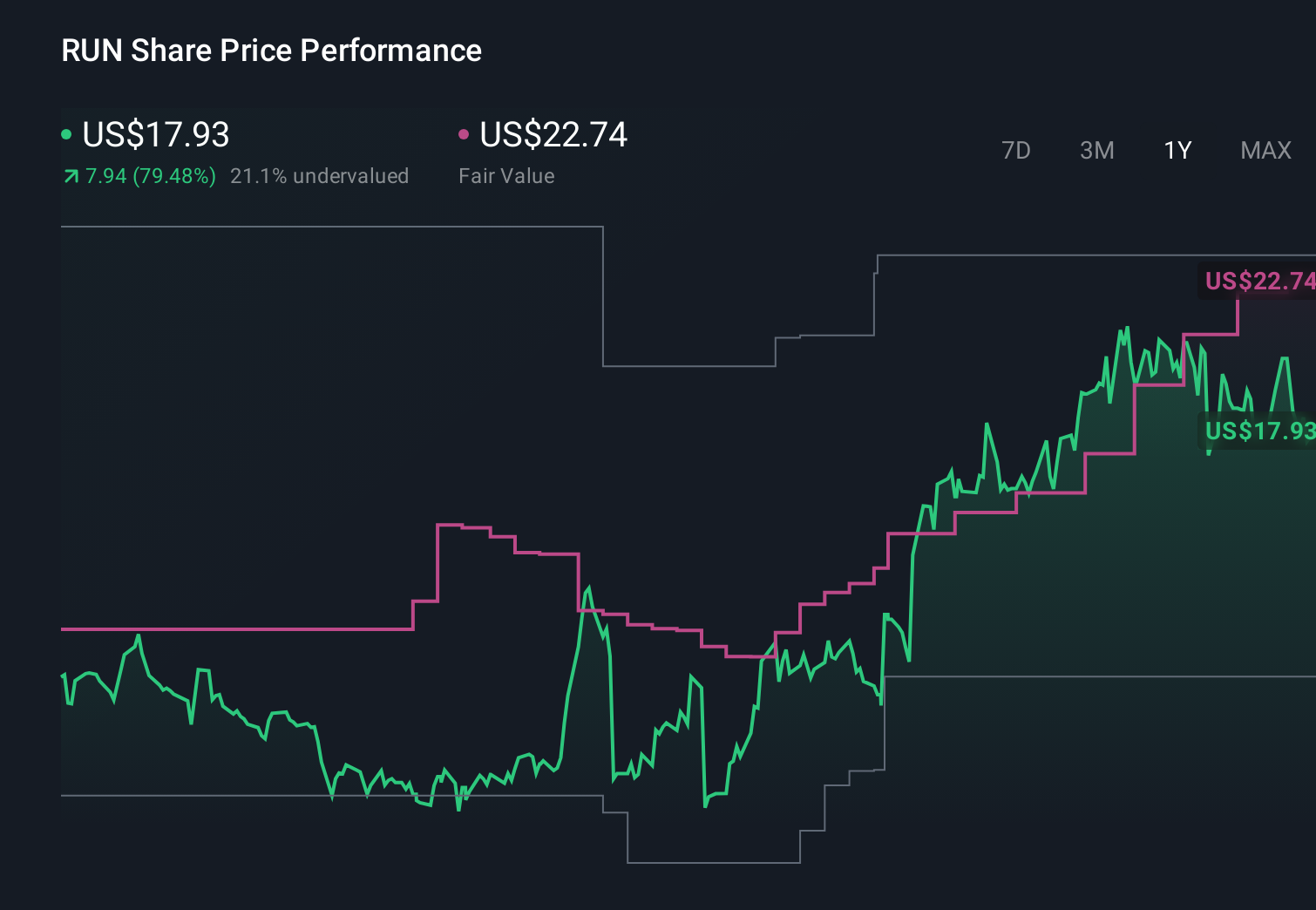

Sunrun's narrative projects $3.7 billion revenue and $56.5 million earnings by 2029. This implies 8.0% yearly revenue growth but a sharp earnings decline of $391.1 million from $447.6 million today.

Uncover how Sunrun's forecasts yield a $19.67 fair value, a 52% upside to its current price.

Exploring Other Perspectives

Bearish analysts were expecting Sunrun’s revenue to shrink about 5.8% annually and earnings to fall toward roughly US$291 million by 2029, a far more pessimistic view than the grid focused upside case you have just read about, and a reminder that your own stance should weigh both this new 16 GW opportunity and the possibility that these cautious forecasts may or may not be revised.

Explore 3 other fair value estimates on Sunrun - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Sunrun research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Sunrun research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sunrun's overall financial health at a glance.

Looking For Alternative Opportunities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 41 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.