How Tariffs And ATV Strategy Shifts Will Impact Polaris (PII) Investors

Polaris Inc. PII | 57.91 57.91 | +9.22% 0.00% Pre |

- In recent days, Polaris has been downgraded by AI models as tariff costs, margin pressure, and projected net losses weigh on near-term performance, even as the company continues to generate operating cash flow, reduce debt, and maintain its dividend.

- At the same time, the all-terrain vehicle market is expected to expand steadily through 2035, with Polaris aiming to capture demand in the growing mid-capacity segment through its Sportsman 570 lineup and rising side-by-side vehicle volumes.

- With Polaris confronting tariff-driven margin pressure while targeting growth in mid-capacity ATVs, we'll assess how this reshapes its investment narrative today.

We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Polaris Investment Narrative Recap

To own Polaris today, you need to believe that its core powersports franchises and cash generation can outlast tariff headwinds, margin pressure, and current net losses, while the all-terrain vehicle market grows steadily. The AI-driven downgrade highlights that the most important near term catalyst is evidence of margin stabilization, and the biggest risk remains tariff driven cost inflation and uncertain tariff policy, which could keep profitability under pressure despite solid operating cash flow and an ongoing dividend.

Against this backdrop, Polaris’ decision in January 2026 to raise its quarterly dividend by 2% to US$0.68 per share stands out. That move signals confidence in cash generation even after a 2025 net loss of about US$465.5 million, and it directly ties into key catalysts around balance sheet strength, tariff mitigation efforts, and the company’s ability to support shareholder payouts while absorbing higher gross tariff costs.

Yet despite resilient cash flow, investors should be aware that tariff costs and weak powersports demand could still materially affect Polaris’ margins and earnings trajectory...

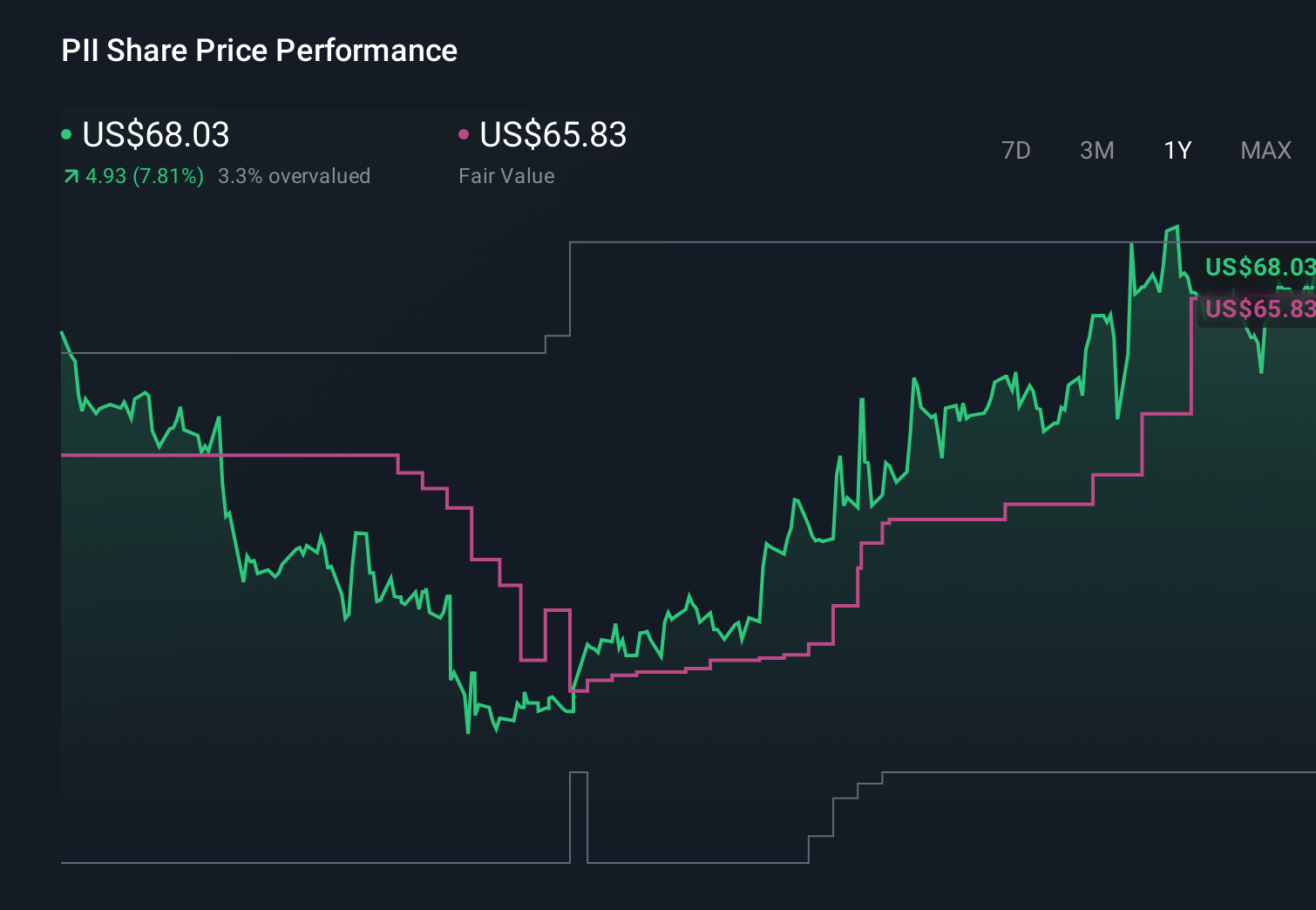

Polaris’ narrative projects $7.8 billion revenue and $243.0 million earnings by 2029.

Uncover how Polaris' forecasts yield a $66.71 fair value, a 21% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts took a far more pessimistic view, assuming only about US$7.1 billion of revenue and roughly US$219.8 million of earnings by 2028, warning that heightened tariff exposure could keep Polaris’ profitability well below peers even if current narratives and the latest AI downgrade eventually prove too optimistic.

Explore 4 other fair value estimates on Polaris - why the stock might be worth 42% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Polaris research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Polaris research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Polaris' overall financial health at a glance.

Ready For A Different Approach?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.