How Texas’ New Data‑Privacy Lawsuit Against Netflix (NFLX) Has Changed Its Investment Story

Netflix NFLX | 0.00 |

- In recent days, Texas Attorney General Ken Paxton filed a lawsuit accusing Netflix of illegally collecting and monetizing sensitive user and children’s data without proper consent and of designing its platform to be addictive. The state is seeking civil penalties, data deletion, and limits on targeted advertising, while Netflix calls the claims meritless and says it complies with privacy laws.

- The suit directly challenges Netflix’s data practices just as it leans more heavily on targeted advertising and engagement metrics to support its content spending and business model.

- We’ll now examine how this Texas data-privacy lawsuit, and the potential for higher compliance and reputational costs, could reshape Netflix’s investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 39 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Netflix Investment Narrative Recap

To own Netflix today, you generally have to believe it can keep turning its global scale, content engine, and growing ad tier into solid earnings, even as growth expectations moderate and the stock has lagged the broader market over the past year. The Texas data-privacy lawsuit adds to the existing regulatory risk around data and algorithms, but at this stage it does not clearly alter the key near term catalyst, which remains execution on advertising and engagement monetization.

The most directly relevant recent announcement is Netflix’s push into advertising, with management expecting ad revenue to roughly double in 2026 and emphasizing engagement-based monetization. That ambition relies heavily on data-driven targeting and measurement, which is exactly what the Texas lawsuit is challenging. If regulators force tighter rules around data use, it could increase compliance costs or slow parts of the ad business just as it becomes more important to Netflix’s story.

But while the upside case leans on rising ad revenue and price increases, investors should also be aware that growing regulatory scrutiny of Netflix’s data practices could...

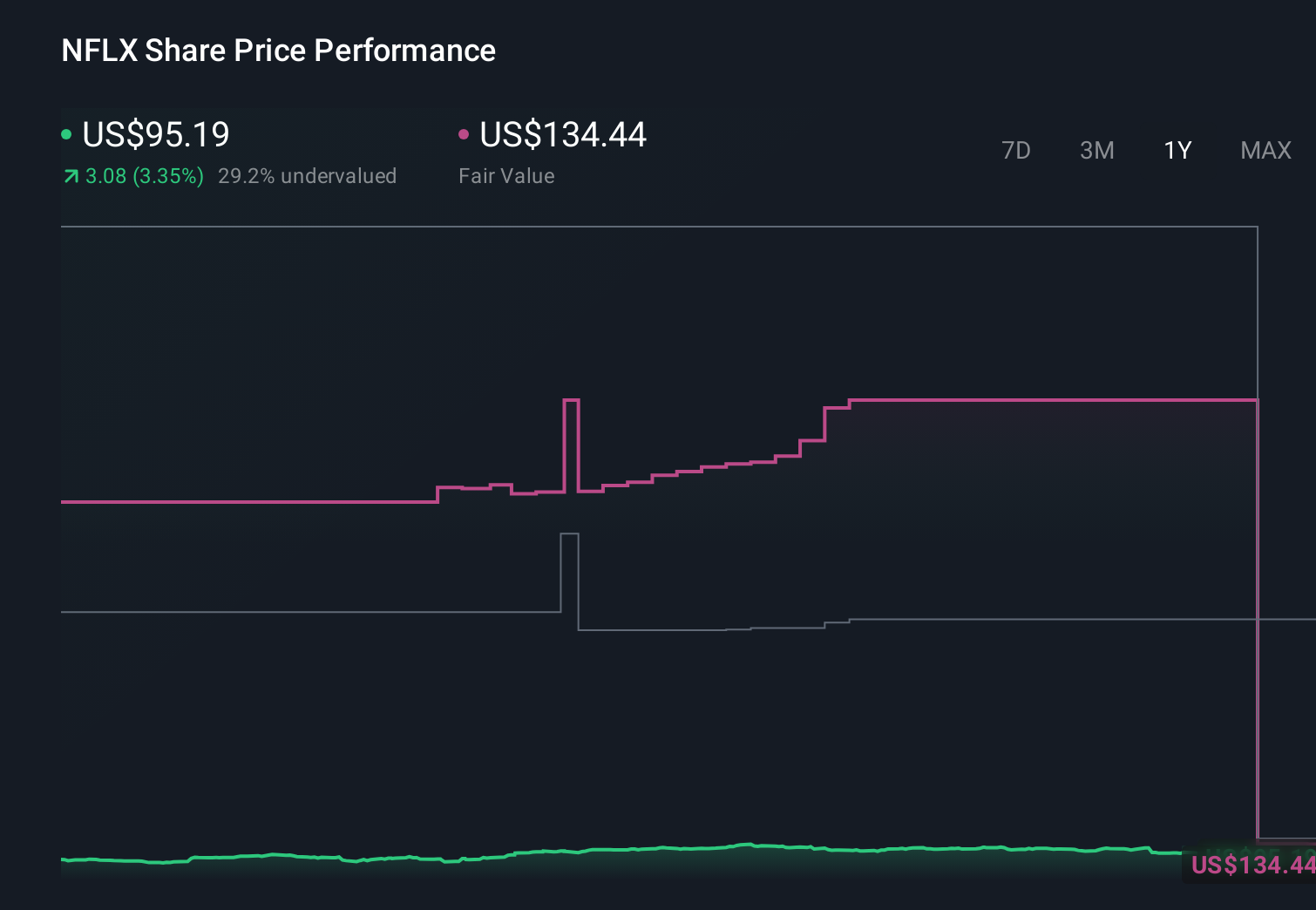

Netflix's narrative projects $59.4 billion revenue and $17.7 billion earnings by 2028. This requires 12.5% yearly revenue growth and a $7.5 billion earnings increase from $10.2 billion.

Uncover how Netflix's forecasts yield a $113.17 fair value, a 29% upside to its current price.

Exploring Other Perspectives

Compared with the baseline view, the most bearish analysts were already cautious, assuming only about 9.4% annual revenue growth to roughly US$61.4 billion and thinner margins by 2029. In light of the Texas data-privacy lawsuit and broader regulatory risks, their narrative highlights how much more pessimistic some expectations are, and why it can be useful for you to weigh several very different outlooks before deciding what you think Netflix is really worth.

Explore 26 other fair value estimates on Netflix - why the stock might be worth as much as 71% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Netflix research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Netflix research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Netflix's overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with 28 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.