How Textron’s Industrial Spinoff And Portfolio Refocus At Textron (TXT) Has Changed Its Investment Story

Textron Inc. TXT | 0.00 |

- In late April 2026, Textron Inc. announced plans to separate its Industrial segment from its core aerospace and defense operations, while also reporting higher first-quarter 2026 revenue of US$3,695 million and net income of US$220 million alongside ongoing share repurchases and a quarterly dividend declaration.

- The proposed separation would create a focused aerospace and defense “New Textron” with expected 2026 revenues above US$12.00 billion and backlog of US$19.00 billion, while an Industrial business of more than US$3.00 billion in expected 2026 revenues could pursue capital allocation and growth priorities tailored to its automotive and specialized vehicle markets.

- We’ll now explore how Textron’s planned separation of its Industrial segment could reshape the company’s investment narrative and long-term positioning.

The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Textron Investment Narrative Recap

To own Textron today, you need to believe in the value of a simpler, pure‑play aerospace and defense company centered on Textron Aviation, Bell and Textron Systems. The planned separation of the Industrial segment is now the key short term catalyst, while execution risk around the transaction and any disruption to margins or backlog conversion is the biggest near term concern. The latest Q1 2026 results and capital returns do not materially change that risk‑reward balance.

The Industrial separation announcement itself is the most relevant recent update. By carving out over US$3.00 billion in expected 2026 Industrial revenues from “New Textron,” the company is effectively betting that a focused aerospace and defense profile, supported by a US$19.00 billion backlog and ongoing buybacks and dividends, will be more compelling than the current diversified structure for driving the next phase of value creation.

Yet investors should not overlook how dependent this thesis could become on defense programs and regulatory decisions over the next few years...

Textron's narrative projects $16.7 billion revenue and $1.2 billion earnings by 2029. This requires 4.2% yearly revenue growth and an earnings increase of about $300 million from $923.0 million.

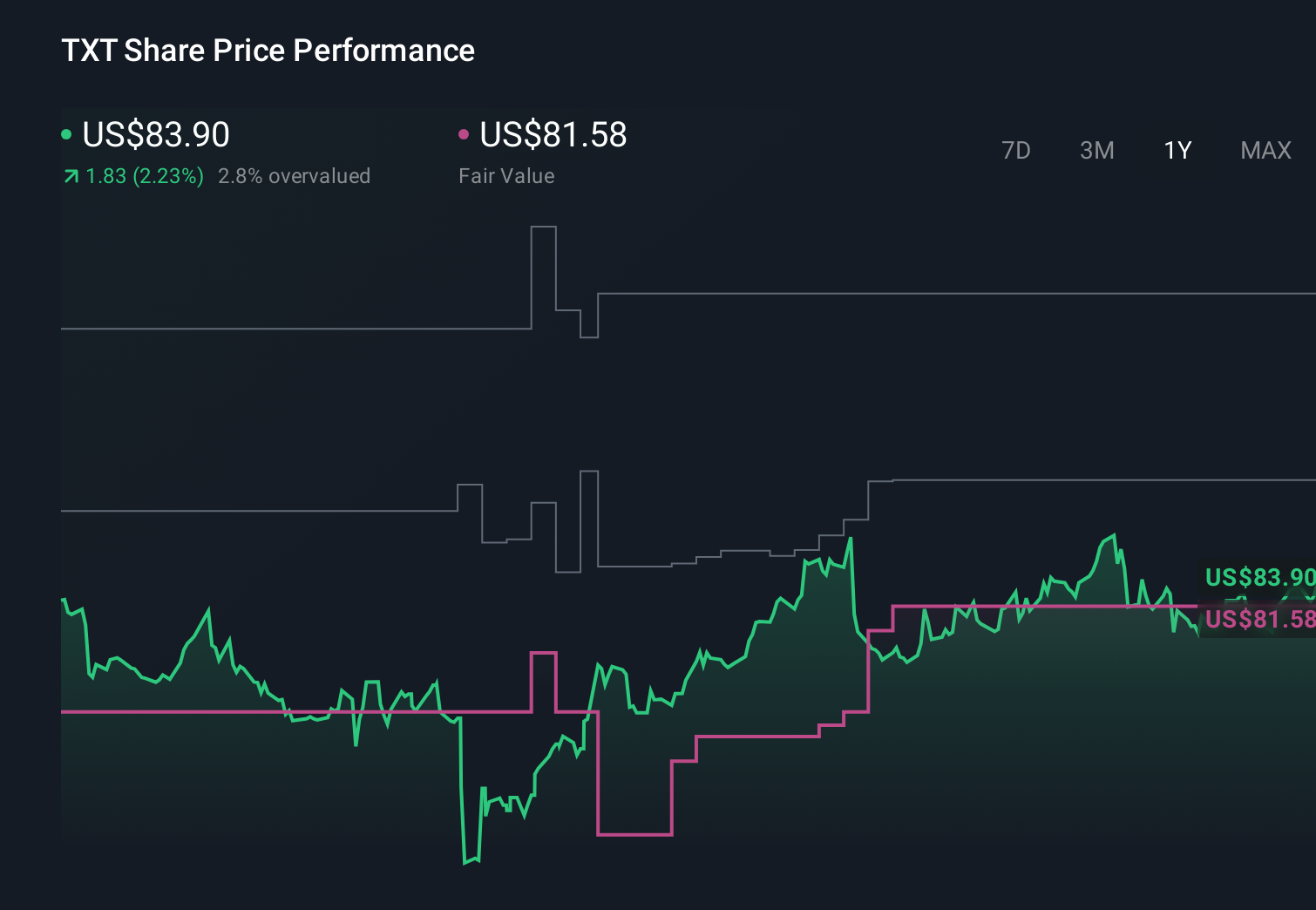

Uncover how Textron's forecasts yield a $98.95 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already expected Textron to reach about US$17.3 billion in revenue and US$1.2 billion in earnings, and they see rising defense spending as a key support; if you are weighing this against the new separation plan and the risk of overreliance on U.S. contracts, it is a reminder that informed investors can reasonably reach very different conclusions about the same set of facts.

Explore 5 other fair value estimates on Textron - why the stock might be worth as much as 14% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Textron research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Textron research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Textron's overall financial health at a glance.

Searching For A Fresh Perspective?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 33 companies in the world exploring or producing it. Find the list for free.

- Find 49 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.