How the 20% Drop Shapes Rocket Lab’s 2025 Valuation Outlook

Rocket Lab RKLB | 65.52 | +2.02% |

- Wondering if Rocket Lab stock is a bargain or already priced for perfection? Let’s dig into what the numbers and recent events are telling investors right now.

- Rocket Lab has soared 105.3% year-to-date and an incredible 249.5% over the past year, though it's pulled back sharply, dropping 20.3% in just the last month.

- This rollercoaster ride has been shaped by headlines ranging from major contract wins with government agencies to notable technological achievements, such as their reusable launch successes. These milestones have sparked optimism, but also heightened debate about the company’s risk and reward profile.

- Currently, Rocket Lab scores a 0 out of 6 on our undervaluation checks, which raises questions about whether traditional valuation methods are capturing the full story. We’ll break down these common approaches, and by the end, you’ll see there is a smarter way to gauge what Rocket Lab is really worth.

Rocket Lab scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

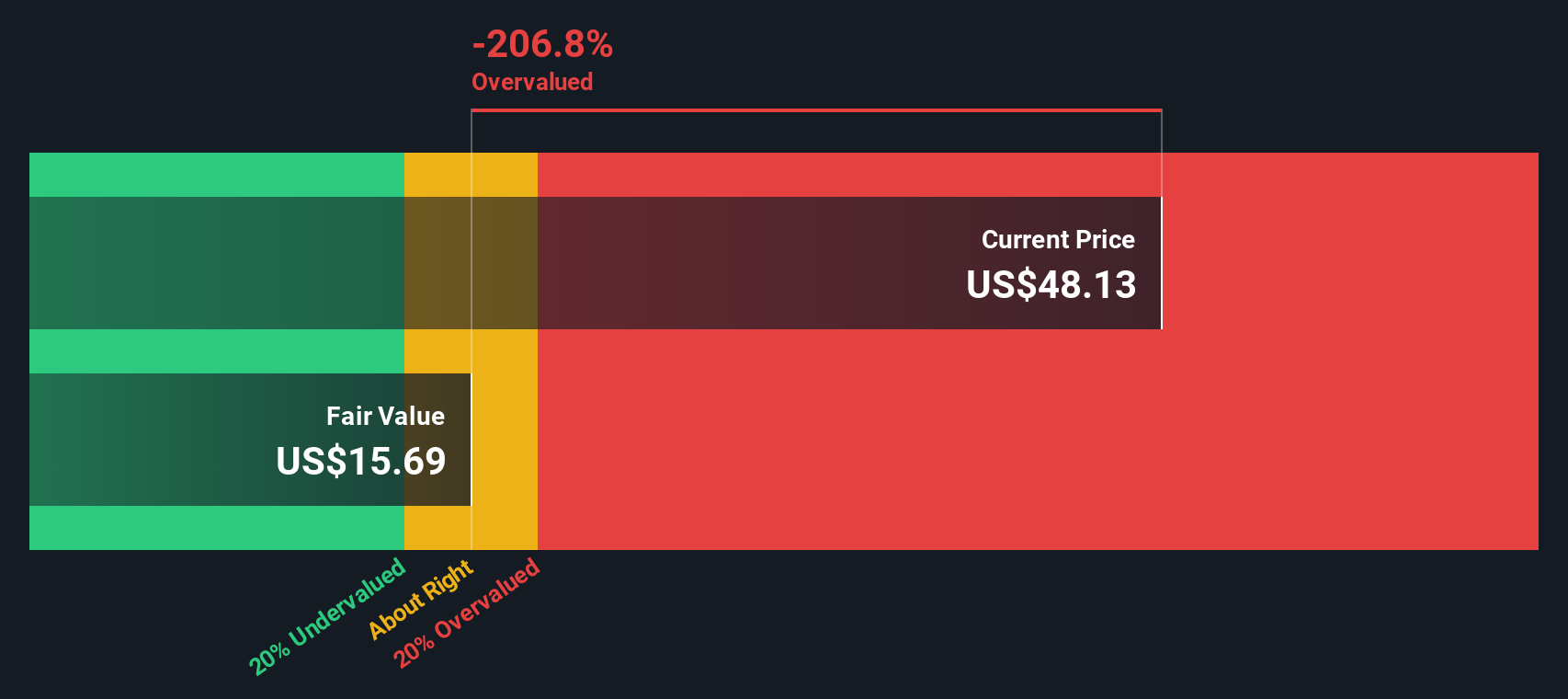

Approach 1: Rocket Lab Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates what a company is worth based on its expected future cash flows by projecting each year's figures and then discounting them back to today's value. This helps investors assess whether the current share price reflects the company's potential earnings.

For Rocket Lab, the latest reported Free Cash Flow is -$220.28 million, indicating the company is currently spending more than it generates from its core business each year. Looking ahead, analysts forecast that Free Cash Flow will become positive by 2027 and reach $58.55 million. For the period beyond the next five years, Simply Wall St projects Free Cash Flows rising to as much as $710.22 million by 2035.

After discounting these projected cash flows, the estimated intrinsic value for Rocket Lab is $19.16 per share. When compared to the current share price, this suggests the stock is 167.5% overvalued according to the DCF methodology.

In summary, even with strong future growth projections, the figures indicate Rocket Lab's shares are trading significantly above what its future cash flows would support today.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Rocket Lab may be overvalued by 167.5%. Discover 856 undervalued stocks or create your own screener to find better value opportunities.

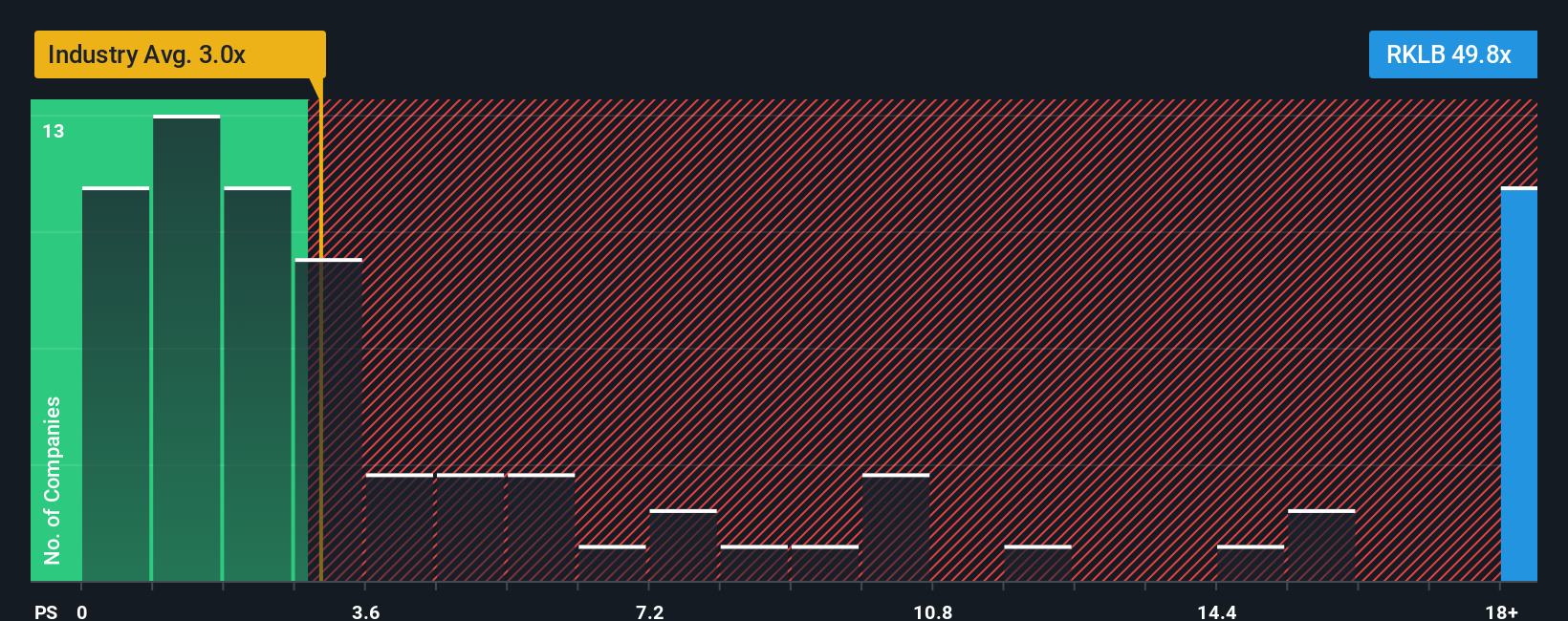

Approach 2: Rocket Lab Price vs Sales

For companies that are still working toward profitability, the Price-to-Sales (PS) multiple is often the preferred valuation metric. This is because earnings may be negative or misleading due to heavy investment in growth, while revenue provides a more stable view of the business’s scale and progress.

Growth expectations and risk play a significant role in determining what counts as a “normal” or “fair” PS ratio. Fast-growing, innovative companies can sometimes justify higher multiples, particularly if their industry views future earnings potential as substantial. At the same time, higher business risks or industry disruptions typically require a lower multiple to compensate for uncertainty.

Rocket Lab’s current PS ratio stands at 49.36x, far above the Aerospace and Defense industry average of 2.99x and the peer average of 12.41x. This signals that the market is pricing the company well above its sector peers based solely on sales.

Simply Wall St’s proprietary “Fair Ratio” for Rocket Lab is 7.80x, designed to factor in unique aspects such as its earnings growth potential, business risks, profit margins, market cap, and other industry nuances. Unlike basic industry or peer comparisons, the Fair Ratio looks deeper at the specific characteristics that drive a valuation premium or discount.

Comparing the actual PS ratio of 49.36x to the Fair Ratio of 7.80x, it is clear the market is assigning a significant premium beyond what Rocket Lab’s fundamentals justify based on these underlying factors.

Result: OVERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1372 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Rocket Lab Narrative

Earlier, we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is simply your story or perspective about a company, including how you think the business will perform, what kinds of profits it might achieve, and what its true value should be, all backed by your own assumptions about future revenue, earnings, and margins.

With Narratives, you connect the dots from Rocket Lab’s business story to a detailed financial forecast and finally to a tailored fair value calculation. This approach moves beyond static numbers and lets you factor in industry trends, technological progress, competitive risks, and your personal outlook on the company’s future.

Narratives are available on Simply Wall St's Community page and empower millions of investors with an easy way to compare their assumptions and forecasts to others, update their view when new news or results are released, and know instantly if a stock is trading below or above their own Fair Value target.

For example, some Rocket Lab Narratives set a bullish fair value of $60 per share, assuming rapid launch expansion and successful Neutron development, while others take a more careful stance around $20, factoring in execution challenges and ongoing losses. This shows how your personal viewpoint can directly inform your buy or sell decisions and adjust as new information arrives.

For Rocket Lab, we will make it really easy for you with previews of two leading Rocket Lab Narratives:

Fair Value: $58.67

Current price is 12.7% below the narrative fair value

Revenue Growth Rate: 37.36%

- Rocket Lab's vertical integration, end-to-end space solutions, and launch cadence are positioning it for major defense contracts and sustained multi-year revenue growth.

- The company is targeting margin expansion through international demand, higher launch prices, and reusability. Profitability is projected as investments shift from development to production.

- Key risks include heavy ongoing R&D spend, reliance on large contracts, competition with SpaceX, and potential execution or regulatory setbacks. Analysts’ consensus target suggests shares are fairly priced if ambitious objectives are met.

Fair Value: $31.72

Current price is 61.5% above the narrative fair value

Revenue Growth Rate: 30.0%

- Achieving rapid scale in launches and hitting ambitious revenue targets hinges on successful, reliable Neutron operations. Failure here risks the entire company.

- Space launch competition is intensifying, especially from SpaceX, and Rocket Lab faces challenges managing working capital and the expectations of early customers.

- Maintaining a low-cost focus and becoming profitable from ongoing operations is essential; market dominance is not assured amidst government-subsidized and billionaire-backed competitors.

Do you think there's more to the story for Rocket Lab? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.