How the First CRISPR-Based Therapy Approval Impacts CRISPR Therapeutics’ Valuation

CRISPR Therapeutics AG CRSP | 48.81 48.75 | +2.61% -0.12% Post |

- Curious if CRISPR Therapeutics is undervalued, overhyped, or hiding a bargain? Let’s cut through the biotech buzz and look at the numbers that matter.

- Shares saw some turbulence recently, with a 24.5% dip over the past month. They are still up 21.2% year to date and 4.9% higher over the last year.

- Recent headlines focused on new regulatory decisions and progress in gene-editing therapies, keeping investors’ eyes on both breakthroughs and challenges. The approval of the first CRISPR-based therapy in the US put the spotlight firmly on this stock and drove notable volatility as market expectations shifted.

- Right now, CRISPR Therapeutics posts a valuation score of 4 out of 6, meaning it looks attractively priced on most, but not all, key measures. We will dive into those different ways to value the stock in a moment, and reveal one potentially better way to look at valuation by the end.

Approach 1: CRISPR Therapeutics Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model works by estimating a company’s future cash flows and discounting them back to today’s value. This method is designed to find the intrinsic value of a stock based on what the company is expected to generate in actual cash over time rather than headlines or hype.

For CRISPR Therapeutics, recent cash flow numbers are still negative, with a last twelve months free cash flow (FCF) of minus $306.7 million. According to analyst consensus and further extrapolations, this figure is projected to climb steadily and could transition to a positive $136.9 million by the year ending 2029. Looking even further ahead, Simply Wall St’s model extends projections up to 2035, where annual FCF could reach over $704 million, showing a sharp improvement as clinical programs mature and potential therapies hit the market.

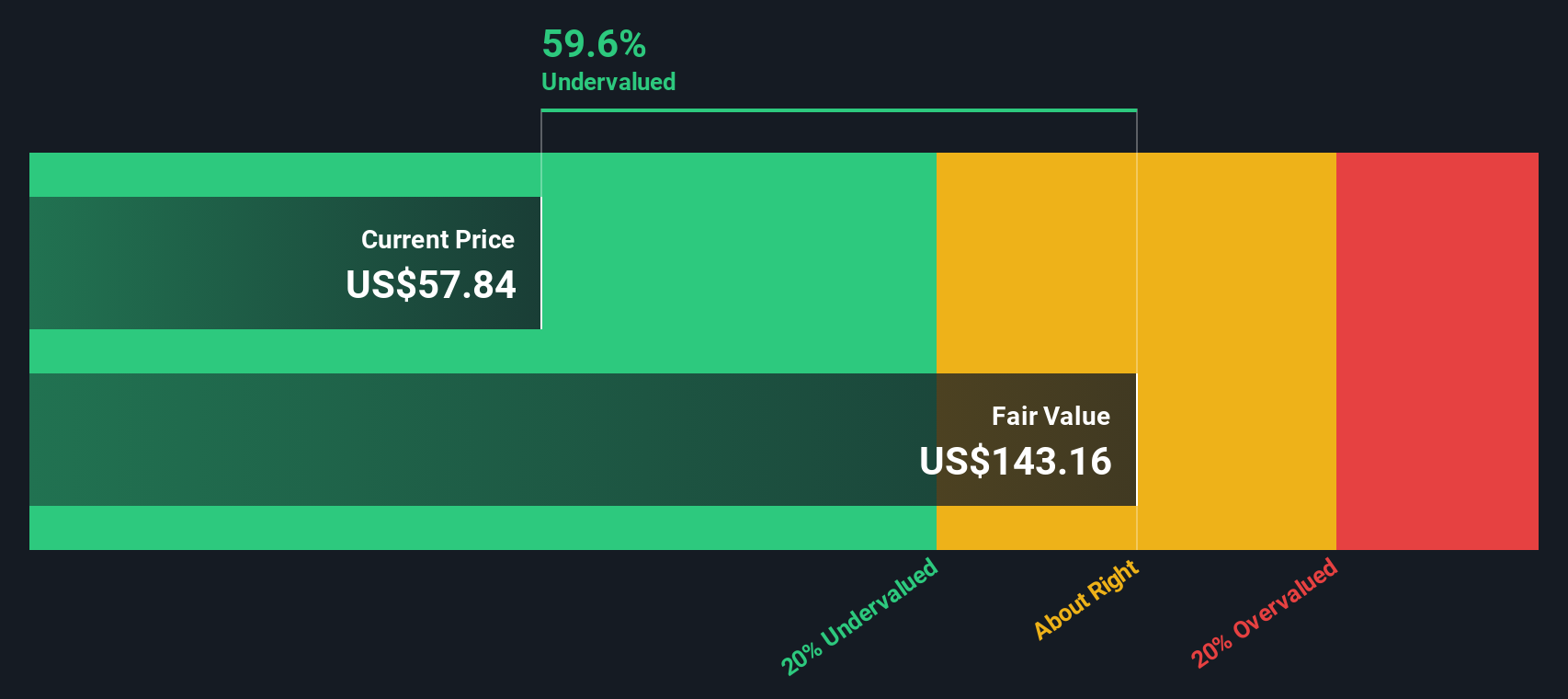

When these projected cash flows are run through the 2 Stage Free Cash Flow to Equity model and discounted, the estimated fair value for CRISPR Therapeutics comes out to $127.57 per share. Based on this, the current share price implies the stock is trading at a 60.6 percent discount to its intrinsic value, suggesting it is significantly undervalued right now.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests CRISPR Therapeutics is undervalued by 60.6%. Track this in your watchlist or portfolio, or discover 918 more undervalued stocks based on cash flows.

Approach 2: CRISPR Therapeutics Price vs Book

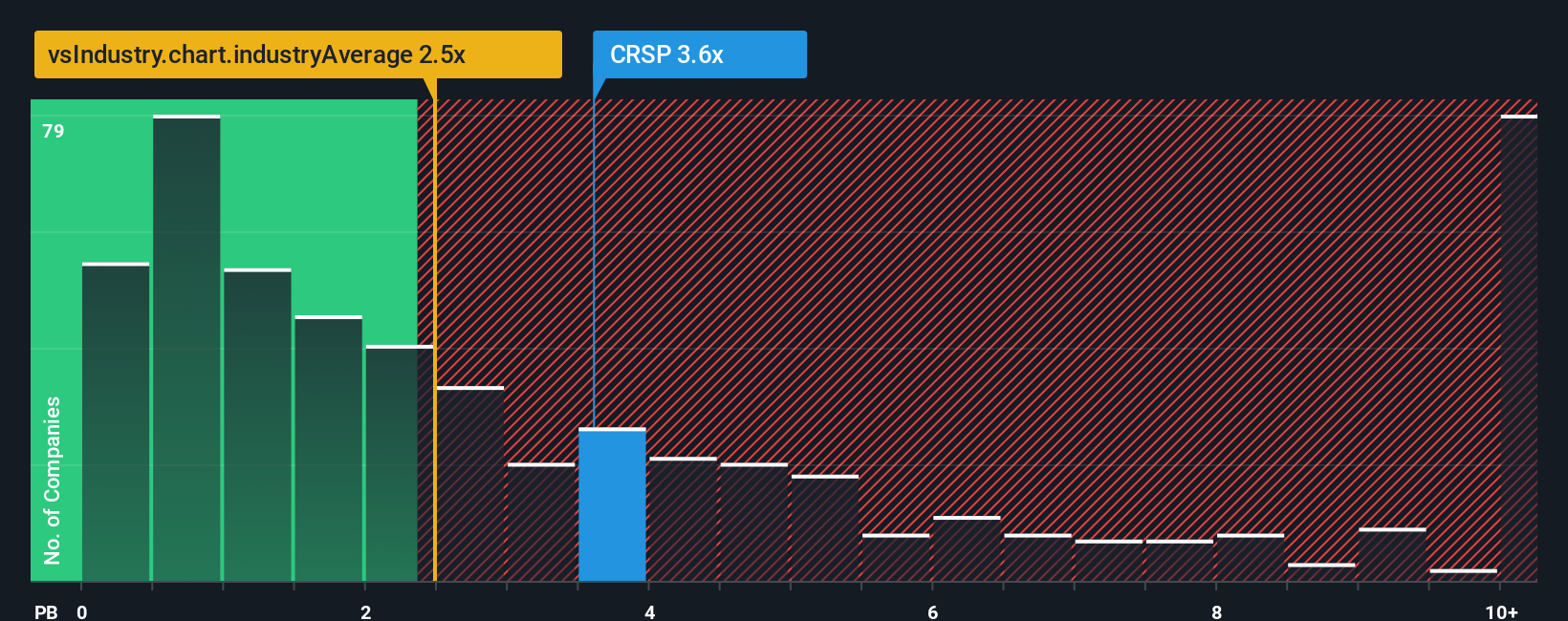

The price-to-book (P/B) ratio is a common valuation tool for biotech companies like CRISPR Therapeutics that are not consistently profitable yet. Since their earnings can be volatile or even negative as they invest heavily in research and development, assessing their value relative to the underlying assets on their balance sheet can provide more meaningful insight than using profit-based multiples.

Growth expectations, risk profile, and business fundamentals all help determine what a “normal” or “fair” P/B ratio should be for a given company. Fast-growing or less risky businesses tend to fetch higher P/B multiples, reflecting investor willingness to pay more for future potential. In contrast, riskier or slower-growing companies warrant lower ratios.

Currently, CRISPR Therapeutics trades at a P/B ratio of 2.5x. This is right in line with the Biotechs industry average of 2.5x and notably lower than the peer average of 11.6x, suggesting the stock is not trading at a premium compared to similar companies.

Simply Wall St’s proprietary “Fair Ratio” goes a step further by tailoring what would be a reasonable P/B for CRISPR given its unique blend of future growth prospects, market cap, industry norms, profitability, and risk factors. This individualized benchmark is more reliable than simply comparing against broad industry or peer averages because it captures company-specific variables that truly move valuation in biotech.

When you compare CRISPR Therapeutics’ actual P/B ratio to its Fair Ratio, the numbers are almost identical, implying the stock is currently valued about right based on its specific fundamentals.

Result: ABOUT RIGHT

PB ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1422 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your CRISPR Therapeutics Narrative

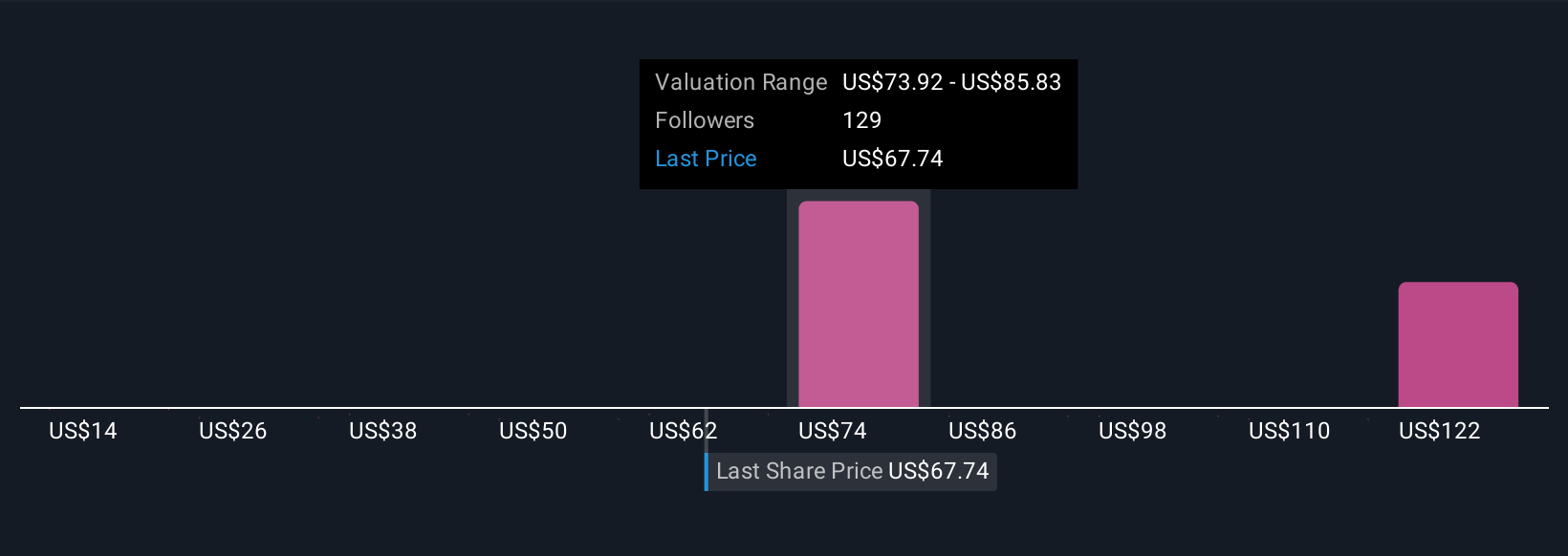

Earlier we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is simply your story and perspective about a company, connecting what you believe about its future with concrete financial forecasts. It ties together your assumptions around fair value, future growth, and profitability with the data.

Narratives turn complex numbers into an understandable storyline, linking CRISPR Therapeutics’ real-life progress to the financial models and then to a clear estimate of what the stock is really worth. This approach is designed to be easy and accessible for every investor. On Simply Wall St, millions use the Community page to shape and share their Narratives.

The real power of Narratives is that they help you decide how to act, by constantly comparing your Fair Value to the price in real time. Narratives are also dynamic, updating automatically as new news, earnings reports, or analyst estimates roll in. This way, your decisions stay relevant and grounded.

For example, on CRISPR Therapeutics, one Narrative might reflect strong optimism with a high fair value based on breakthrough therapies reaching the market quickly, while another shows caution and a lower valuation due to regulatory and commercialization risks. This puts the full range of investor perspectives at your fingertips.

Do you think there's more to the story for CRISPR Therapeutics? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.