How Twilio’s 10-Year NYSE Milestone And New Goldman View At Twilio (TWLO) Has Changed Its Investment Story

Twilio TWLO | 0.00 |

- In June 2026, Twilio marked its 10th anniversary on the NYSE as CEO Khozema Shipchandler highlighted the company’s role as infrastructure for emerging AI-powered businesses and thanked its 5,500 employees and alumni for their contributions.

- Around the same time, Goldman Sachs began covering Twilio with a positive view on its position in AI-driven customer experience software and its potential for market and margin expansion, which drew fresh attention to how the business is evolving.

- We’ll now explore how Goldman Sachs’ upbeat initiation, centered on Twilio’s AI-driven customer engagement role, may influence the existing investment narrative.

The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Twilio Investment Narrative Recap

To own Twilio, you need to believe it can turn its AI-centric customer engagement platform into a higher margin, software-led business while keeping core messaging growth intact. Goldman Sachs’ new positive coverage and Twilio’s 10-year NYSE milestone both reinforce that AI role, but they do not fundamentally change the near term focus on improving margins or the key risk that communications revenue mix and carrier fees could still weigh on profitability.

The SIGNAL launch of Conversation Memory, Orchestrator, Intelligence, and Agent Connect feels especially relevant here, because it shows how Twilio is trying to move deeper into AI orchestration rather than just selling raw messaging. For investors watching Goldman’s initiation, these products sit at the heart of the main catalyst: shifting more of Twilio’s revenue toward higher value, stickier software that could help offset margin pressure from commoditized messaging over time.

Yet even with AI momentum, investors should be aware that rising regulatory and privacy costs could still challenge Twilio’s long term margin story...

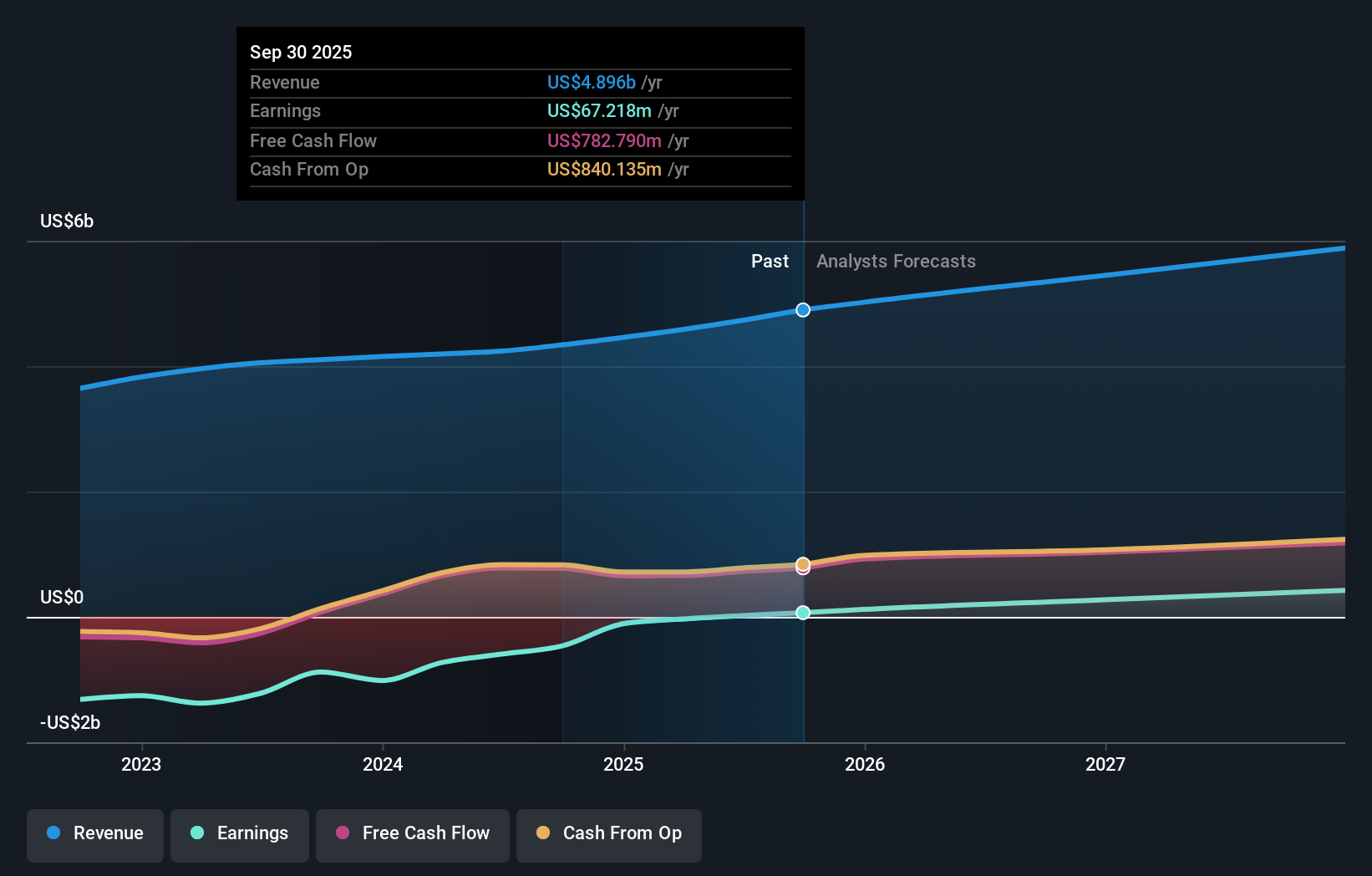

Twilio's narrative projects $5.9 billion revenue and $449.9 million earnings by 2028. This requires 7.9% yearly revenue growth and about a $429.7 million earnings increase from $20.2 million today.

Uncover how Twilio's forecasts yield a $143.14 fair value, a 24% downside to its current price.

Exploring Other Perspectives

Before this latest news, the most optimistic analysts were already projecting Twilio earnings of about US$940.4 million by 2029, so if you are weighing that against Goldman’s upbeat view and the risk that large enterprise customers might still build more in house, it is worth recognizing just how much more optimistic those forecasts are and how much they may shift as Twilio’s AI story keeps unfolding.

Explore 5 other fair value estimates on Twilio - why the stock might be worth 24% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Twilio research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Twilio research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Twilio's overall financial health at a glance.

Looking For Alternative Opportunities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.