How Twilio’s (TWLO) Launch of Advanced Data Features Could Reshape Its Investment Story

Twilio, Inc. Class A TWLO | 125.82 | +4.00% |

- Earlier this month, Twilio announced the global launch of a suite of advanced data features, including granular observability, a centralized alerting hub, expanded APIs, and no-code auto-instrumentation, all aimed at improving customer data infrastructure and experience for enterprises.

- This rollout enables enterprises to catch and resolve data issues rapidly, reduce manual work, and ensure reliable, campaign-ready data while optimizing for compliance and operational efficiency.

- We'll examine how Twilio's expanded observability and automation features could shift the company's investment narrative and long-term margins.

Find companies with promising cash flow potential yet trading below their fair value.

Twilio Investment Narrative Recap

To be a Twilio shareholder, you need to believe customer data reliability and integration will underpin long-term growth as enterprises accelerate digital transformation. The latest launch of advanced data features, while enhancing trust in Twilio’s enterprise software, does not materially shift the immediate catalyst: transitioning more revenue toward higher-margin software within the Segment/CDP business. The biggest risk remains persistent pressure on gross margins from low-margin messaging revenue and carrier fee increases, which this update does little to offset in the short term.

Among recent announcements, Twilio’s October 15 rollout of granular observability and a centralized alerting hub is most relevant, targeting data quality and compliance pain points for enterprise customers. These enhancements are closely tied to Twilio’s ambition to drive software adoption and higher margins over time, as reliable customer data and reduced manual work are increasingly cited as must-haves by enterprises considering platform investment.

Yet, on the other hand, investors should also be aware that ongoing carrier fee hikes and a rising mix of international messaging revenue could impact margins even as the company...

Twilio's narrative projects $5.9 billion revenue and $449.9 million earnings by 2028. This requires 7.9% yearly revenue growth and a $429.7 million increase in earnings from the current $20.2 million.

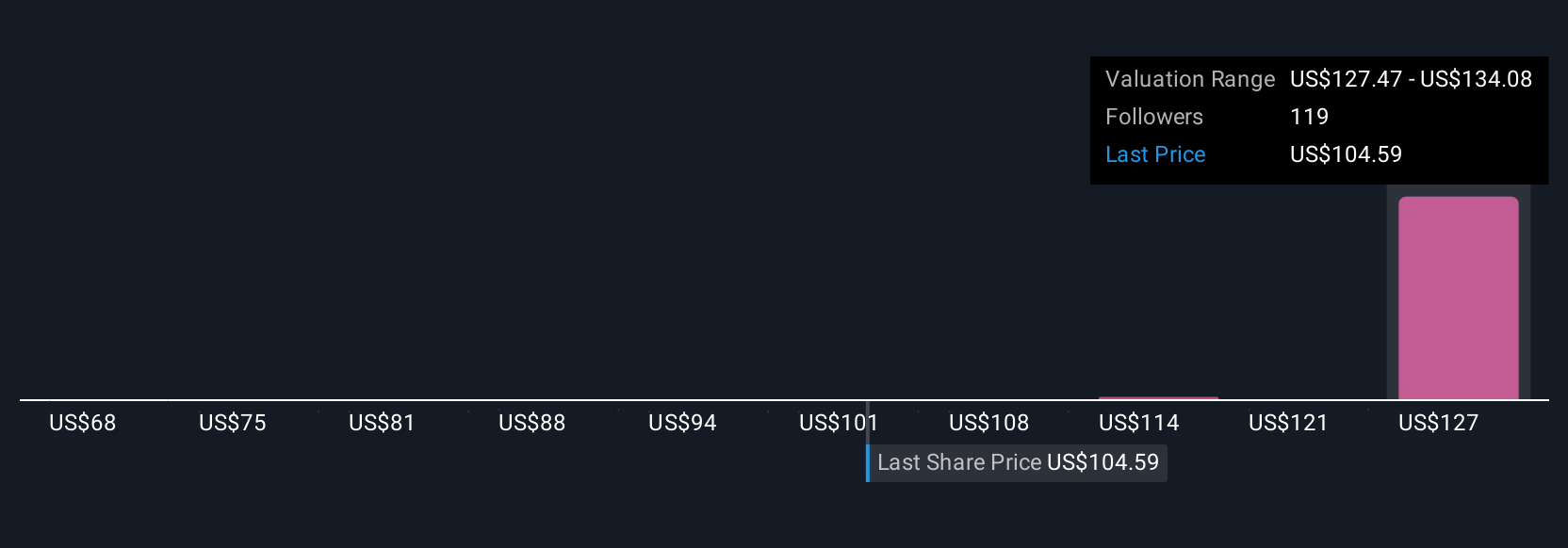

Uncover how Twilio's forecasts yield a $130.88 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Six fair value estimates from the Simply Wall St Community range from US$68 to US$131.53, highlighting a wide spread of perspectives. Keep in mind, margin risks from low-margin messaging and fee increases could weigh on future profitability, an important factor for anyone seeking broader viewpoints on Twilio's outlook.

Explore 6 other fair value estimates on Twilio - why the stock might be worth as much as 18% more than the current price!

Build Your Own Twilio Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Twilio research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Twilio research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Twilio's overall financial health at a glance.

Seeking Other Investments?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.