How UnitedHealth’s Margin Gains and Prior Authorization Cuts Could Impact UnitedHealth Group (UNH) Investors

UnitedHealth Group Incorporated UNH | 0.00 |

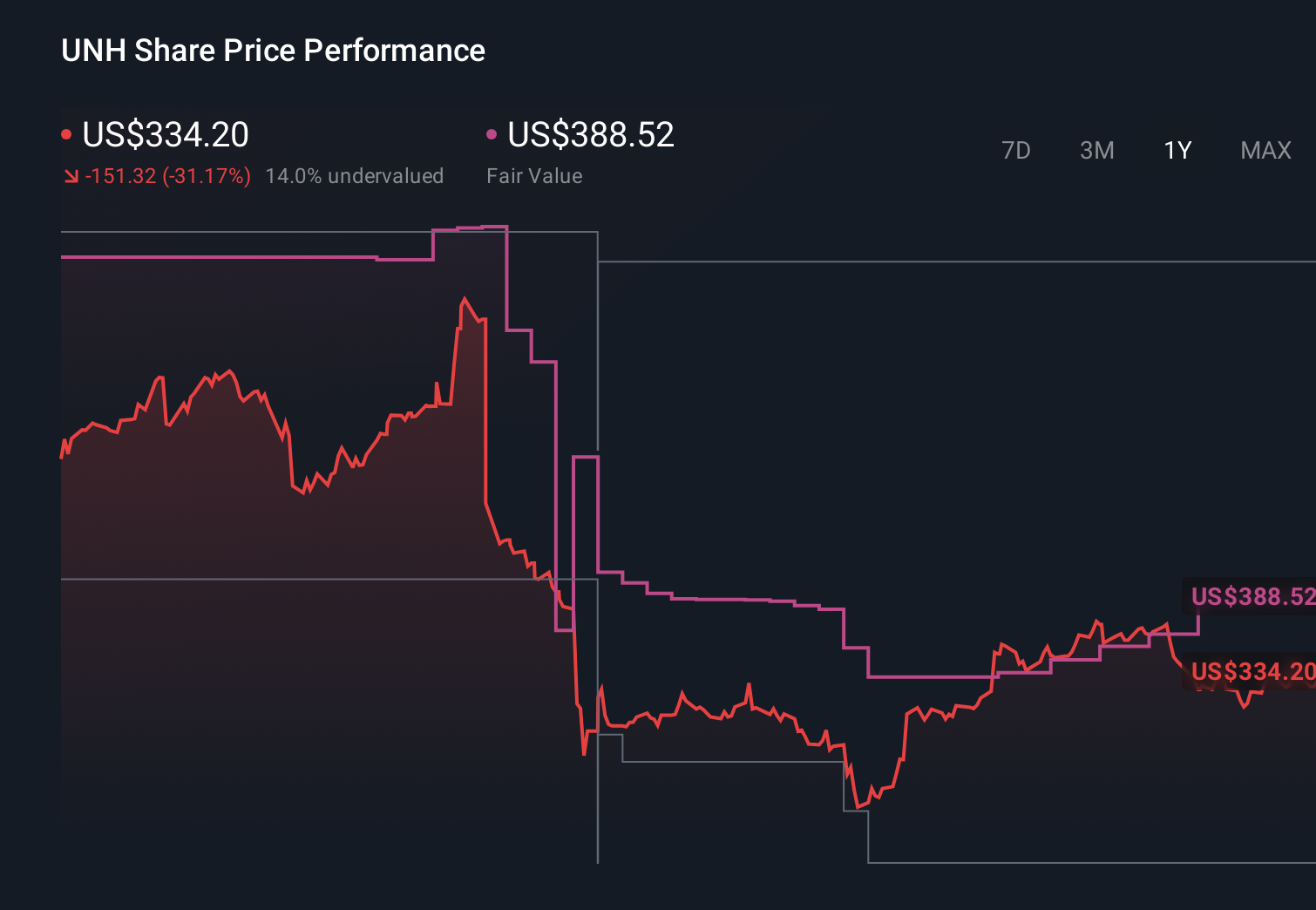

- In recent weeks, UnitedHealth Group reported Q1 2026 results showing revenues of US$111.70 billion and net earnings of US$6.48 billion, while also outlining portfolio divestitures, pending acquisitions, share repurchases, and plans to remove prior authorization requirements for a significant share of services by 2026.

- These moves, alongside improved margins, updated 2026 guidance and efforts to simplify care approvals, highlight how UnitedHealth is reshaping its operations to address cost pressures, regulatory shifts and member mix challenges across Medicare and other businesses.

- We’ll now examine how UnitedHealth’s stronger margins and plan to cut prior authorizations could influence its longer-term investment narrative.

The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

UnitedHealth Group Investment Narrative Recap

To own UnitedHealth, you generally need to believe it can manage medical cost trends and Medicare policy shifts while keeping margins under control. The latest Q1 2026 results and guidance lift suggest the near term catalyst is margin recovery, while the biggest risk remains higher than expected care utilization and funding pressure in Medicare. The new prior authorization cuts look directionally important but do not, on their own, materially change that core risk reward balance in the short term.

The most relevant update here is UnitedHealthcare’s plan to remove prior authorization requirements for 60% of currently affected services by the end of 2026. That decision sits right at the intersection of today’s key catalysts: efforts to simplify care, potentially trim administrative friction and support provider relationships, while still defending margins in Medicare and Optum. How this shift interacts with utilization trends and pricing decisions will be important to watch.

Yet even as margins improved, there is a separate risk around escalating healthcare costs that investors should be aware of...

UnitedHealth Group's narrative projects $492.0 billion revenue and $21.1 billion earnings by 2029. This requires 3.0% yearly revenue growth and a $9.1 billion earnings increase from $12.0 billion today.

Uncover how UnitedHealth Group's forecasts yield a $386.08 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming UnitedHealth could lift earnings to about US$23.1 billion by 2029, but the new authorizations policy and ongoing cost pressures show just how far apart reasonable views can be and why you should weigh several different scenarios before deciding what you believe about the stock’s long term potential.

Explore 87 other fair value estimates on UnitedHealth Group - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your UnitedHealth Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free UnitedHealth Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate UnitedHealth Group's overall financial health at a glance.

Ready For A Different Approach?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 40 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.