How UnitedHealth's Medicare Advantage Cuts and Margin Gains May Impact UnitedHealth Group (UNH) Investors

UnitedHealth Group Incorporated UNH | 0.00 |

- Earlier this week, UnitedHealth Group presented at the Bank of America Global Healthcare Conference 2026 in Las Vegas, outlining its latest operating and Medicare Advantage decisions following a strong first-quarter earnings beat and margin improvement.

- The company’s choice to cut around 1.3 million Medicare Advantage members to protect profitability, while managing regulatory and cyber-related headwinds, highlights how actively it is reshaping its business mix and risk profile.

- We’ll now examine how the Medicare Advantage membership cuts and improving margins may influence UnitedHealth Group’s multi‑year investment narrative.

AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

UnitedHealth Group Investment Narrative Recap

To own UnitedHealth Group today, you have to be comfortable with a business that is actively trading Medicare Advantage volume for margin quality, while still carrying meaningful regulatory and cyber-related overhangs. The key near term catalyst remains whether margin improvements stick after cutting roughly 1.3 million Medicare Advantage members; the biggest current risk is that future CMS decisions and regulatory actions further pressure that same Medicare Advantage profit pool. This week’s conference comments largely reinforced, rather than changed, that near term setup.

Among recent developments, the first quarter 2026 earnings beat, with revenue of US$111,721 million and higher operating margins, is most relevant to these Medicare decisions. The improved medical care ratio, helped by exiting less profitable Medicare Advantage markets, shows how membership cuts are feeding directly into short term profitability. How durable that margin lift proves to be will matter a lot more now that investor attention is firmly on underwriting discipline and regulatory pushback.

Yet, against this improving margin story, the lingering DOJ actions and cyberattack fallout could still surprise investors who are not watching closely...

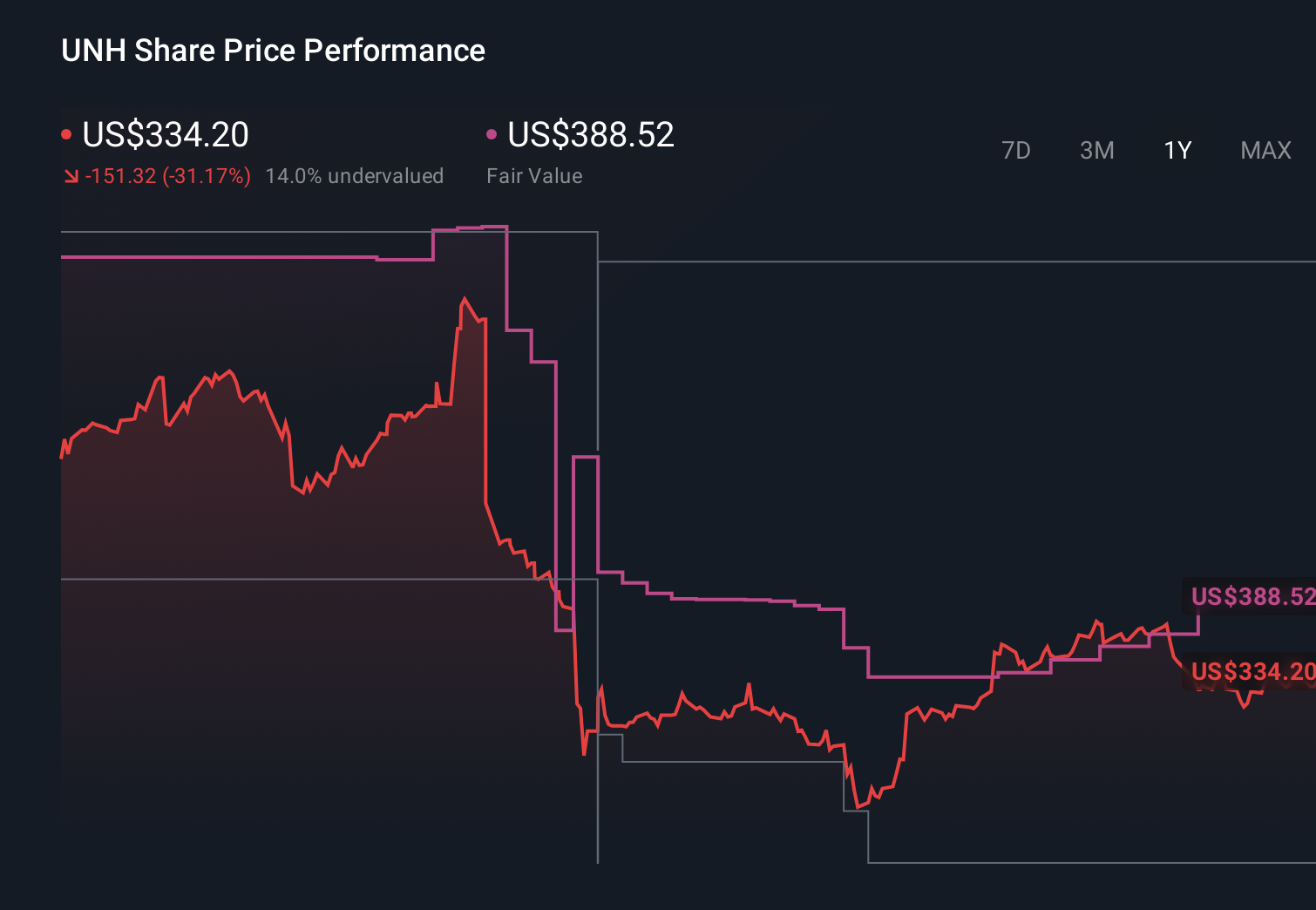

UnitedHealth Group's narrative projects $492.0 billion revenue and $21.1 billion earnings by 2029. This requires 3.0% yearly revenue growth and a $9.1 billion earnings increase from $12.0 billion today.

Uncover how UnitedHealth Group's forecasts yield a $386.08 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were penciling in roughly US$509,100 million of revenue and US$23,100 million of earnings by 2029, which is far more upbeat than the baseline view. When you compare that to the current focus on Medicare Advantage cuts and regulatory strain, you can see how sharply opinions differ and why both sets of assumptions may need revisiting after this latest news.

Explore 74 other fair value estimates on UnitedHealth Group - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your UnitedHealth Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free UnitedHealth Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate UnitedHealth Group's overall financial health at a glance.

Ready For A Different Approach?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.