How V2X’s (VVX) Cheaper Term Loan Repricing Has Changed Its Investment Story

V2X VVX | 0.00 |

- In early June 2026, V2X, Inc. announced it had successfully repriced its approximately $869 million First Lien Term Loan, cutting the interest margin to SOFR plus 2.0% and removing the 0.75% SOFR floor, with an additional 0.25% rate reduction contingent on achieving specified Moody’s and S&P credit ratings.

- This fourth repricing since October 2023 highlights management’s focus on lowering financing costs and strengthening the balance sheet, potentially enhancing cash flow available for operations and growth initiatives.

- Next, we’ll examine how this lower-cost, more flexible debt structure could influence V2X’s investment narrative and future financial profile.

The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

V2X Investment Narrative Recap

To own V2X, you need to believe its growing defense and modernization pipeline can offset contract timing swings and execution risk on large, fixed price programs. In the near term, the key catalyst is converting its US$50 billion pipeline into awards that rebuild backlog, while the biggest risk is continued lumpiness in bookings and protests around major contracts. The latest term loan repricing reduces interest expense but does not materially change these operational swing factors.

The repricing follows V2X’s Q1 2026 results, where the company raised full year revenue guidance to US$4,825 million to US$4,975 million. Together, better operating performance and lower borrowing costs may improve financial flexibility just as the company ramps recent awards like T 6 training, LAIRCM integration, and CJADC2 related programs, all of which could influence how quickly earnings and cash generation track toward consensus expectations.

Yet behind this improved financing picture, investors should still be aware of how protest risk and heavy reliance on large, binary awards could...

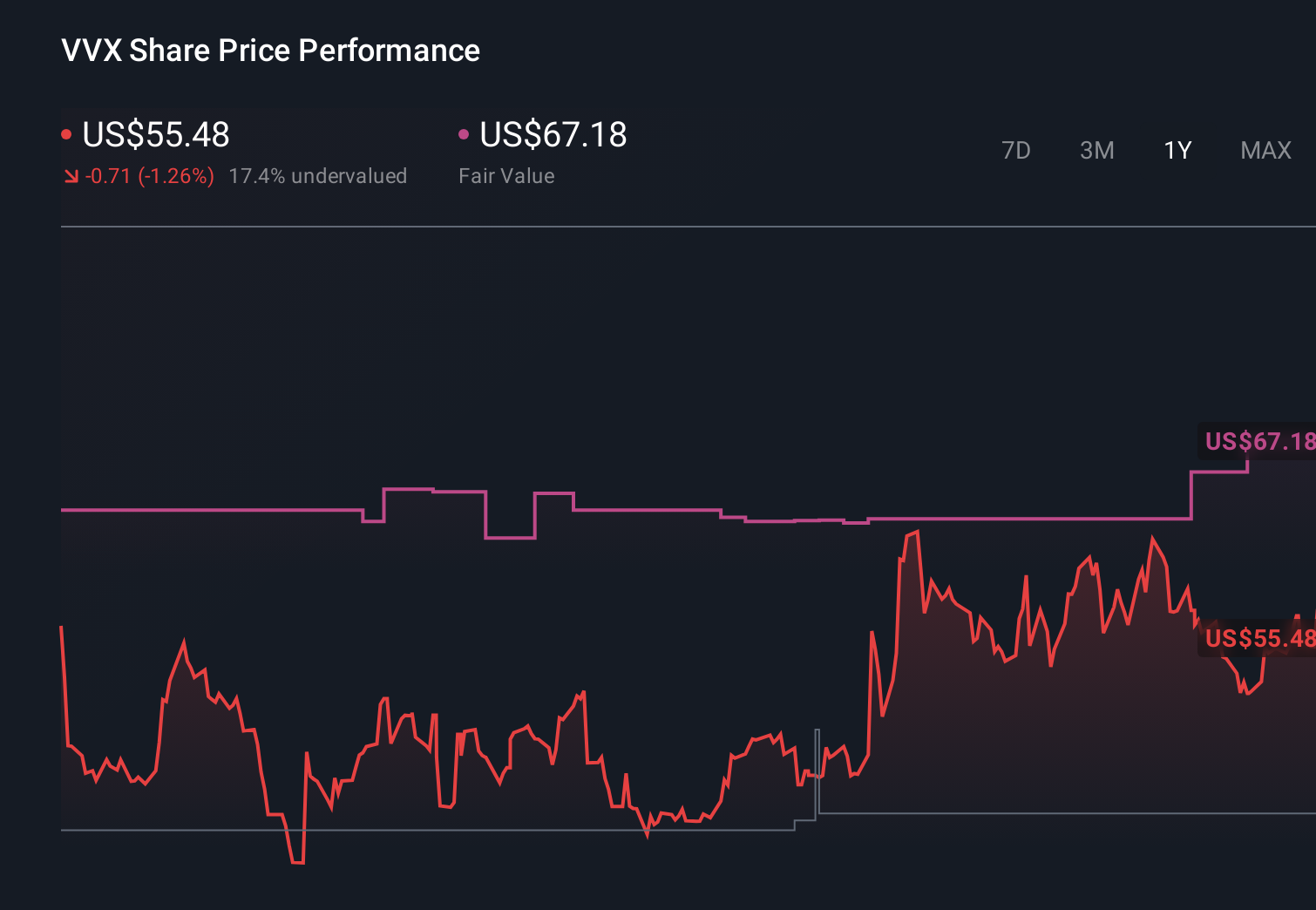

V2X's narrative projects $5.5 billion revenue and $196.9 million earnings by 2029. This implies 5.1% yearly revenue growth and about a $108 million earnings increase from $88.7 million today.

Uncover how V2X's forecasts yield a $79.42 fair value, a 7% downside to its current price.

Exploring Other Perspectives

Some of the most cautious analysts see more risk than the latest debt repricing implies, even as they still project revenue of about US$5.3 billion and earnings near US$142 million by 2029, because they worry that rising automation could steadily undercut V2X’s labor intensive contracts while higher costs and budget shifts pressure margins.

Explore 3 other fair value estimates on V2X - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your V2X research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free V2X research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate V2X's overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.