How Valuation Concerns and Insider Selling At MasTec (MTZ) Has Changed Its Investment Story

MasTec, Inc. MTZ | 0.00 |

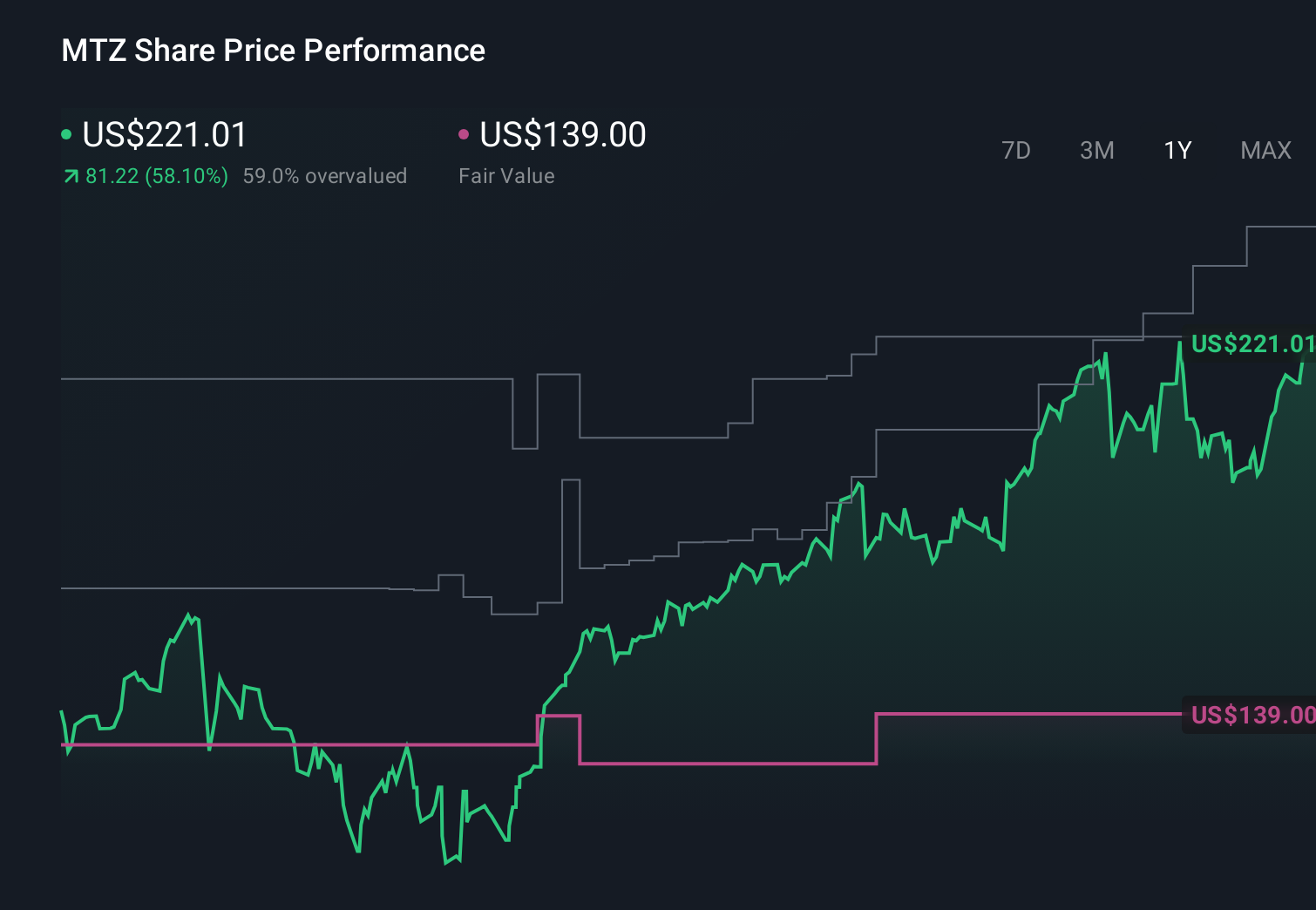

- In early June 2026, MasTec drew attention as valuation services flagged the stock as significantly overvalued and insider sales reached about US$3.5 million over three months with no offsetting insider purchases.

- This combination of valuation concerns and insider activity has sharpened investor focus on how MasTec’s growth opportunities in grid, data center, and clean energy projects balance against perceived risk.

- We’ll now examine how insider selling alongside strong infrastructure demand trends may influence MasTec’s existing investment narrative and risk profile.

Find 47 companies with promising cash flow potential yet trading below their fair value.

MasTec Investment Narrative Recap

To own MasTec, you need to believe that long term demand for grid, data center, and clean energy infrastructure can support its current valuation and capital intensity. The recent flagging of MasTec as “significantly overvalued,” combined with about US$3.5 million in insider sales and no insider buying, heightens near term focus on valuation risk rather than altering the core demand story. For now, it mostly amplifies the existing concern that high expectations could magnify any setback in project timing or execution.

The most relevant recent announcement is MasTec’s Q1 2026 update on 30 April, where the company reported higher revenue and earnings year over year and raised full year 2026 guidance to US$17,500 million in revenue and US$575 million in GAAP net income. That stronger outlook underpins the bull case that record backlog and robust infrastructure spending can offset valuation concerns, but it also means any disappointment on grid, communications, or clean energy projects now has more to lose.

Yet even with strong demand tailwinds, investors should be aware that concentrated customer exposure and project execution risks could quickly matter more if sentiment shifts...

MasTec's narrative projects $20.3 billion revenue and $880.9 million earnings by 2029.

Uncover how MasTec's forecasts yield a $348.72 fair value, a 6% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts already took a tougher view, assuming revenue of about US$21.6 billion and earnings near US$848.8 million by 2029, and warning that if non pipeline demand softens or projects slip, MasTec’s rich starting point could look far less comfortable, which is a useful reminder that your own view should sit within a wide range of possible outcomes.

Explore 6 other fair value estimates on MasTec - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your MasTec research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free MasTec research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MasTec's overall financial health at a glance.

No Opportunity In MasTec?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 32 best rare earth metal stocks of the very few that mine this essential strategic resource.

- This technology could replace computers: discover 29 stocks that are working to make quantum computing a reality.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.