How Viasat’s (VSAT) Atos-Led Workplace Overhaul Could Shape Its Cash Efficiency Story

ViaSat, Inc. VSAT | 0.00 |

- Earlier this week, Atos announced it had been selected by Viasat to run a multi-year digital workplace modernization program across Viasat’s U.S. and global operations, aiming to enhance service desk support, advanced services, and intelligent collaboration tools.

- At the same time, questions around Viasat’s cash usage, returns on capital, and high valuation versus certain fair value estimates are adding extra scrutiny to how effectively such modernization efforts can support its longer-term business resilience.

- Next, we’ll examine how concerns about cash burn and capital efficiency may alter Viasat’s pre-existing investment narrative around growth and scale.

Uncover the next big thing with 28 elite penny stocks that balance risk and reward.

Viasat Investment Narrative Recap

To own Viasat, you need to believe its global satellite network, defense exposure, and ViaSat 3 rollout can ultimately outweigh current losses, high capital intensity, and fierce LEO competition. The Atos workplace modernization deal looks incrementally helpful for execution and cost control, but it does not clearly change the main near term catalyst, which is how quickly ViaSat 3 and Inmarsat assets translate into cash generation, or the key risk around ongoing cash burn and leverage.

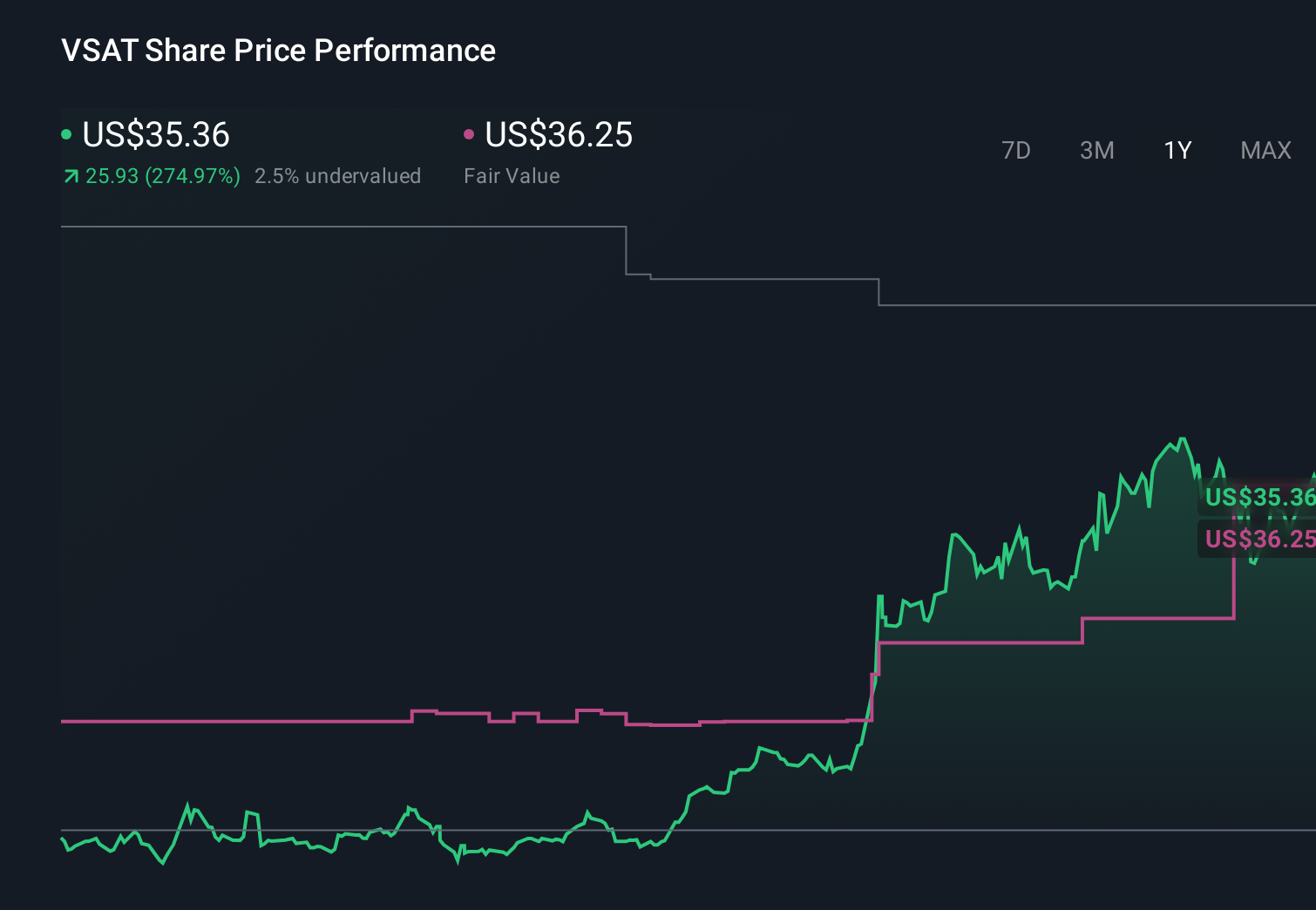

Among recent developments, the sharp share price move to US$75.29, far above one fair value estimate of US$18.32, feels most relevant here. That disconnect puts extra focus on whether operational upgrades, like the Atos partnership, can support better capital efficiency and earnings quality quickly enough to justify a premium multiple while Viasat remains unprofitable and continues to invest heavily.

Yet behind the optimism around modernization and global bandwidth expansion, investors should be aware of how persistent cash burn and high CapEx could...

Viasat's narrative projects $5.1 billion revenue and $557.4 million earnings by 2029.

Uncover how Viasat's forecasts yield a $51.14 fair value, a 28% downside to its current price.

Exploring Other Perspectives

While consensus stays cautious, the most optimistic analysts once modeled revenue of about US$5.1 billion and earnings near US$569 million, assuming integration risks and LEO competition ease rather than intensify, so you may want to weigh how this new deal affects which version of Viasat’s future feels more realistic.

Explore 8 other fair value estimates on Viasat - why the stock might be worth 32% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Viasat research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Viasat research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Viasat's overall financial health at a glance.

Looking For Alternative Opportunities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.