How Westlake’s US$67 Million PVC Settlement At Westlake (WLK) Has Changed Its Investment Story

Westlake Corporation WLK | 112.61 | -5.37% |

- Westlake Corporation has entered into a settlement agreement with direct purchaser plaintiffs in the PVC Pipe Antitrust Litigation, agreeing to pay US$67 million, subject to court approval, while related indirect purchaser claims remain unresolved.

- This settlement helps clarify a key legal overhang tied to Westlake’s PVC pipe and fittings business, an important part of its Housing and Infrastructure Products segment.

- We will now examine how resolving a significant portion of this antitrust litigation could influence Westlake’s investment narrative and perceived risk profile.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

Westlake Investment Narrative Recap

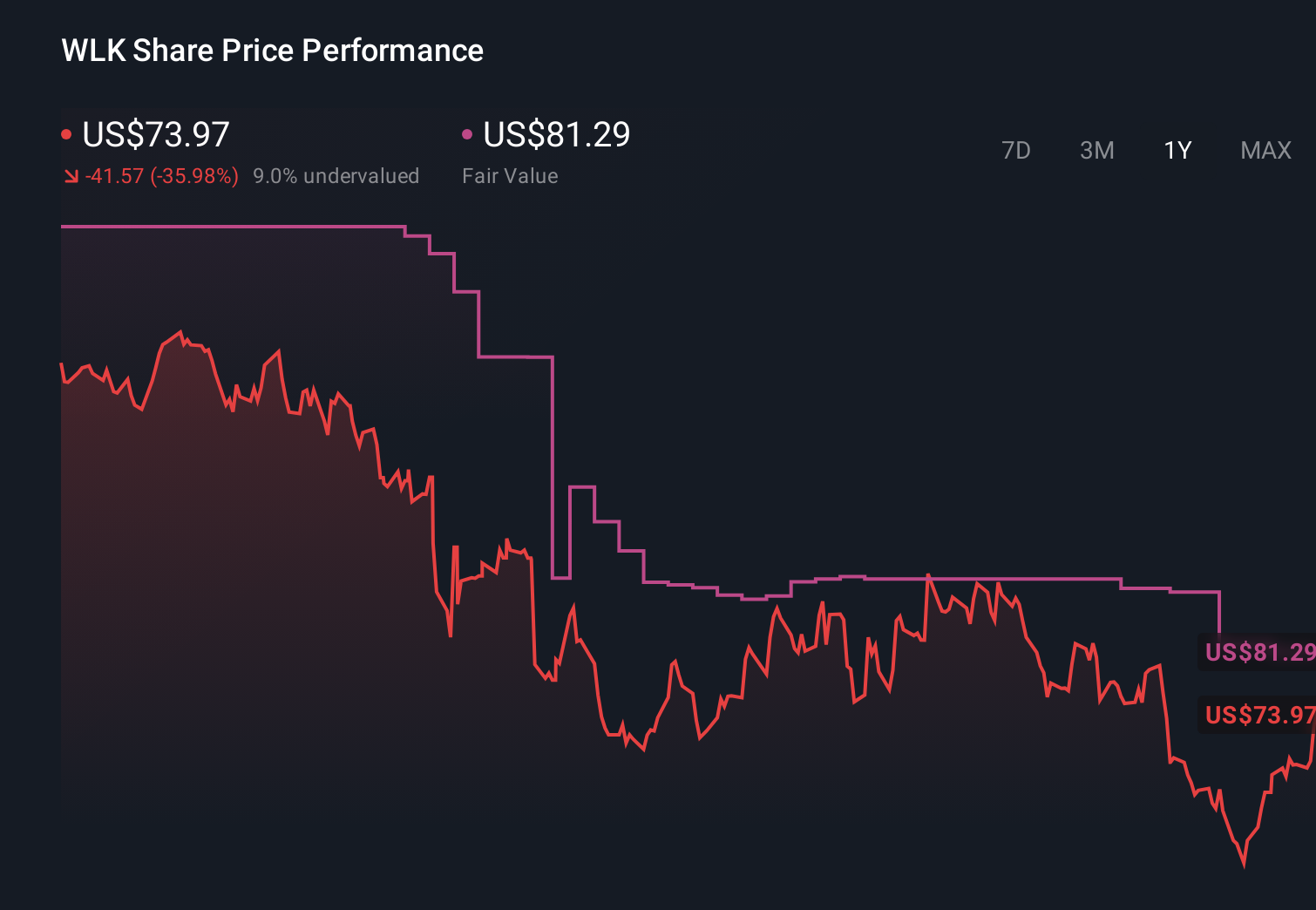

To own Westlake, you need to believe its mix of commodity chemicals and housing and infrastructure products can support a credible path back to profitability after recent losses. The US$67 million PVC pipe settlement, if approved, helps reduce legal uncertainty around a key part of the Housing and Infrastructure Products segment, but it does not change that the core near term catalyst remains execution on cost reduction and asset optimization, while the biggest risk is still sustained margin pressure in Performance and Essential Materials.

The new US$1.5 billion unsecured revolving credit facility is the most relevant recent announcement here, because it reinforces Westlake’s liquidity and financial flexibility at the same time it commits cash to resolve part of the antitrust litigation. That access to committed funding could matter if weak pricing, higher input costs or remaining legal exposures put further strain on cash flows before earnings recover, and it gives the company room to keep investing behind its operational plans.

Yet investors should not ignore how unresolved legal claims and ongoing industry overcapacity could still affect Westlake’s margins and cash flows...

Westlake's narrative projects $12.6 billion revenue and $364.4 million earnings by 2029. This requires 4.2% yearly revenue growth and an earnings increase of about $1.9 billion from -$1.5 billion today.

Uncover how Westlake's forecasts yield a $117.07 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming revenue near US$13.3 billion and earnings of about US$546 million by 2029, which is far more upbeat than the baseline cost pressure risk you just read about. This new legal update could push those expectations higher or lower, so it is worth comparing how your own view on the remaining antitrust exposure lines up with these more hopeful forecasts.

Explore 3 other fair value estimates on Westlake - why the stock might be worth 39% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Westlake research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Westlake research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Westlake's overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with 29 elite penny stocks that balance risk and reward.

- Outshine the giants: these 19 early-stage AI stocks could fund your retirement.

- Find 60 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.