How WTW’s Qover Partnership in Embedded Insurance Could Reshape Its Digital Distribution Strategy (WTW)

Willis Towers Watson WTW | 0.00 |

- Willis, a WTW business, recently expanded its GB Affinity technology ecosystem by announcing a partnership with Qover, a European embedded insurance orchestration provider, to help UK businesses integrate tailored, product-agnostic insurance directly into customer journeys across sectors such as finance, retail, automotive, and membership organisations.

- This collaboration combines Qover’s APIs, real-time dashboards, and AI-enhanced claims tools with Willis’s pricing and analytics capabilities, including Radar, potentially deepening its position in embedded insurance and digital distribution solutions.

- Next, we’ll examine how this embedded insurance partnership, built on Willis’s Radar analytics platform, could influence Willis Towers Watson’s broader investment narrative.

We've uncovered the 15 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Willis Towers Watson Investment Narrative Recap

To own Willis Towers Watson, you need to believe in its ability to compound value through higher margin, tech-enabled risk and advisory services while managing competition and regulation. The Qover embedded insurance partnership appears directionally aligned with this thesis but does not meaningfully change the near term focus on differentiating its core broking and consulting offerings or the ongoing risk that digital tools could compress pricing and fees.

The Qover announcement also sits alongside WTW’s continued build out of its Radar platform, including recent connectors for Databricks and Snowflake and the launch of Radar Fusion. Together, these moves keep execution risk in focus, as WTW works to integrate advanced analytics across broking, underwriting and affinity channels without materially inflating costs or diluting its service quality.

Yet beneath the appeal of embedded insurance and advanced analytics, investors should be aware of the risk that accelerating AI adoption could...

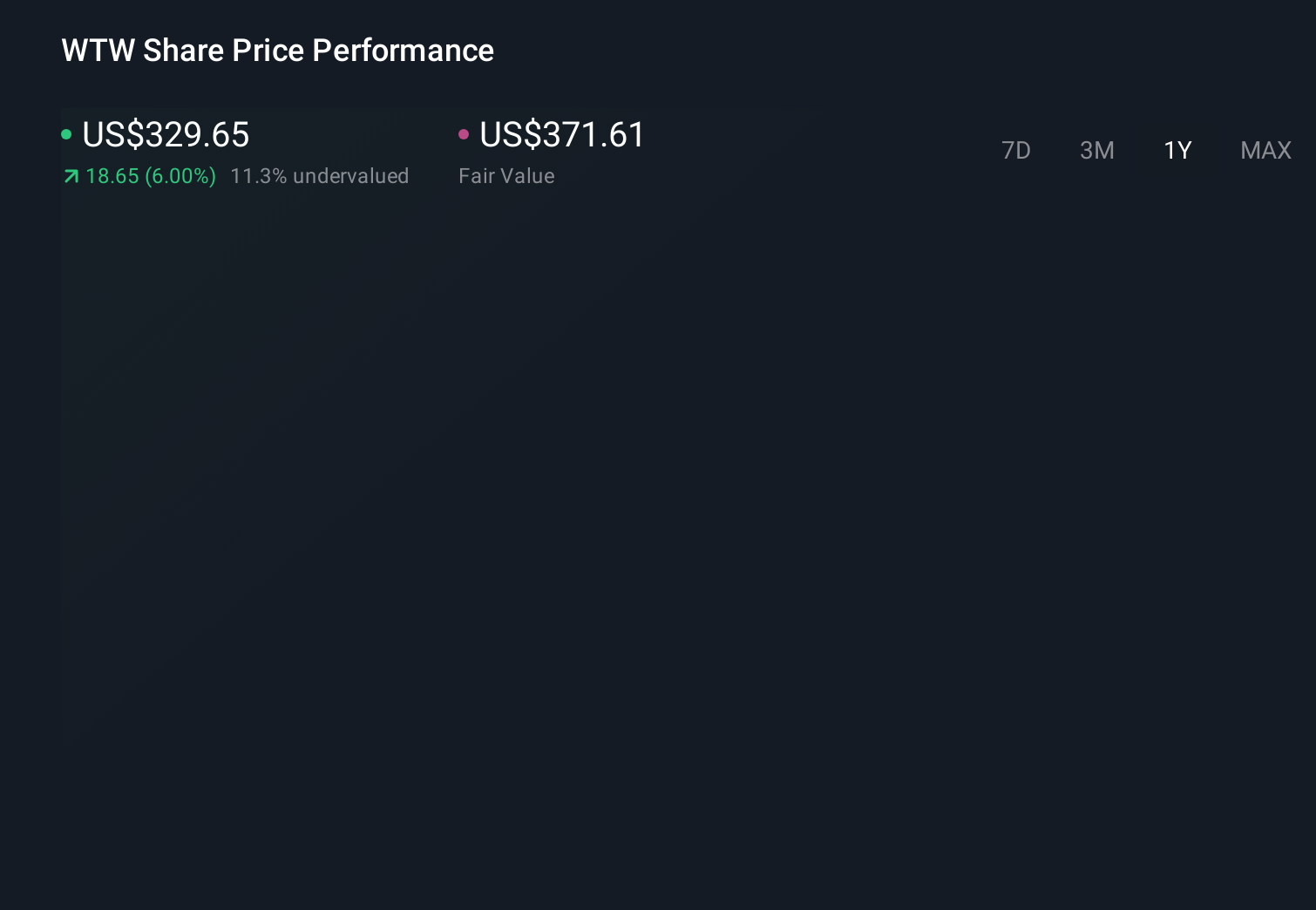

Willis Towers Watson's narrative projects $10.9 billion revenue and $2.5 billion earnings by 2028.

Uncover how Willis Towers Watson's forecasts yield a $369.42 fair value, a 27% upside to its current price.

Exploring Other Perspectives

Two Simply Wall St Community fair value estimates span roughly US$187 to US$369 per share, showing very different expectations for WTW’s potential. Against this spread, WTW’s push into embedded insurance and broader digital solutions puts execution and differentiation risks at the center of its future performance, so it is worth weighing several viewpoints before forming your own.

Explore 2 other fair value estimates on Willis Towers Watson - why the stock might be worth 36% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Willis Towers Watson research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Willis Towers Watson research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Willis Towers Watson's overall financial health at a glance.

Want Some Alternatives?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Rare earth metals are the new gold rush. Find out which 28 stocks are leading the charge.

- Invest in the nuclear renaissance through our list of 87 elite nuclear energy infrastructure plays powering the global AI revolution.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 21 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.