Huntington (HBAN) Is Down 5.9% After Outsourcing Wealth Unit And Issuing 2027 Guidance - Has The Bull Case Changed?

Huntington Bancshares Incorporated HBAN | 15.79 | -0.57% |

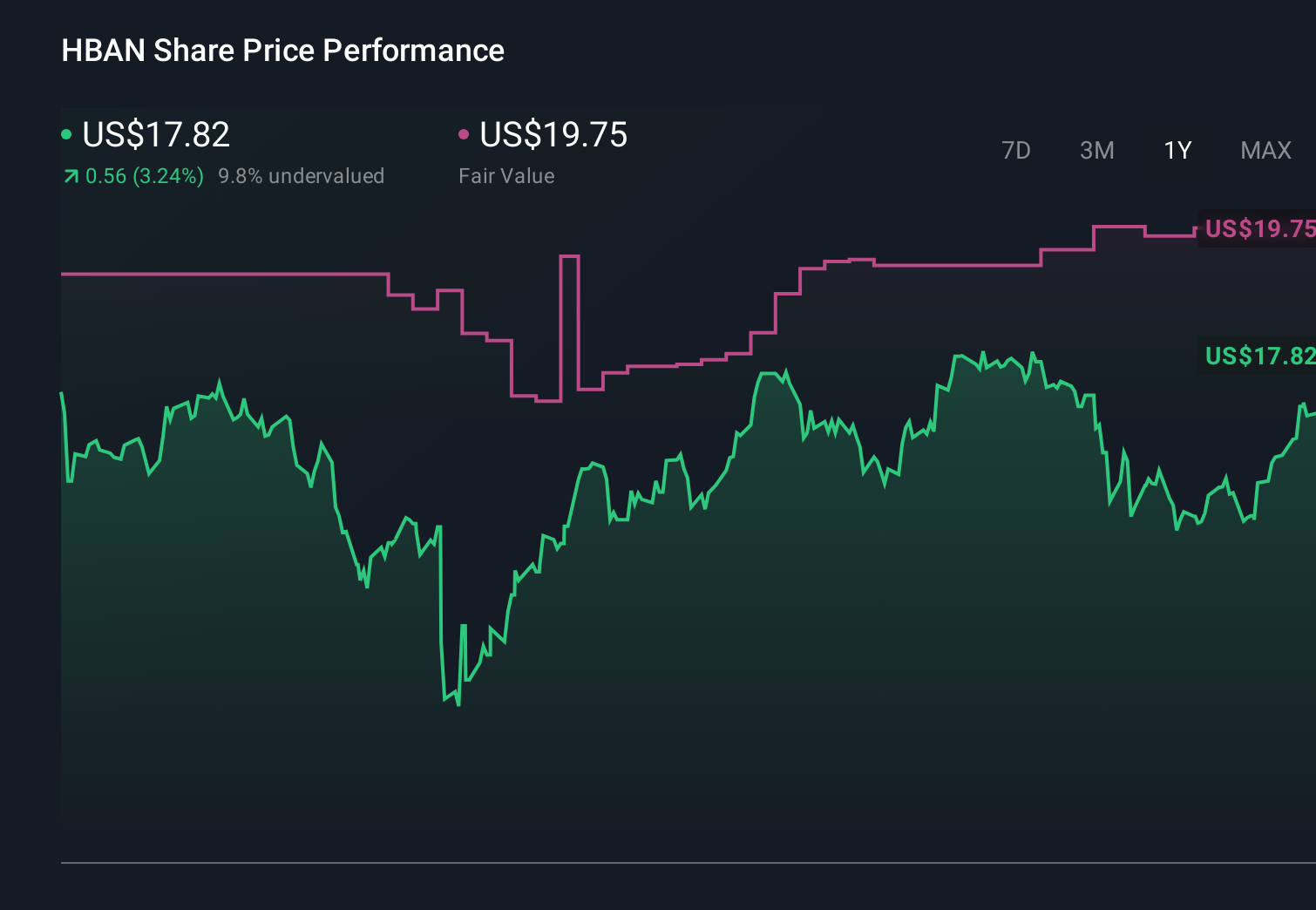

- In February 2026, Huntington Bancshares announced it will outsource its approximately US$28.00 billion wealth management business to Ameriprise, while recent disclosures show no shares were repurchased under its 2025 buyback authorization and the bank issued 2027 guidance of about US$12.60 billion in revenue with earnings per share of US$1.90–US$1.93.

- This reshaping of Huntington’s wealth offering and board, through the addition of former Cadence Bank directors, marks a meaningful shift in how the post‑merger bank organizes its operations, governance, and long‑term priorities.

- We’ll now examine how outsourcing Huntington’s sizeable wealth management business to Ameriprise could alter the bank’s previously framed investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Huntington Bancshares Investment Narrative Recap

To own Huntington Bancshares, you need to be comfortable with a regional bank that is reshaping its mix of fee and interest income while expanding beyond its Midwest core. The Ameriprise outsourcing of the US$28.00 billion wealth unit and the absence of 2025 buybacks do not appear to change the near term focus on executing acquisitions and managing integration risk, which still feels like the most important swing factor alongside interest margin pressure.

The 2027 guidance of about US$12.60 billion in revenue and earnings per share of US$1.90 to US$1.93 looks particularly relevant here, because it sets a reference point for how much Huntington expects to deliver after reconfiguring its wealth business and board. For investors watching catalysts around efficiency and expansion into faster growing markets, these targets provide a concrete yardstick against which to judge whether the outsourcing decision and integration of Cadence and Veritex are helping or hindering overall performance.

Yet behind this clearer outlook, investors should be aware of the integration and overexpansion risk that could...

Huntington Bancshares' narrative projects $8.9 billion revenue and $2.3 billion earnings by 2028. This requires 7.3% yearly revenue growth and a $0.3 billion earnings increase from $2.0 billion.

Uncover how Huntington Bancshares' forecasts yield a $20.45 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span roughly US$11 to almost US$37 per share, showing very different views on Huntington’s potential. Against that wide range, the current focus on executing acquisitions in Texas and the Carolinas raises important questions about how integration risk could affect the bank’s ability to deliver on its ambitions and earnings targets.

Explore 4 other fair value estimates on Huntington Bancshares - why the stock might be worth 37% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Huntington Bancshares research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Huntington Bancshares research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Huntington Bancshares' overall financial health at a glance.

Interested In Other Possibilities?

Our top stock finds are flying under the radar-for now. Get in early:

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.