Huntsman (HUN) Valuation Check As Portfolio Shift Meets Mixed Long Term Shareholder Returns

Huntsman Corporation HUN | 0.00 |

How Huntsman’s Recent Performance Frames the Stock Today

Huntsman (HUN) has been on many investors’ radars after a mixed stretch for the stock, with recent short term weakness contrasting with stronger longer term returns. That backdrop makes its current fundamentals more relevant.

Recent share price action has softened, with a 7 day share price return of 7.43% and a 30 day share price return of 5.01%. This contrasts with a 39.45% year to date share price return and a 32.68% 1 year total shareholder return, while 3 and 5 year total shareholder returns remain more muted.

If Huntsman’s mixed track record has you thinking about diversification, it could be a good moment to scan other materials focused ideas using the 8 top copper producer stocks

With Huntsman shares close to analyst targets and a discounted view from some intrinsic models, the key question now is simple: is the stock being overlooked, or is the market already pricing in any future recovery?

Most Popular Narrative: 1% Undervalued

Huntsman’s most followed narrative places fair value at $14.31, only slightly above the last close at $14.21, which frames the stock as almost fully priced.

The company is actively transforming its portfolio away from lower-margin, commodity chemicals toward specialty chemicals (e.g., adhesives, elastomers, aerospace composites). It is aiming to further improve EBITDA margins and overall profitability in future cycles. Cost optimization, working capital discipline, and strategic asset closures (e.g., the maleic anhydride facility in Europe) are expected to enhance free cash flow generation and support improved net margins and earnings resilience during the next macro upturn.

Want to see what that portfolio shift really assumes for growth, margins, and future earnings multiples? The narrative rests on a tight mix of revenue expansion, margin repair, and a relatively low future valuation multiple, all working together to justify that fair value.

Result: Fair Value of $14.31 (ABOUT RIGHT)

However, the picture could change quickly if prolonged overcapacity in global MDI markets or sustained weakness in construction and housing demand keeps margins under pressure.

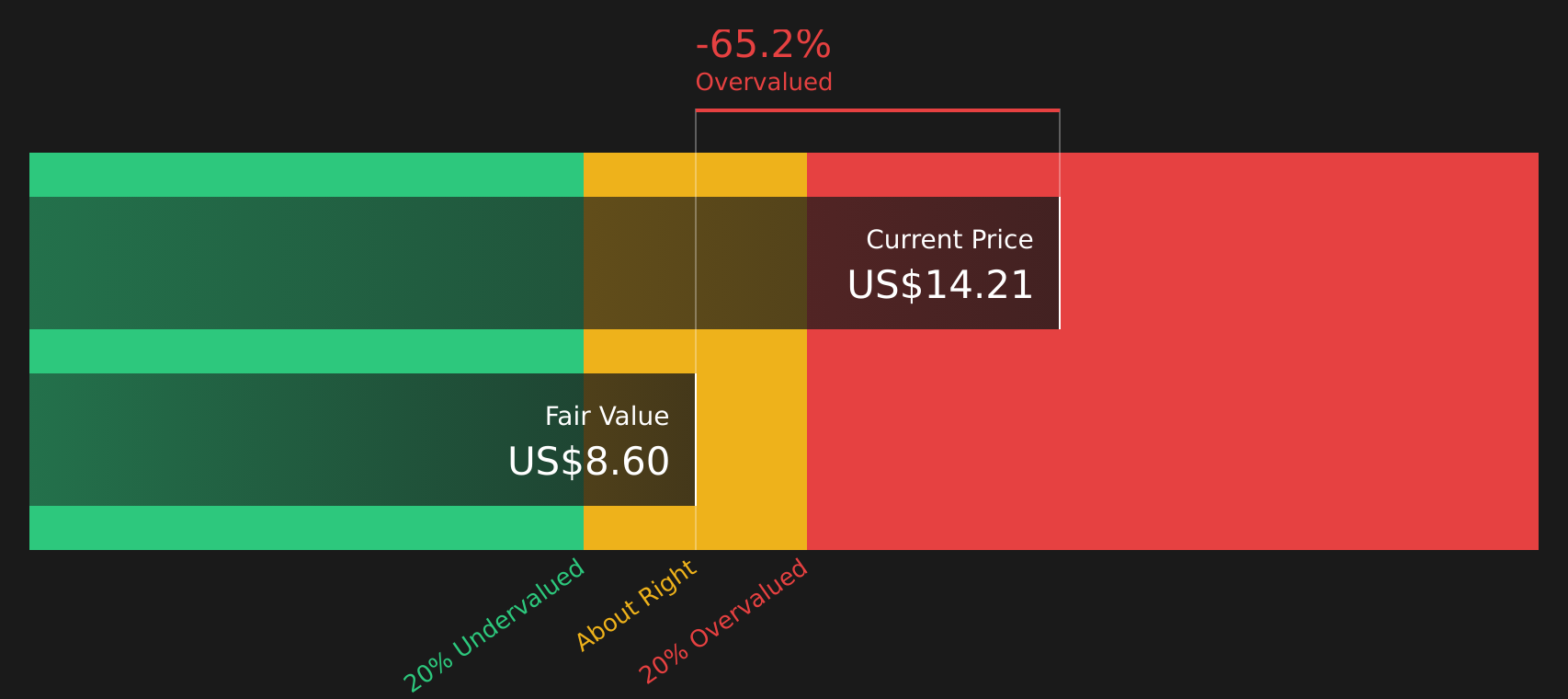

Another View: Cash Flows Paint A Tougher Picture

While the popular narrative points to fair value around $14.31, our DCF model using future cash flows tells a different story. On that basis, Huntsman is valued at about $8.60 per share, which frames the current $14.21 price as expensive. Which perspective do you find more convincing?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Huntsman for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With the mixed signals in this article, it makes sense to look at the underlying numbers, compare them with your own expectations, and move quickly to shape your view by weighing the 1 key reward and 2 important warning signs.

Looking for more investment ideas?

If Huntsman has sharpened your thinking, now is the moment to broaden your watchlist with a few focused ideas that you would not want to miss.

- Spot potential mispricing early by scanning 49 high quality undervalued stocks, which combines quality fundamentals with compressed expectations.

- Strengthen your income focus by reviewing 9 dividend fortresses, which aims to pair higher yields with resilient payouts.

- Prioritize resilience by checking 61 resilient stocks with low risk scores, which scores well on stability and financial strength.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.