Icahn Enterprises (IEP): Taking Stock of Valuation During a Quiet Period

Icahn Enterprises L.P. IEP | 7.57 | +0.26% |

Price-to-Sales Ratio of 0.5x: Is it justified?

Based on the preferred multiple of price-to-sales, Icahn Enterprises appears undervalued compared to both its global industry and peer group, trading at just 0.5 times its sales.

The price-to-sales ratio compares a company’s market value to its total revenues, serving as a classic measure of valuation in sectors where profitability may be inconsistent or negative. For Icahn Enterprises, this metric is especially relevant because the company is currently unprofitable but still generates significant revenue.

In this case, Icahn Enterprises is valued lower than peers and the broader industry. This suggests the market may be discounting its future prospects or factoring in higher risk. Whether this conservative valuation is justified depends on the company’s ability to return to profitability and halt its recent revenue decline.

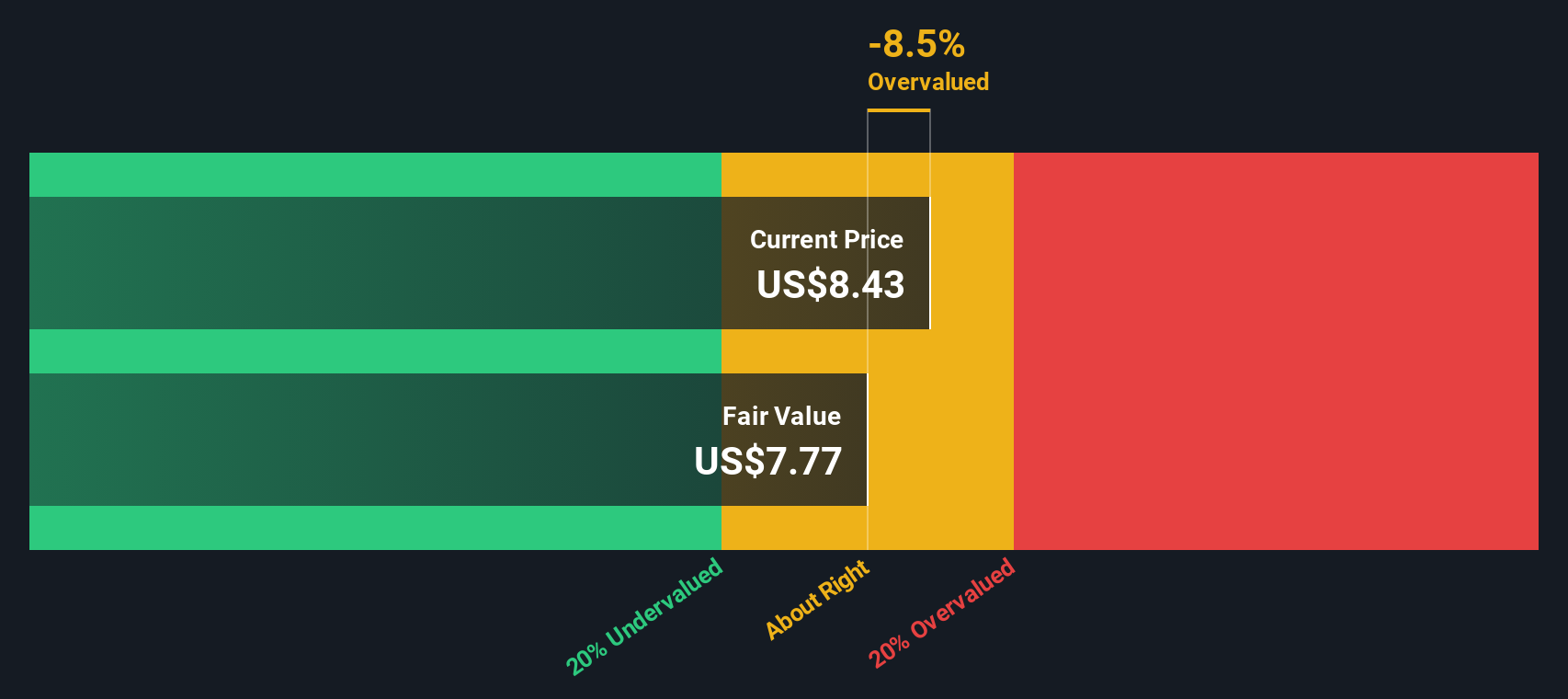

Result: Fair Value of $8.43 (UNDERVALUED)

See our latest analysis for Icahn Enterprises.However, persistent revenue declines and recent underperformance compared to the market could pose challenges for any near-term recovery in Icahn Enterprises’ valuation story.

Find out about the key risks to this Icahn Enterprises narrative.Another View: Discounted Cash Flow Challenges the Surface

While the market value looks attractive using the sales comparison, our SWS DCF model suggests a less optimistic outcome. This approach estimates the business's intrinsic worth based on future cash flows and raises questions about whether current market skeptics might be on to something. Which outlook truly tells the full story: value today, or risk ahead?

Build Your Own Icahn Enterprises Narrative

If you have a different perspective or want to dig deeper into the numbers yourself, you can shape your own view in just a few minutes with Do it your way.

A great starting point for your Icahn Enterprises research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t sit on the sidelines while new opportunities unfold. The Simply Wall Street Screener unlocks exciting stock ideas tailored to unique trends worth your attention.

- Capture early momentum in rapidly advancing technology by checking out AI-focused stocks with strong growth using AI penny stocks.

- Boost your portfolio’s income with reliable picks offering attractive yields by scanning stocks that excel in delivering over 3% dividends through dividend stocks with yields > 3%.

- Seize great value potential by finding underestimated companies trading below their cash flow worth, all surfaced for you via undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.