ICF International And 2 Other Undervalued Small Caps With Insider Buying In Global Markets

ICF International, Inc. ICFI | 0.00 |

The United States market has shown a positive trend, climbing 1.4% in the last week and 19% over the past year, with earnings anticipated to grow by 19% annually in the coming years. In this favorable environment, identifying stocks that are considered undervalued and have insider buying can be a strategic approach for investors looking to capitalize on potential growth opportunities.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Betterware de MéxicoP.I. de | 10.0x | 0.8x | 49.89% | ★★★★★★ |

| Similarweb | NA | 1.9x | 27.81% | ★★★★★☆ |

| Onterris | 170.8x | 0.9x | 26.85% | ★★★★★☆ |

| AVITA Medical | NA | 2.2x | 49.78% | ★★★★★☆ |

| Industrial Logistics Properties Trust | NA | 1.3x | 37.99% | ★★★★★☆ |

| Kingstone Companies | 9.4x | 1.3x | 35.73% | ★★★★☆☆ |

| Modiv Industrial | NA | 3.9x | 48.28% | ★★★★☆☆ |

| Patria Investments | 24.8x | 4.5x | 8.18% | ★★★☆☆☆ |

| Peoples Bancorp | 12.6x | 3.3x | 39.83% | ★★★☆☆☆ |

| Union Bankshares | 10.2x | 2.1x | 13.65% | ★★★☆☆☆ |

Let's take a closer look at a couple of our picks from the screened companies.

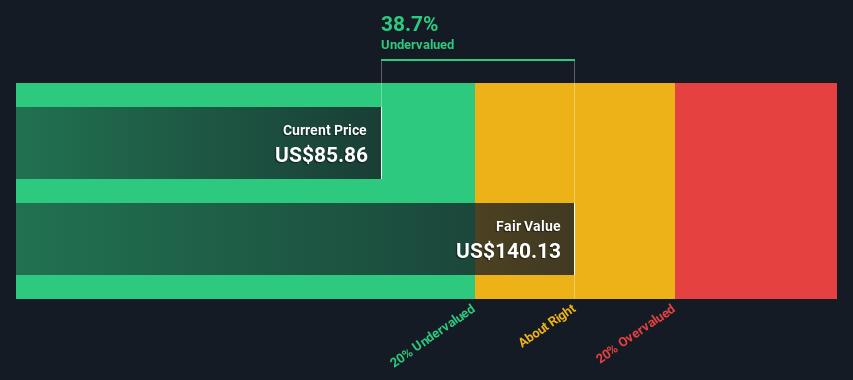

ICF International (ICFI)

Simply Wall St Value Rating: ★★★★★☆

Overview: ICF International is a global consulting and technology services company that provides professional services to a broad array of clients, with a market capitalization of approximately $2.36 billion.

Operations: ICFI generates revenue primarily through professional services, with recent figures indicating $1.82 billion in this segment. The company has experienced fluctuations in its net income margin, which was 4.68% as of March 31, 2026. Gross profit margins have shown some variation over time, standing at 37.19% for the same period. Operating expenses and cost of goods sold are significant components impacting profitability, with general and administrative expenses being a notable part of the cost structure.

PE: 15.9x

ICF International, a smaller U.S. company, recently secured a $14 million contract with the California Department of Transportation to enhance infrastructure project delivery. Between January and June 2026, they repurchased 435,000 shares for $29 million as part of an extensive buyback plan now increased by $100 million. Despite high debt levels and reliance on external funding, ICF's innovative AI-driven solutions and government partnerships position it for potential growth amidst industry challenges.

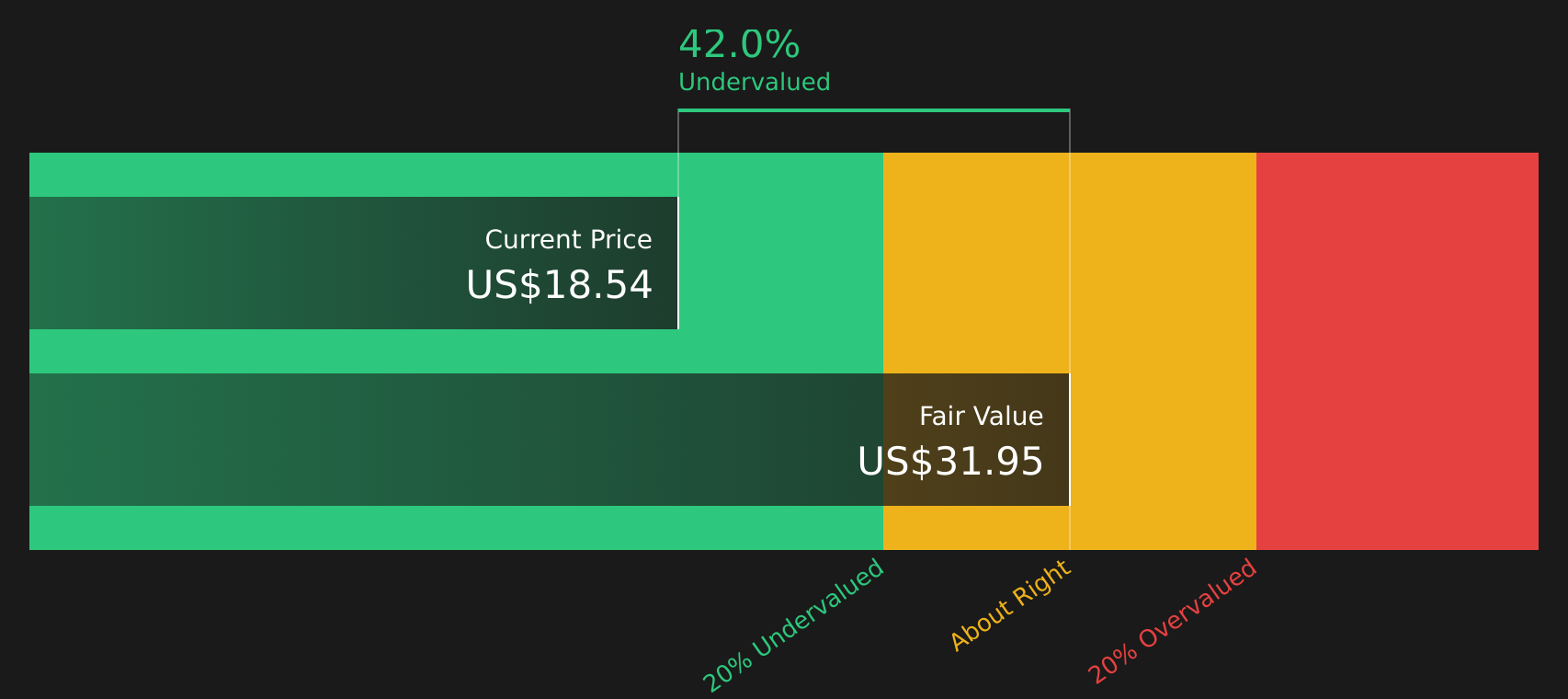

Betterware de MéxicoP.I. de (BWMX)

Simply Wall St Value Rating: ★★★★★★

Overview: Betterware de México is a company that specializes in the direct-to-consumer sale of home organization and solutions products, with a market cap of approximately MX$9.45 billion.

Operations: The company generates revenue primarily through sales, with a notable gross profit margin of 71.69% as of September 2023, reflecting its pricing strategy and cost management. Operating expenses are significant, driven largely by sales and marketing efforts, which reached MX$4.04 billion in December 2023. Net income margins have fluctuated over time, with the most recent figure standing at 8.21% in March 2026.

PE: 10.0x

Betterware de México, a company with significant insider confidence, saw Andres Chevallier purchase 10,000 shares worth US$168,062 in June 2026. This move suggests a positive outlook from within the company. Despite high debt levels and reliance on external borrowing, earnings are projected to grow annually by 26%. Recent earnings show an increase in net income to MXN 281 million for Q1 2026 from MXN 151 million last year. With new CFO Raúl del Villar's extensive experience enhancing financial strategies at multinational firms, Betterware is poised for potential growth amidst its challenges.

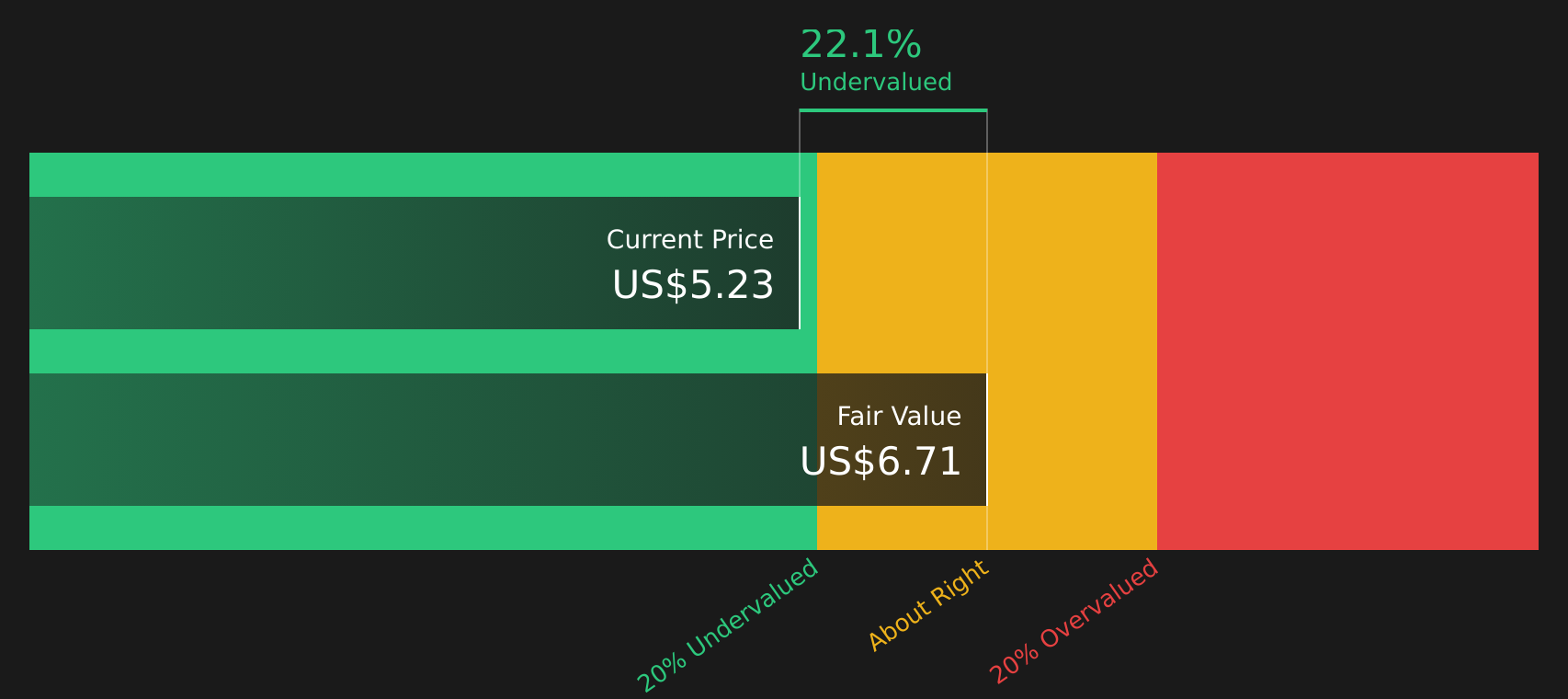

NexPoint Diversified Real Estate Trust (NXDT)

Simply Wall St Value Rating: ★★★★☆☆

Overview: NexPoint Diversified Real Estate Trust operates in the diversified and hospitality real estate sectors, with a market cap of approximately $1.06 billion.

Operations: The company generates revenue primarily from its diversified and hospitality segments. It has experienced fluctuations in net income margin, with a notable shift from negative to positive figures between 2015 and 2021, before returning to negative margins thereafter. The gross profit margin remained at 100% until 2022 when it began to decline, reaching approximately 62.20% by the first quarter of 2026. Operating expenses have consistently included significant general and administrative costs alongside non-operating expenses that have impacted overall profitability.

PE: -2.3x

NexPoint Diversified Real Estate Trust, a smaller company in the real estate sector, recently faced challenges with its removal from the Russell 2000 indices on June 27, 2026. Despite reporting a net loss of US$21.26 million for Q1 2026, down from US$33.16 million the previous year, insider confidence remains evident through share repurchases totaling over one million shares since November 2024. The company's decision to maintain quarterly dividends reflects a commitment to shareholder returns amid financial restructuring efforts and potential growth opportunities in real estate investments.

Summing It All Up

- Click this link to deep-dive into the 65 companies within our Undervalued US Small Caps With Insider Buying screener.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.