ICL Group (ICL) Is Down 5.3% After US Energy Funding Pulled for St. Louis Battery Plant

ICL Group Ltd. ICL | 5.24 | +1.16% |

- ICL Group announced that the U.S. Department of Energy has discontinued federal funding for its planned lithium iron phosphate cathode materials plant in St. Louis, following a comprehensive review and rising project costs.

- This decision could lead to a US$40 million investment write-off if ICL ultimately chooses to discontinue the project, raising new questions about the future of its battery materials expansion in the U.S.

- We’ll examine how the withdrawal of U.S. government support for the St. Louis LFP project could reshape ICL’s diversification strategy.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

ICL Group Investment Narrative Recap

To believe in ICL Group as a shareholder, you need confidence in its ability to successfully diversify beyond traditional fertilizers, particularly by capturing growth in specialty and advanced material markets. The discontinuation of U.S. Department of Energy funding for the St. Louis lithium iron phosphate plant could delay or reduce momentum in its U.S. battery materials expansion, which is currently a major catalyst but also heightens the risk around capital allocation and new growth ventures. The immediate catalyst is now less certain, while project-related investment risks have become more prominent.

Among recent company announcements, the January 2025 joint venture with Shenzhen Dynanonic to produce LFP cathode material in Europe stands out. This move remains relevant as it shows ICL is still advancing its ambitions in battery materials despite U.S. setbacks, and demonstrates that its growth plans extend beyond any single region or project.

But even as ICL pursues new specialties and regional growth, the potential financial write-off tied to scrapped U.S. battery projects is an emerging risk investors should keep in mind...

ICL Group's narrative projects $8.1 billion revenue and $714.9 million earnings by 2028. This requires 5.2% yearly revenue growth and a $310.9 million earnings increase from $404.0 million today.

Uncover how ICL Group's forecasts yield a $6.74 fair value, a 8% upside to its current price.

Exploring Other Perspectives

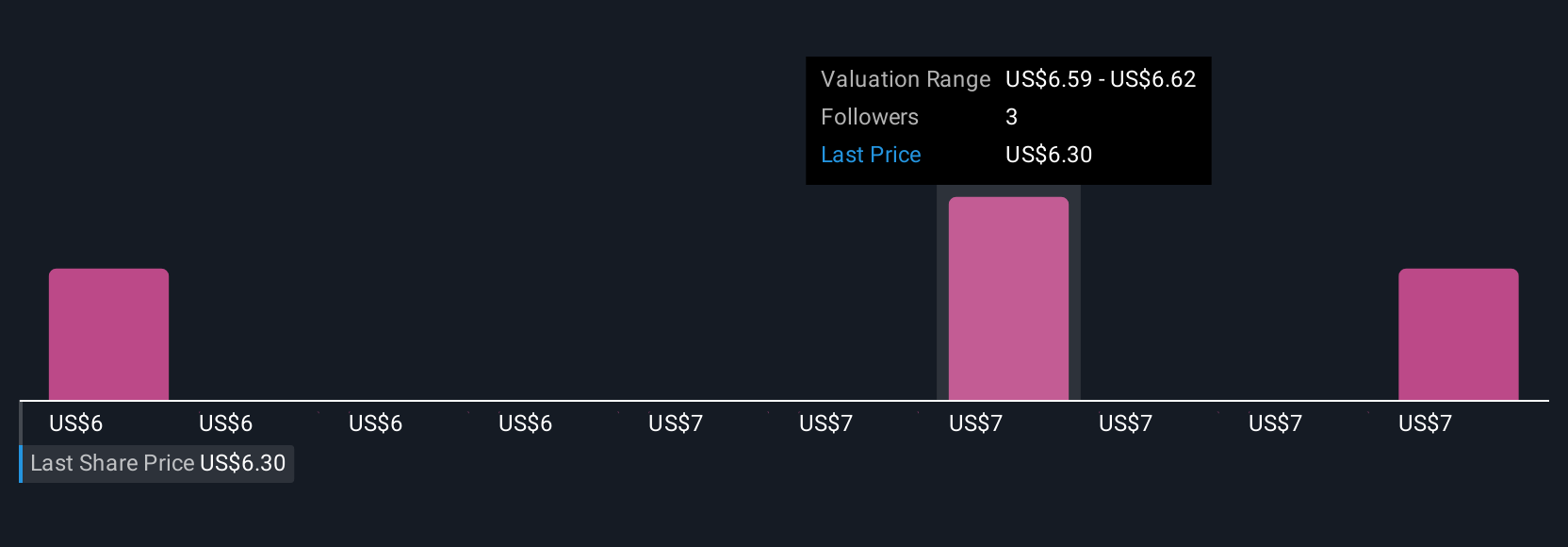

Three Simply Wall St Community members assessed ICL’s fair value between US$5.36 and US$6.74 per share before the latest funding news, showing opinions can vary widely. Ongoing investment in new product lines remains a key source of both potential and risk for future company performance.

Explore 3 other fair value estimates on ICL Group - why the stock might be worth as much as 8% more than the current price!

Build Your Own ICL Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your ICL Group research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

- Our free ICL Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ICL Group's overall financial health at a glance.

Ready For A Different Approach?

Our top stock finds are flying under the radar-for now. Get in early:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 37 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.