IDEXX Laboratories (IDXX): Assessing Valuation After Robust Earnings and Uptake of New Diagnostic Technologies

IDEXX Laboratories, Inc. IDXX | 561.89 | +0.86% |

IDEXX Laboratories (IDXX) just announced quarterly results showing higher reported and organic revenue, supported by momentum from their newest premium diagnostic tools. Even with lighter vet visits, the company delivered impressive business growth this quarter.

IDEXX Laboratories’ share price has rallied strongly in 2025, posting a 56.7% year-to-date gain and a 41.97% total shareholder return over the past twelve months. With enthusiasm growing thanks to robust earnings and rapid uptake of new diagnostics, momentum is clearly building for the stock after a decisive quarterly update.

If breakthroughs in diagnostics have you thinking bigger, consider exploring other healthcare innovators. See the full list for free with our See the full list for free..

The question now is whether IDEXX Laboratories’ strong momentum leaves the stock undervalued, or if the recent surge means investors are already paying up for future growth and innovation.

Most Popular Narrative: 5.7% Undervalued

With IDEXX Laboratories trading at $640.85, the prevailing narrative suggests a fair value almost 6% higher, indicating analyst confidence just above the current price. Investors are watching to see if this bullish outlook can hold in a rapidly evolving diagnostics market, especially considering how much depends on new technology adoption and recurring revenue potential.

Rapid adoption of innovative diagnostic platforms such as inVue Dx, Catalyst Cortisol, and Cancer Dx is expanding IDEXX's addressable market and boosting recurring consumables demand. This is likely to drive sustained revenue and margin growth as new product usage increases and menu breadth widens.

Curious about what truly powers this premium valuation? The narrative is built around ambitious projections for future growth, margin expansion, and a profit multiple that outpaces its industry. Interested in seeing which numbers underpin the price target and how bold these financial forecasts are? Explore the full story to uncover the core financial assumptions driving IDEXX’s valuation.

Result: Fair Value of $679.92 (UNDERVALUED)

However, underlying risks remain. These include the possibility of slowing U.S. veterinary visits and growing competition, both of which could quickly challenge the bullish outlook.

Another View: Price Multiples Raise Caution

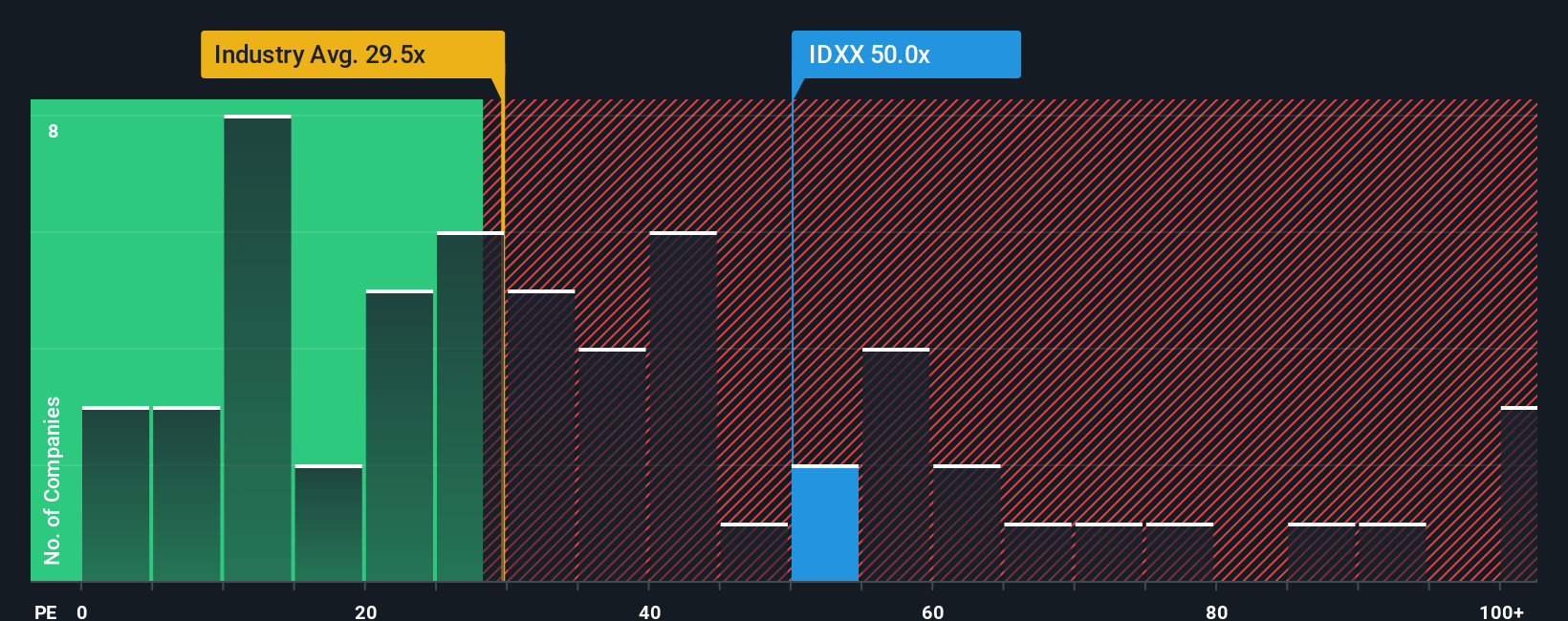

Looking beyond analyst targets, the current valuation tells a different story. IDEXX trades at a price-to-earnings ratio of 52x, significantly higher than both the US Medical Equipment industry average of 29.7x and its peer average of 27x. The market's own fair ratio suggests a much lower benchmark of 31.3x. This gap means investors are paying a substantial premium, raising the question: is growth potential enough to justify these lofty expectations?

Build Your Own IDEXX Laboratories Narrative

If you have a different perspective or want to dive into the numbers yourself, it's quick and easy to craft your own narrative in just a few minutes. Do it your way

A great starting point for your IDEXX Laboratories research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Smart investing means looking beyond obvious winners and spotting new opportunities before everyone else. Use these screens to get ahead of the curve and shape your own advantage:

- Maximize your income potential by tapping into these 17 dividend stocks with yields > 3% with yields above 3%. This is a practical approach for building a resilient portfolio focused on steady returns.

- Capitalize on emerging tech by targeting these 27 AI penny stocks designed to redefine industries with innovations in artificial intelligence and transformative digital solutions.

- Seize opportunities the market might be overlooking and focus on value with these 877 undervalued stocks based on cash flows that offer strong fundamentals at compelling prices.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.