IDT (IDT): Assessing Valuation After Automation Partnership With Hamilton in Genomics

IDT Corporation Class B IDT | 0.00 |

Integrated DNA Technologies (IDT) just announced a partnership with Hamilton to automate next generation sequencing workflows. The collaboration focuses on developing scripts for IDT’s NGS products, aiming to make genomic research more efficient and accessible for labs worldwide.

After a tough month that saw a 28.9% slide in the share price, IDT’s partnership news seems to be rekindling optimism. While short-term share price returns have faced headwinds recently, the company has still delivered a 1.3% total shareholder return over the past year and a remarkable 87% over three years. This underscores strong long-term momentum.

If you’re eager to find more companies with compelling growth stories, broaden your search and discover fast growing stocks with high insider ownership

Given the mix of strong long-term returns and the recent fall in share price, the key question now is whether IDT is genuinely undervalued or if the market is already factoring in all of its growth prospects. Could this be a timely entry point? Or is future upside already reflected in today’s price?

Most Popular Narrative: 41% Undervalued

According to the widely followed narrative, IDT’s fair value estimate stands well above its last close, set to spark debate among investors. This sizable fair value gap is rooted in strong business catalysts and bullish future assumptions.

IDT's NRS segment is launching new features and functionalities, which are expected to deepen market penetration and drive revenue growth in the independent retailer market. This is anticipated to bolster recurring revenue and adjusted EBITDA.

Curious which bold projections for revenue, margins, and recurring cash flows are at the heart of this sky-high valuation? The financial formula powering this narrative relies on ambitious operational improvements. Find out what they are and see if the numbers add up.

Result: Fair Value of $80 (UNDERVALUED)

However, IDT’s exposure to foreign exchange swings and dependence on acquisitions remain potential stumbling blocks that could challenge this positive outlook.

Another View: What Do the Numbers Say?

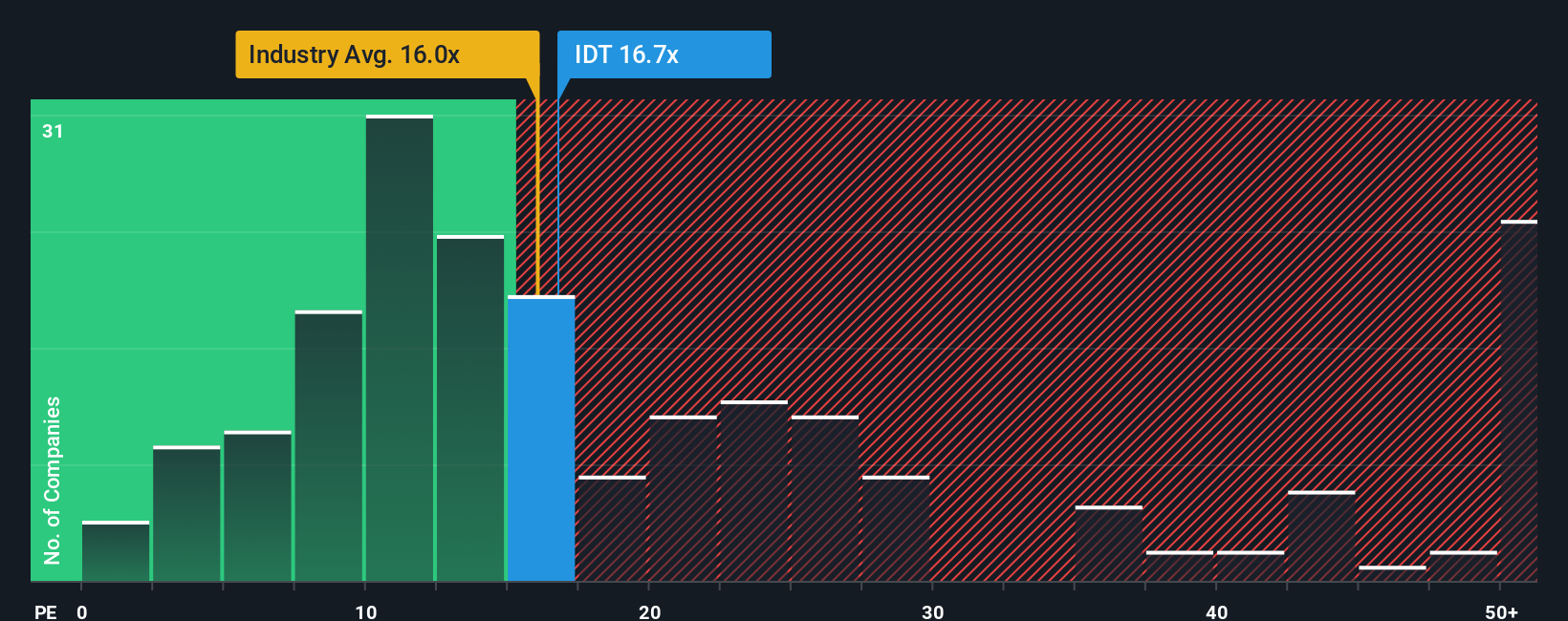

Shifting away from analyst projections, a look at the price-to-earnings ratio gives a different perspective. IDT trades at 15.6x earnings, higher than the fair ratio of 14.8x and the US Telecom industry average of 15.4x, but well below its peers at 19.4x. This means investors might be accepting greater valuation risk relative to industry standards, even as they pay less than the peer average. Is the premium warranted, or could it pose a hurdle if growth does not accelerate?

Build Your Own IDT Narrative

Keep in mind, if this viewpoint does not align with yours or you want to dive into the numbers on your own, you can craft a personalized narrative in just a few minutes. Do it your way

A great starting point for your IDT research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Moves?

Great investing is all about staying ahead. Supercharge your portfolio by uncovering stocks shaping tomorrow, unlocking hidden value, and capturing income you may be missing.

- Tap into tech trends and ride the momentum by checking out these 25 AI penny stocks, which are powering groundbreaking advances in artificial intelligence.

- Hunt for income opportunities with these 18 dividend stocks with yields > 3%, featuring companies providing strong dividend yields above 3% for steady cash flow.

- Jump on undervalued stocks ready to rebound by exploring these 877 undervalued stocks based on cash flows, based on analysis of future cash flows and market catalysts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.