Improved Solar-Backed Securitization Terms Test the Resilience of Sunrun’s Funding Model (RUN)

Sunrun Inc. RUN | 0.00 |

- In late April 2026, Sunrun announced it had priced a US$584 million securitization of residential solar leases and power purchase agreements, its sixteenth such transaction since 2015, featuring US$584 million of A-rated notes with a 6.30% coupon and improved credit spreads versus its 2025 deals.

- This financing, backed by nearly 38,706 systems across 19 states, Washington D.C. and Puerto Rico with a weighted average customer FICO of 744, underscores Sunrun’s continued access to large-scale, asset-backed funding in a capital-intensive residential solar model.

- We’ll now explore how this improved securitization spread and continued access to asset-backed financing may influence Sunrun’s existing investment narrative.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Sunrun Investment Narrative Recap

To own Sunrun, you have to believe residential solar and storage can support a capital intensive, financing heavy model despite policy and credit uncertainties. The new US$584 million securitization, with slightly better spreads, supports the key short term catalyst of continued funding access, while only partially easing the biggest current risk around higher financing costs and reliance on external capital.

The most relevant recent development is Barclays and Citi cutting their Sunrun targets while highlighting greater dependence on asset sales in 2026. That context makes this securitization particularly important, as it shows Sunrun can still tap asset backed markets even as some analysts worry about softer tax equity and earnings pressure ahead.

Yet, behind this improved deal spread, a more serious issue investors should be aware of is Sunrun’s exposure to tighter credit markets and rising funding costs...

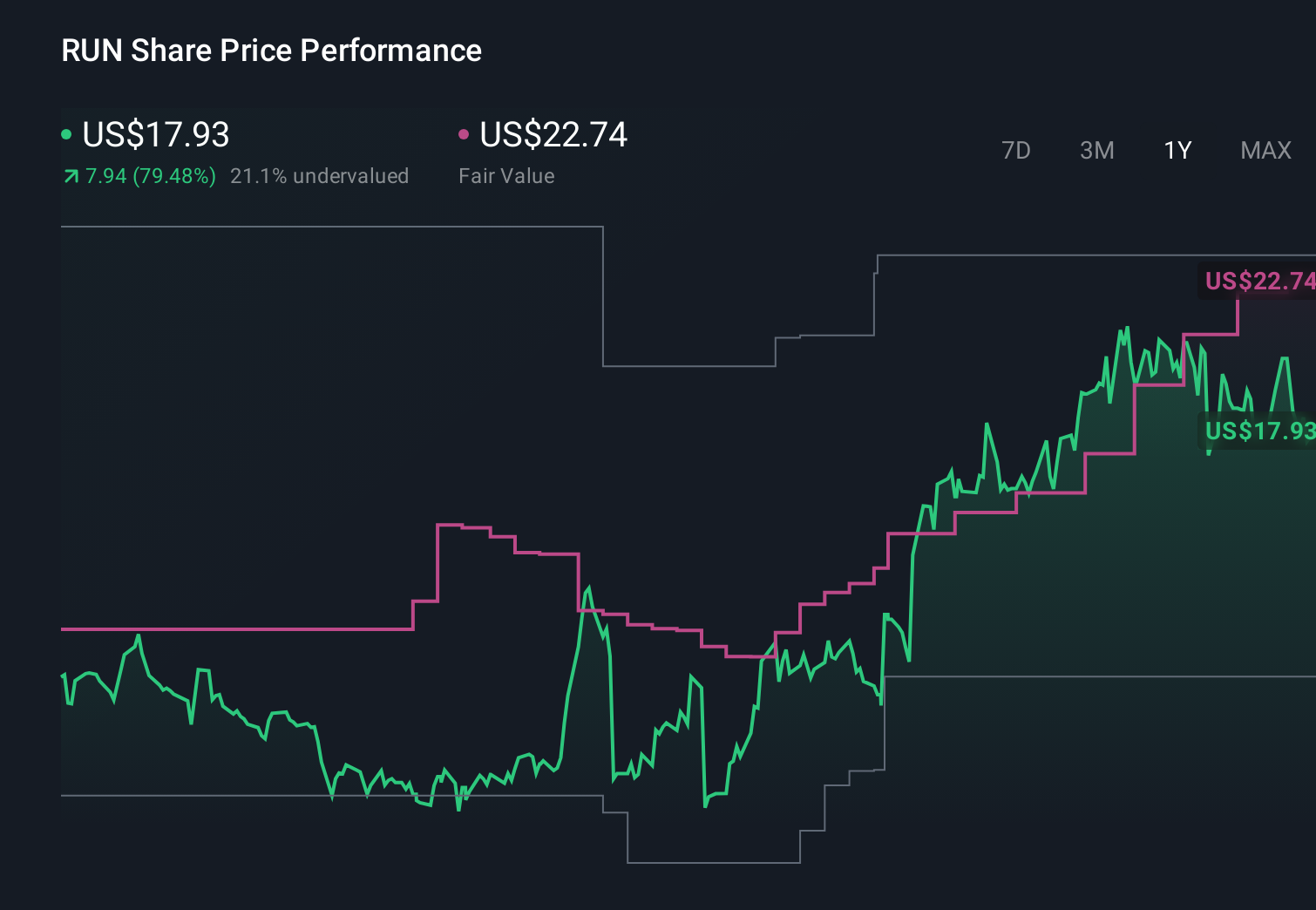

Sunrun's narrative projects $2.9 billion revenue and $465.4 million earnings by 2028. This requires 10.4% yearly revenue growth and about a $3.1 billion earnings increase from -$2.6 billion today.

Uncover how Sunrun's forecasts yield a $22.20 fair value, a 70% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts see a harsher path, with revenue shrinking about 5.6 percent annually and earnings falling from roughly US$447 million to about US$276 million, so if you lean toward that view, this securitization could either soften or reinforce your concerns about how financing risk and grid projects shape Sunrun’s future cash generation.

Explore 3 other fair value estimates on Sunrun - why the stock might be worth over 2x more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Sunrun research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Sunrun research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sunrun's overall financial health at a glance.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 17 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.