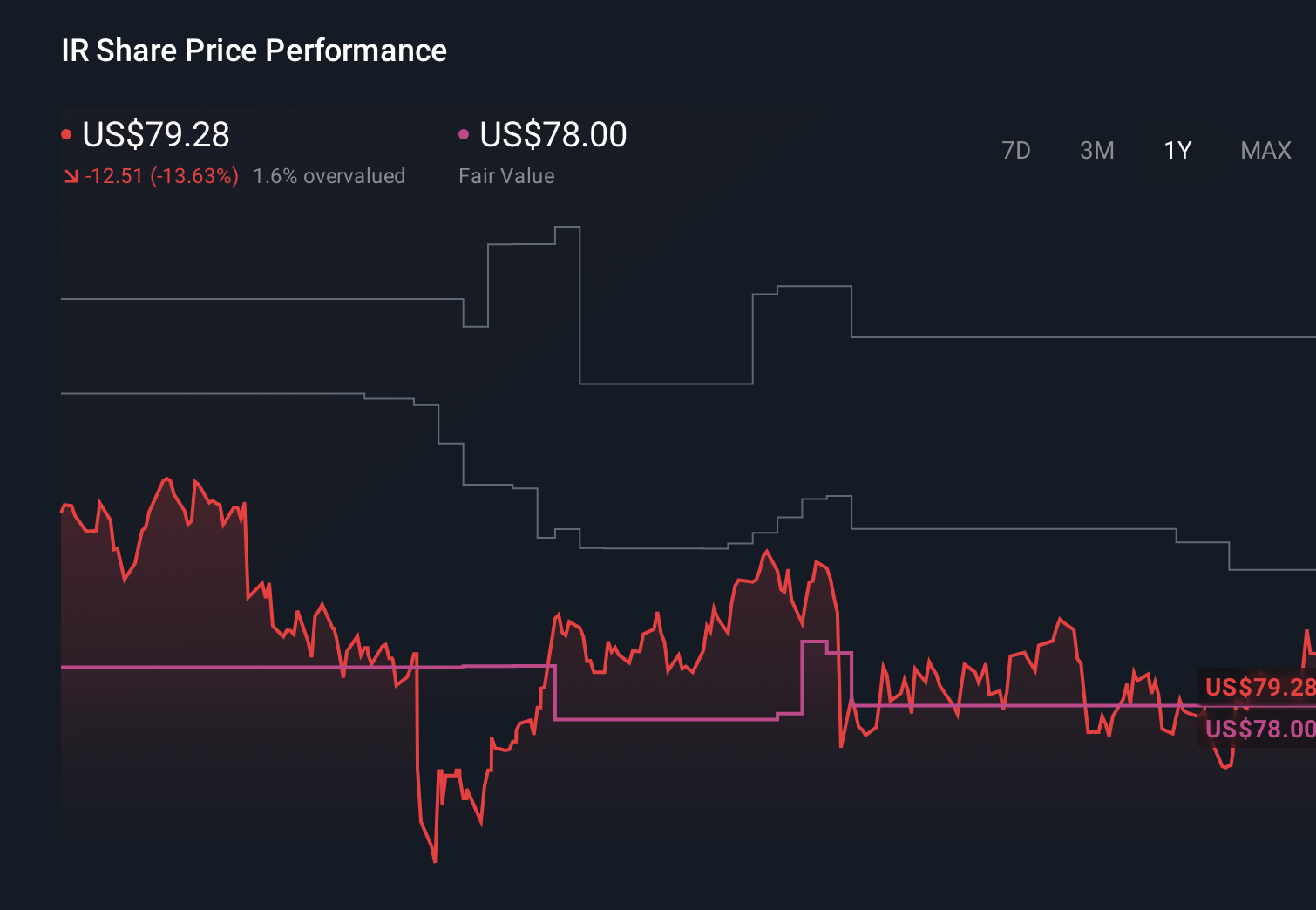

Ingersoll Rand (IR) Is Up 5.3% After Orders Rebound And Book‑To‑Bill Tops One Again – Has The Bull Case Changed?

Ingersoll Rand Inc. IR | 0.00 |

- In recent months, Ingersoll Rand has reported a book-to-bill ratio above one for its first full year since 2022, alongside positive organic order growth in three of the past four quarters and solid cash-generating first-quarter 2026 results.

- Despite insider stock sales of about US$2.7 million and signs of an extended industrial downturn, institutional investors and analysts have highlighted Ingersoll Rand’s resilient, acquisition-driven model and recovering orders as reasons for renewed optimism about its operations.

- We’ll now examine how this recovery in orders and book-to-bill strength may influence Ingersoll Rand’s existing investment narrative and outlook.

Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

Ingersoll Rand Investment Narrative Recap

To own Ingersoll Rand, you need to believe its mix of mission critical equipment, recurring aftermarket revenue, and bolt on acquisitions can compound value through cycles. The key short term catalyst is the apparent order recovery, with book to bill above one, while the biggest risk remains that industrial demand stays soft longer than expected. Recent data on improving orders and solid cash generation appears supportive, but does not remove that cyclical risk.

The most relevant recent update here is the Q1 2026 earnings release, which showed US$1,847.2 million in sales and continued cash generation despite pressure in some segments. Paired with positive organic order trends and a full year book to bill above one, these results give more context for whether the acquisition heavy model and ongoing buybacks are reinforcing the order recovery that many see as the main near term catalyst.

Yet despite improving orders and upbeat commentary, investors should still be aware of the risk that a prolonged industrial downturn could...

Ingersoll Rand's narrative projects $9.0 billion revenue and $1.4 billion earnings by 2029. This requires 4.9% yearly revenue growth and roughly a $0.8 billion earnings increase from $587.0 million today.

Uncover how Ingersoll Rand's forecasts yield a $93.20 fair value, a 20% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue near US$9.4 billion and earnings of about US$1.5 billion by 2029, so if you see order momentum and book to bill strength differently from the risk of expansion into underpenetrated markets backfiring, you might find their much more bullish view very different from the more cautious consensus and worth comparing with your own expectations.

Explore 3 other fair value estimates on Ingersoll Rand - why the stock might be worth as much as 20% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Ingersoll Rand research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Ingersoll Rand research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ingersoll Rand's overall financial health at a glance.

Want Some Alternatives?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.