Ingersoll Rand (IR): Revisiting Valuation After a Recent Short-Term Share Price Rebound

Ingersoll Rand Inc. IR | 80.00 80.00 | 0.00% 0.00% Pre |

Ingersoll Rand (IR) has quietly outperformed the broader industrials space over the past month, with the stock up roughly 8%, even as its year to date performance remains negative.

That recent 30 day share price return of just over 8% looks more like a short term rebound than a full trend change, given the roughly 10% year to date share price decline and still healthy three year total shareholder return of about 61%.

If IR’s move has you thinking about what else could surprise to the upside, now is a good time to explore fast growing stocks with high insider ownership.

With shares still below analysts’ targets despite solid earnings momentum, investors are left wondering if Ingersoll Rand’s recent pullback offers undervalued exposure to long term secular growth or if the market has already priced in the next leg higher.

Most Popular Narrative: 6.8% Undervalued

With Ingersoll Rand last closing at $81.76 against a narrative fair value near $87.70, the story leans toward modest upside driven by fundamentals.

The company continues building recurring, high margin revenue streams through expansion of aftermarket services and value added lifecycle solutions (aftermarket revenue grew to 37% of total), which increases the stability of net margins and supports long term earnings resilience even if new equipment demand remains variable.

Curious how stable service revenues, rising profitability expectations, and a premium future earnings multiple all combine into that fair value estimate? The full narrative explains the specific growth path, margin reset, and valuation bridge behind this upside case, step by step.

Result: Fair Value of $87.70 (UNDERVALUED)

However, that upside hinges on smooth M&A execution and resilient industrial demand; integration missteps or prolonged capex slowdowns are both capable of derailing the premium narrative.

Another View: Rich On Traditional Metrics

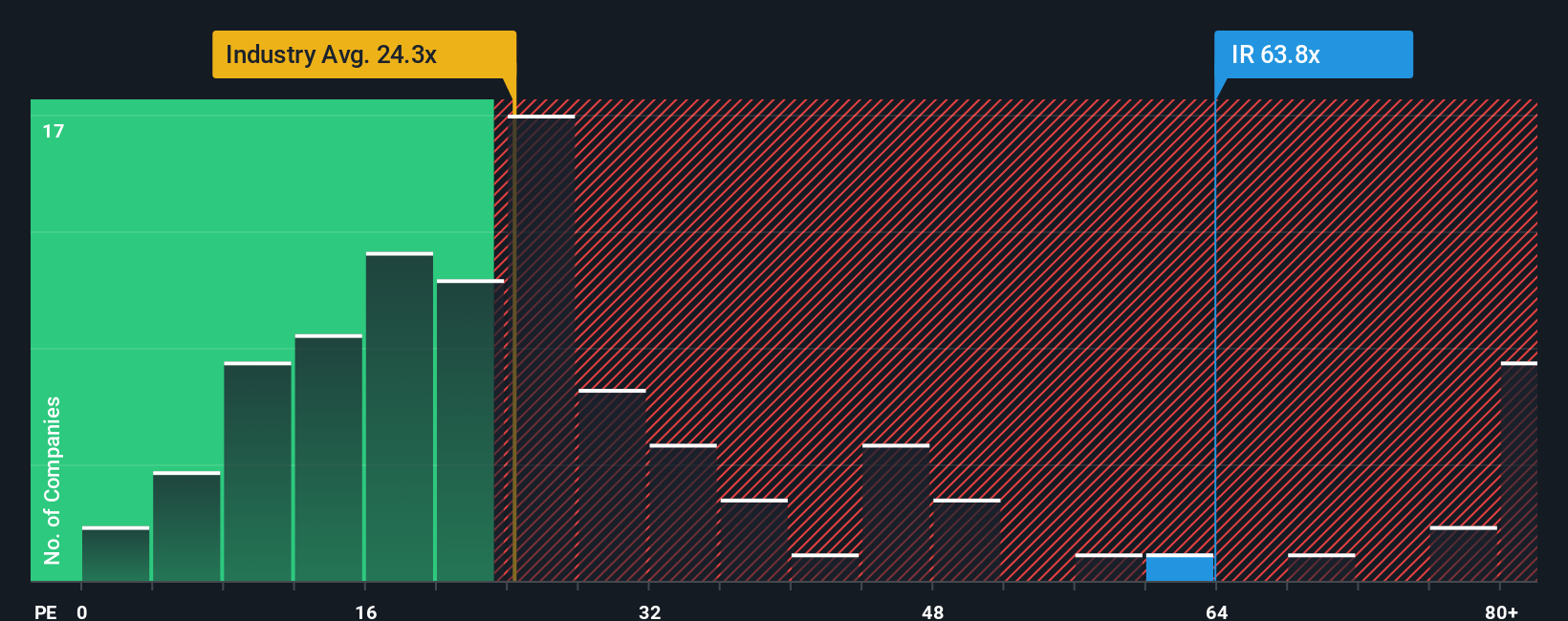

While our fair value work suggests modest upside, the earnings multiple paints a tougher picture. IR trades around 59.3 times earnings, more than double the US Machinery industry at 26 times and well above peers at 26.1 times, compared with a fair ratio of 39.9 times. That rich gap could compress quickly if growth stumbles, so is today’s discount really enough compensation for multiple risk?

Build Your Own Ingersoll Rand Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a tailored view in just a few minutes: Do it your way.

A great starting point for your Ingersoll Rand research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Do not stop at a single stock when the market is full of opportunities; use the Simply Wall Street Screener now so you are not second guessing later.

- Capture potential multi-baggers early by scanning these 3611 penny stocks with strong financials that already back their small size with solid financial foundations.

- Position yourself for the next wave of innovation by reviewing these 26 AI penny stocks powering advances in automation, data, and intelligent software.

- Explore income potential by targeting these 13 dividend stocks with yields > 3% offering yields above 3% while also considering underlying business quality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.