Ingersoll Rand (IR) Stock Revalued As Recurring Revenue Model Reduces Cyclical Risk

Ingersoll Rand Inc. IR | 0.00 |

Ingersoll Rand (IR) is drawing fresh attention after investors reacted to its shift from traditional machinery cycles toward service driven, recurring revenue, a change that is reshaping how the stock’s risk profile is viewed.

At a recent share price of US$74.00, Ingersoll Rand has seen short term momentum pick up, with a 1 month share price return of 3.66%. However, the 1 year total shareholder return is down 7.98% after a softer period that included a decline of 9.90% over the last 90 days.

If this shift toward more recurring revenue has you rethinking industrials, it could be a good moment to widen your search using the 35 power grid technology and infrastructure stocks

With the stock down over the past year yet trading at a discount to analyst price targets and some estimates of intrinsic value, you have to ask: Is this a reset that opens a buying window, or is the market already banking on future growth?

Most Popular Narrative: 20.6% Undervalued

Ingersoll Rand's most followed narrative points to a fair value of $93.20 against the last close at $74.00, putting the current share price well below that estimate while analysts anchor their work on detailed revenue and margin assumptions.

The company continues building recurring, high-margin revenue streams through expansion of aftermarket services and value-added lifecycle solutions (aftermarket revenue grew to 37% of total), which increases the stability of net margins and supports long-term earnings resilience even if new equipment demand remains variable.

Curious what sits behind that fair value gap? The narrative focuses on earnings growth, expanding margins, and a richer mix of recurring revenue over time.

Result: Fair Value of $93.20 (UNDERVALUED)

However, this depends on acquisitions delivering clean integration and returns, as well as on industrial spending not slowing enough to pressure volumes, margins, and the implied future P/E.

Another View: What The P/E Is Telling You

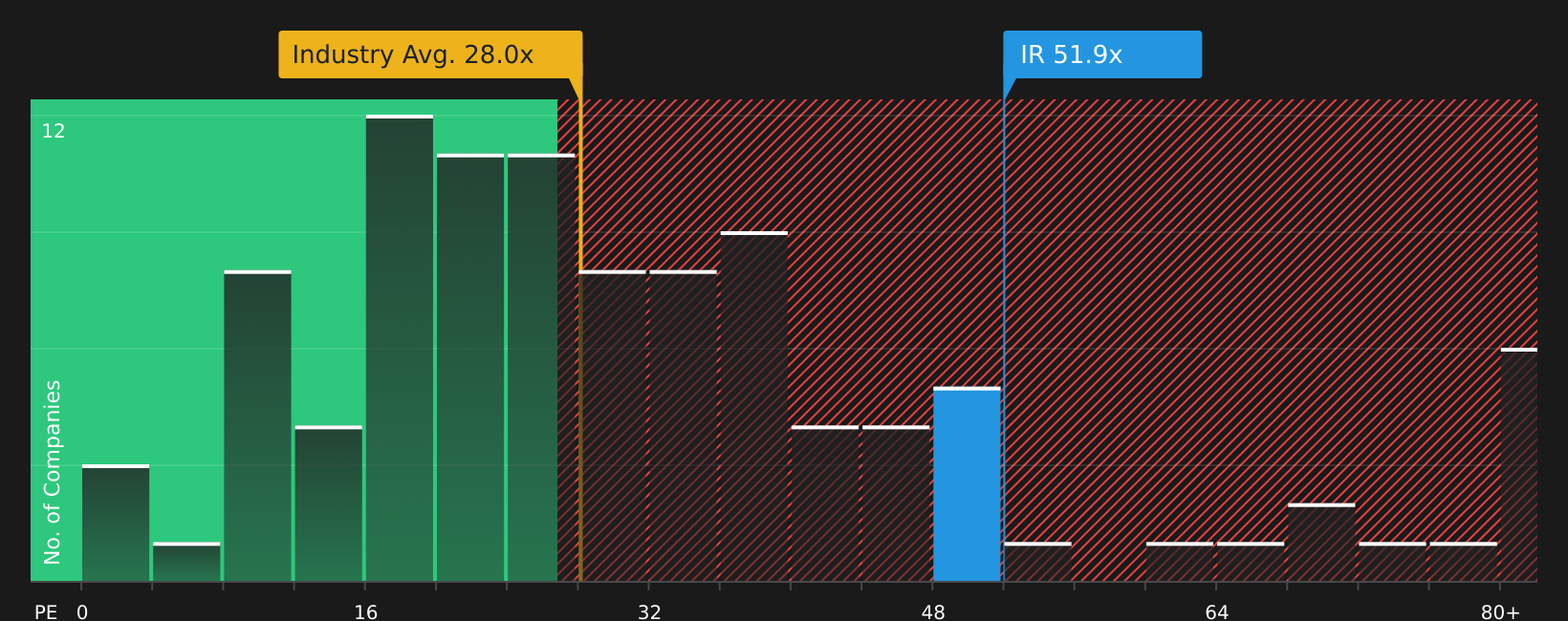

That 20.6% gap to fair value sits awkwardly next to the current P/E of 49.3x, which is far higher than both the Machinery industry at 26.9x and a fair ratio of 36.2x. If sentiment cools, the share price could move toward those lower multiples instead.

Next Steps

Seeing mixed signals on valuation and sentiment? Do not wait for a consensus. Review both the risks and the upside, starting with the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If you only stop at one stock, you risk missing opportunities that fit your style better, so broaden your watchlist using focused screeners built from real fundamentals.

- Target potential mispricings by scanning companies that combine quality fundamentals with appealing valuations through the 44 high quality undervalued stocks.

- Prioritise resilience by reviewing companies highlighted in the 70 resilient stocks with low risk scores that score well on balance sheet strength and risk factors.

- Get ahead of the crowd by checking the screener containing 20 high quality undiscovered gems for companies with solid fundamentals that fewer investors are watching closely.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.