Inside Google’s 13F: Alphabet Reveals Q4 Holdings—Why ASTS and Planet Labs Top the List

Alphabet Inc. Class C GOOG | 294.46 | -0.15% |

AST SPACEMOBILE INC ASTS | 92.62 | +10.28% |

Planet Labs PBC PL | 35.88 | +16.83% |

Revolution Medicines RVMD | 99.12 | +0.49% |

Tempus AI, Inc. Class A TEM | 47.39 | +0.77% |

As Wall Street digests the latest round of fourth-quarter 13F filings from hedge funds, the latest moves by asset management giants are coming into focus.

According to the 13F filing submitted to the SEC by Alphabet Inc. Class C(GOOG.US), the parent company of Google, the tech giant's top two equity holdings remain the pioneer of space-based cellular broadband AST SPACEMOBILE INC(ASTS.US) and satellite imagery firm Planet Labs PBC(PL.US).

Notably, Google did not open any new positions or increase its stake in any existing companies during the quarter. As a result, this report focuses on a breakdown of Google's top ten heavyweights.

1. The Space Economy: An 'Interstellar Leap' in Communication and Data

Together, AST SPACEMOBILE INC(ASTS.US) and Planet Labs PBC(PL.US) account for 49.6% of the top ten holdings—dominating nearly half of the portfolio's weight.

First, looking at AST SPACEMOBILE INC(ASTS.US), this company is building the world’s first space-based cellular broadband network accessible directly by standard smartphones. By launching high-performance satellites, it aims to provide seamless connectivity to areas globally that currently suffer from network dead zones.

Imagine standing in a desert, deep in the mountains, or out at sea with no cell towers in sight. Yet, your phone still has a signal, allowing you to make calls, send texts, and even surf the web. This is the "Direct-to-Device" reality ASTS is building.

Unlike traditional networks that rely on thousands of interconnected ground towers to form a dense cellular grid, a space-based network relies on satellites moving at high speeds in orbit. These satellites act as "flying cell towers," transmitting signals directly back to the core network on the ground. It is a centralized coverage method acting like a massive canopy, easily spanning physical obstacles to achieve comprehensive coverage.

ASTS’s solution differs significantly from SpaceX’s Starlink. While Starlink requires a dedicated dish to receive signals, ASTS’s goal is for your existing phone to be the satellite receiver, offering superior convenience.

To achieve this, ASTS has launched satellites equipped with the largest commercial communications arrays in history—nearly 700 square feet in size. These act like giant "space ears" with extreme sensitivity, designed to capture weak signals from standard ground-based phones. The test satellite, BlueWalker 3, has already successfully demonstrated 4G, 5G, and data transmission capabilities from space to unmodified phones, proving the technology is viable and not just theoretical.

Looking ahead, the pace of satellite deployment will be the most critical catalyst for stock volatility. Currently, the company has successfully deployed its first five commercial satellites (BlueBird) to Low Earth Orbit. It plans to complete 40 satellites by early 2026, reaching 45-60 by year-end, with production capacity ramping to six per month.

In summary, while ASTS is in the early stages of commercialization, its unique technological approach, solid strategic partnerships, and clear deployment roadmap allow it to compete with a differentiated product in the space sector.

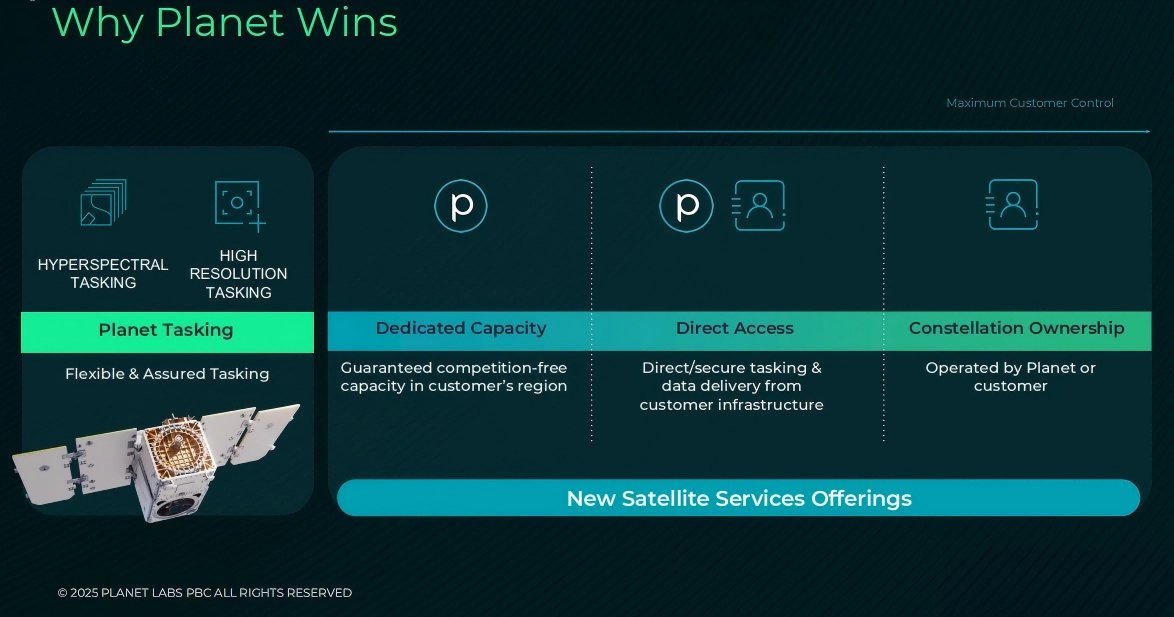

Secondly, Planet Labs PBC(PL.US) is a global leader in Earth observation and satellite data. Operating the world's largest fleet of satellites in orbit, it possesses the unique capability to scan the entire Earth's landmass daily.

The company is dedicated to building a "dynamic geophysical index." By capturing high-frequency, continuous satellite imagery, it provides critical data support for agricultural monitoring, defense intelligence, energy infrastructure management, and climate sustainability. Currently, the company is actively using AI to mine its massive archive of historical data, accelerating its transition from a simple "satellite image vendor" to a high-value "geospatial data and insights provider."

Planet Labs' commercial roadmap is iterating from a "resource" model to a "service" model, supported by three business lines:

- Layer 1: The Photographer of Earth (Data Subscription): This is Planet’s most well-known business. Leveraging its massive satellite constellation, it provides high-frequency imagery to global clients much like a newspaper subscription. Whether it’s the Pentagon or a farmer, they aren't just buying a photo; they are buying the right to monitor daily changes on Earth. This gives Planet robust, SaaS-like cash flow.

- Layer 2: The Data Actuary (Analytics Services): Raw imagery is just the raw material; Planet is attempting to use AI to process it into a finished product. Through computer vision, it can automatically count ships in a port or assess forest fire damage. This means clients don't need to hire staff to look at pictures—they buy the "analytical results." Expansion in this layer implies Planet is gaining core pricing power.

- Layer 3: The Space Contractor (Satellite Services): This is a strategic business addressing the rise of "sovereign space capabilities." By providing full "build + launch + operate" delivery services to nations or agencies, Planet can rapidly boost its backlog and Remaining Performance Obligations (RPO). The financial logic here is astute: it allows the company to use client capital to build constellation capacity, optimizing CapEx efficiency despite gross margins fluctuating based on hardware and partnership models.

Investors should note three main themes from recent earnings calls that may impact share performance:

- The Base (Government): Planet Labs is showing a clear trend toward "government-heavy" revenue. The explosion in Defense & Intelligence (D&I) business validates the product's irreplaceability, providing a safety net for revenue. However, the reduction in EOCL (Electro-Optical Commercial Layer) and NASA orders warns of "concentration risk." Fluctuations in U.S. fiscal budget cycles and appropriations can translate directly into quarterly earnings "noise." The market is currently debating whether to award a "certainty premium" for high order visibility or a "dependency discount" for reliance on government budgets.

- The Growth Driver (AI): Selling images is a "red ocean"; selling answers is the "blue ocean." The shift from data to decision-making driven by AI determines Planet's long-term market cap ceiling. Management has repeatedly emphasized Maritime Domain Awareness and change detection, essentially attempting to upgrade the business model from a low-margin data supplier to a high-barrier intelligence system provider. Commercial demand from insurance, finance, and supply chains will only hit an inflection point when Planet delivers "actionable answers," not just pictures.

- New Tech (GPUs in Space): "Project Owl" (edge computing with Nvidia GPUs) and "Suncatcher" (space TPUs in partnership with Google) form an imaginative technical narrative. They represent the future of "Space Computing" and grab headlines. However, investors need to remain grounded: at this stage, these are largely "R&D-style call options." In the short term, the income statement relies on government contract fulfillment and legacy satellite services.

2. Biotech: An AI-Driven Life Sciences Transformation

Google’s top ten holdings include a strategic cluster of four biotech companies— Revolution Medicines(RVMD.US), Tempus AI, Inc. Class A(TEM.US), DexCom, Inc.(DXCM.US), and Maze Therapeutics, Inc.(MAZE.US)—signaling Google's attempt to stake out positions across the biotech matrix.

- Revolution Medicines(RVMD.US) focuses on developing RAS(ON) inhibitors. RAS mutations are present in 30% of cancers and have historically been extremely difficult to target. Although Google slightly trimmed its position in Q4, maintaining it as the third-largest holding reflects significant confidence in its potential to develop a "universal cancer drug."

- Tempus AI, Inc. Class A(TEM.US) is an AI-driven precision medicine platform possessing the world's largest library of clinical and molecular data. It uses AI to assist physicians in diagnosis and treatment selection, representing the most direct play for Google’s AI implementation in healthcare.

- DexCom, Inc.(DXCM.US) remains the dominant player in Continuous Glucose Monitoring (CGM) systems and a leader in wearable health monitoring. With the rollout of its new Stelo product in 2026, DexCom is pivoting from solely diabetes monitoring to the broader health management market.

- Maze Therapeutics, Inc.(MAZE.US), which saw a small reduction in Google’s stake, focuses on kidney and cardiovascular metabolic diseases. Its Compass platform precisely identifies genetic variants, fitting the "platform biotech" logic that aligns with Google’s preference for data-driven R&D.

3. IT and Software: The Execution Entry Point for Agentic AI

- Freshworks, Inc. Class A(FRSH.US): The highlight here is AI-enabled enterprise client and employee experience management. With strong growth projected for its Employee Experience (EX) platform in 2026, FRSH lowers operating costs through AI, becoming a staple for digital transformation in SMBs.

- UiPath, Inc. Class A(PATH.US): Known for Robotic Process Automation (RPA), the company is pivoting toward "Agentic AI." It serves as a critical technical execution platform for Google to land AI on the enterprise side, replacing cumbersome manual workflows.

- GITLAB INC.(GTLB.US): A one-stop AI-native DevSecOps platform handling everything from coding to deployment. In the era of AI-generated code, GitLab represents a choke point for controlling the developer ecosystem.

4. Semiconductors: The Infrastructure of the Computing World

ARM Holdings PLC Sponsored ADR(ARM.US) constructs the foundational rules of the global digital world. It not only holds a near-monopoly (99%) in the smartphone market but, thanks to the extreme energy efficiency of its architecture, has become the "computational oxygen" for AI data centers and edge computing.

For Google, holding Arm has a dual strategic significance:

- Ecosystem Defense: Ensuring the stability of the underlying architecture for the global Android ecosystem.

- Cloud Offense: Google Cloud’s proprietary Axion processors are built on the Arm architecture.

With the accelerated penetration of the v9 architecture and the explosion in demand for low-power computing in data centers, Arm is evolving from a simple IP licensor to a key "tax collector" of the AI era, enjoying a high certainty premium in the computing arms race.

Summary

This list reveals Google's core ambitions: "Connecting the world from space, conquering cancer with AI, and reshaping productivity through automation." For investors, these companies often represent the "technological monopolists" of their respective vertical tracks.