Insider Activity Highlights These 3 Undervalued Small Caps Across Regions

Arbor Realty Trust Inc ABR | 0.00 |

The United States market has remained flat over the last week but is up 16% over the past year, with earnings anticipated to grow by 15% annually. In this environment, identifying stocks that are potentially undervalued can be crucial for investors seeking opportunities, particularly when insider activity suggests confidence in a company's future prospects.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Enovis | NA | 0.6x | 47.58% | ★★★★★★ |

| PCB Bancorp | 8.6x | 2.8x | 27.57% | ★★★★★☆ |

| AVITA Medical | NA | 1.6x | 37.83% | ★★★★★☆ |

| Franklin Financial Services | 10.8x | 2.7x | 1.92% | ★★★★☆☆ |

| 1st Source | 10.7x | 4.0x | 49.10% | ★★★★☆☆ |

| German American Bancorp | 13.9x | 4.6x | 46.70% | ★★★☆☆☆ |

| New Peoples Bankshares | 9.4x | 2.2x | 41.69% | ★★★☆☆☆ |

| Bank of the James Financial Group | 10.4x | 1.9x | 48.19% | ★★★☆☆☆ |

| Union Bankshares | 10.1x | 2.1x | 22.20% | ★★★☆☆☆ |

| Aldeyra Therapeutics | NA | NA | 46.79% | ★★★☆☆☆ |

We're going to check out a few of the best picks from our screener tool.

Trinity Capital (TRIN)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Trinity Capital is a financial services company specializing in providing venture capital, with a market cap of $0.69 billion.

Operations: The company primarily generates revenue from its venture capital segment, with a reported $279.52 million in the most recent period. Operating expenses have shown an upward trend, reaching $69.35 million by the latest quarter. Despite fluctuations in net income, gross profit margins have consistently remained at 100%.

PE: 9.0x

Trinity Capital, a player in the lower middle market, recently formed a joint venture with Capital Southwest Corporation to invest in senior secured debt opportunities, each committing US$50 million. Despite an earnings dip in Q4 2025 compared to the previous year, revenue for the full year rose to US$293.65 million from US$237.69 million. Insider confidence is evident with Steven Brown purchasing 27,109 shares valued at approximately US$399,858 between October and November 2025. With no recent share buybacks and reliance on external borrowing for funding, Trinity's strategic moves could drive future growth despite current financial challenges.

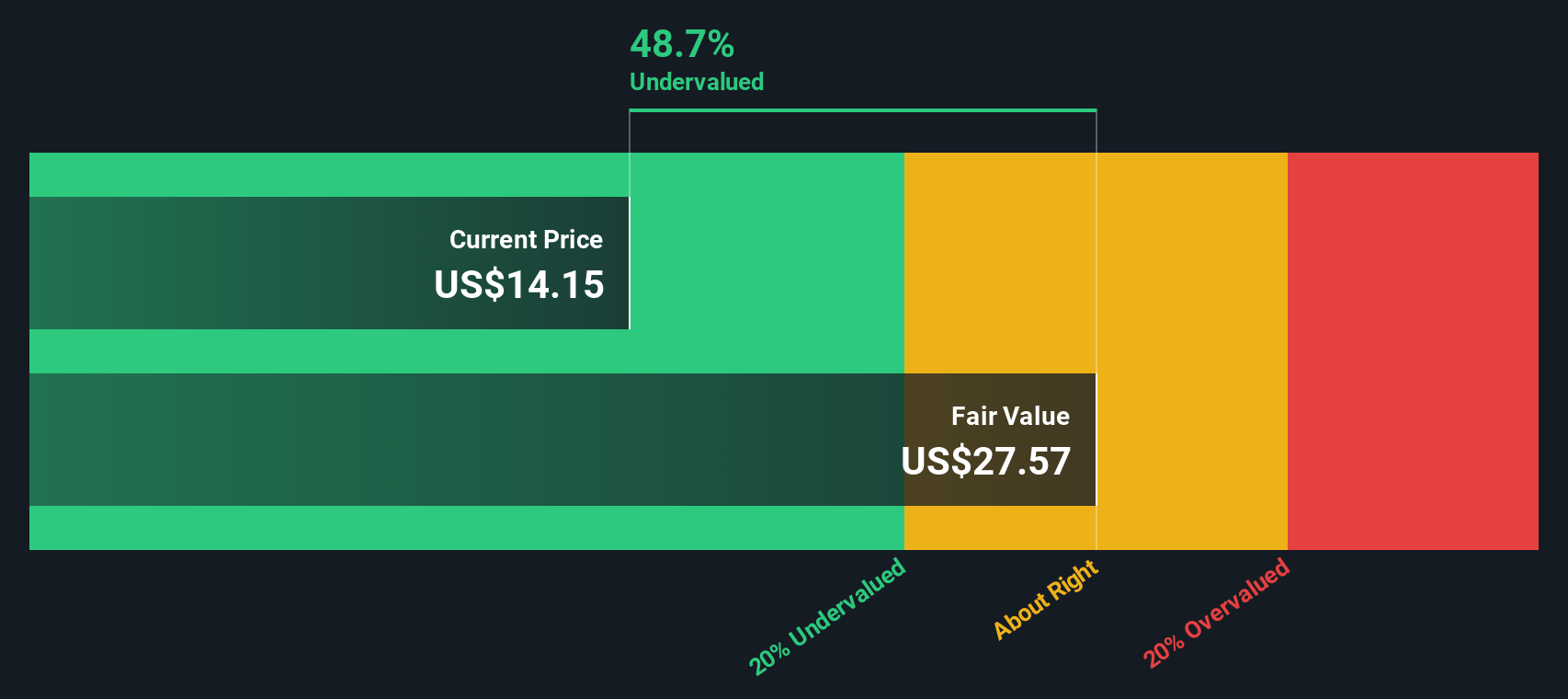

Arbor Realty Trust (ABR)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Arbor Realty Trust is a real estate investment trust that specializes in providing loans and financing for multifamily and commercial real estate, with a market capitalization of approximately $2.73 billion.

Operations: Arbor Realty Trust generates revenue primarily from its Agency and Structured Business segments. The company has seen fluctuations in its gross profit margin, with a notable high of 93.44% in the first quarter of 2021. Operating expenses are significant, with General & Administrative Expenses being a major component.

PE: 13.9x

Arbor Realty Trust, a smaller company in the U.S., has shown insider confidence with recent share purchases. The company closed a $762.6 million securitization deal, enhancing its financial flexibility for future investments. Despite a decline in net income to US$148.8 million for 2025 compared to the previous year, Arbor's strategic moves like debt financing and executive appointments signal potential growth opportunities. Additionally, their ongoing share repurchase program underscores commitment to shareholder value amidst challenging profit margins and higher-risk funding sources.

Babcock & Wilcox Enterprises (BW)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Babcock & Wilcox Enterprises is a company that provides energy and environmental technologies and services, with a market cap of approximately $0.5 billion.

Operations: BW's revenue model primarily involves generating income through its core business operations, with a recent reported revenue of $587.68 million. The company's cost structure includes significant expenditures on COGS and operating expenses, impacting its profitability metrics. Notably, the gross profit margin has shown variability over time but was 24.48% in the most recent period analyzed.

PE: -41.6x

Babcock & Wilcox Enterprises, a smaller company in the U.S., recently reported a turnaround with Q4 net income of US$9.2 million, bouncing back from a US$63.2 million loss the previous year. This shift suggests potential value for investors eyeing smaller companies. Despite high volatility and reliance on external borrowing, insider confidence is evident with recent share purchases, signaling trust in future growth prospects. The company's strategic moves include an agreement with Siemens Energy for power projects and extending credit facilities to 2028, indicating plans for expansion and stability amidst industry challenges.

Summing It All Up

- Unlock more gems! Our Undervalued US Small Caps With Insider Buying screener has unearthed 53 more companies for you to explore.Click here to unveil our expertly curated list of 56 Undervalued US Small Caps With Insider Buying.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.