Insiders Are Betting Big On These 3 High Growth Stocks

Evolus EOLS | 0.00 |

Over the last 7 days, the United States market has risen by 2.2%, and over the past 12 months, it is up by an impressive 25%, with earnings expected to grow by 19% per annum in the coming years. In this thriving environment, growth companies with high insider ownership can be particularly appealing as they often indicate strong confidence from those closest to the business's operations and future prospects.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Uxin (UXIN) | 34.3% | 74.1% |

| Upstart Holdings (UPST) | 14.1% | 58.5% |

| SharonAI Holdings (SHAZ) | 34.9% | 92.8% |

| QT Imaging Holdings (QTI) | 23.9% | 104.2% |

| Karman Holdings (KRMN) | 15.6% | 52.6% |

| Figure Technology Solutions (FIGR) | 26.8% | 54.1% |

| Corcept Therapeutics (CORT) | 10.9% | 48.9% |

| Astera Labs (ALAB) | 10% | 29.3% |

| AppLovin (APP) | 27.2% | 21.7% |

| Abeona Therapeutics (ABEO) | 16.5% | 32.9% |

We're going to check out a few of the best picks from our screener tool.

Evolus (EOLS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Evolus, Inc. is a performance beauty company that provides products in the cash-pay aesthetic market across the United States, Canada, Europe, and Australia with a market cap of approximately $443.20 million.

Operations: Revenue Segments (in millions of $): Evolus generates $301.79 million from delivering medical aesthetic products within the cash-pay aesthetic market.

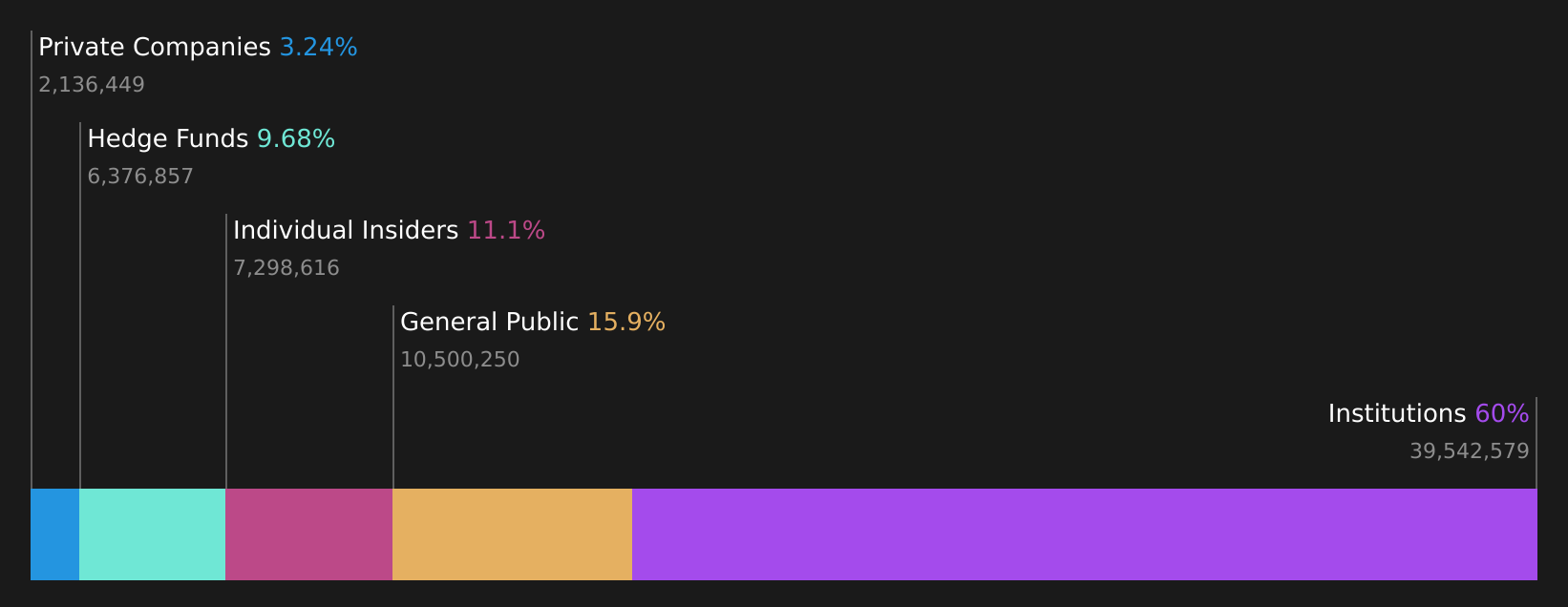

Insider Ownership: 11.1%

Earnings Growth Forecast: 66.7% p.a.

Evolus is trading at a significant discount to its estimated fair value and offers promising growth prospects, with earnings expected to increase by 66.74% annually over the next three years. Despite negative shareholder equity, Evolus's revenue is forecasted to grow at 14.4% per year, outpacing the U.S. market average of 12.7%. Recent developments include a $250 million shelf registration filing and the European launch of its Estyme HA gel collection, marking international expansion in dermal fillers.

Hennessy Capital Investment VII (HVII)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Hennessy Capital Investment Corp. VII is a company without significant operations, with a market capitalization of $271.16 million.

Operations: Revenue Segments (in millions of $): null

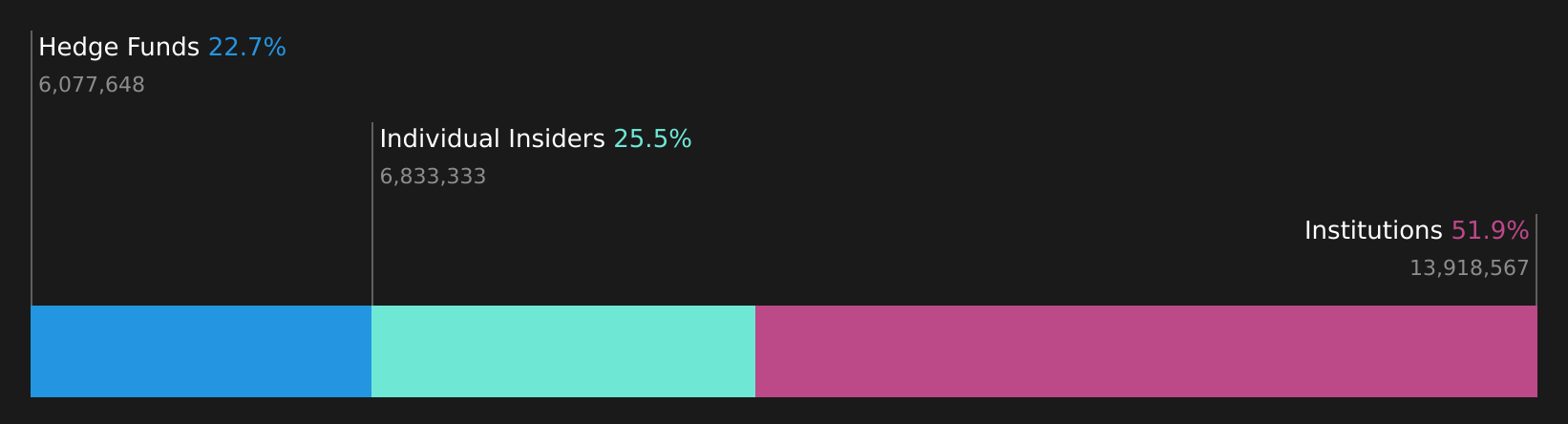

Insider Ownership: 25.5%

Earnings Growth Forecast: 74.8% p.a.

Hennessy Capital Investment VII demonstrates strong growth potential, with revenue expected to increase by 68.2% annually, significantly outpacing the U.S. market's 12.7% growth rate. Despite negative shareholder equity and earnings declining from US$1.02 million to US$0.58 million in the latest quarter, its earnings are projected to grow substantially at 74.8% per year over the next three years, surpassing the U.S. market's average of 18.5%.

Upstart Holdings (UPST)

Simply Wall St Growth Rating: ★★★★★★

Overview: Upstart Holdings, Inc. operates a cloud-based AI lending platform in the United States and has a market capitalization of approximately $2.92 billion.

Operations: The company's revenue is primarily generated from its personal lending segment, which accounts for $1.01 billion.

Insider Ownership: 14.1%

Earnings Growth Forecast: 58.5% p.a.

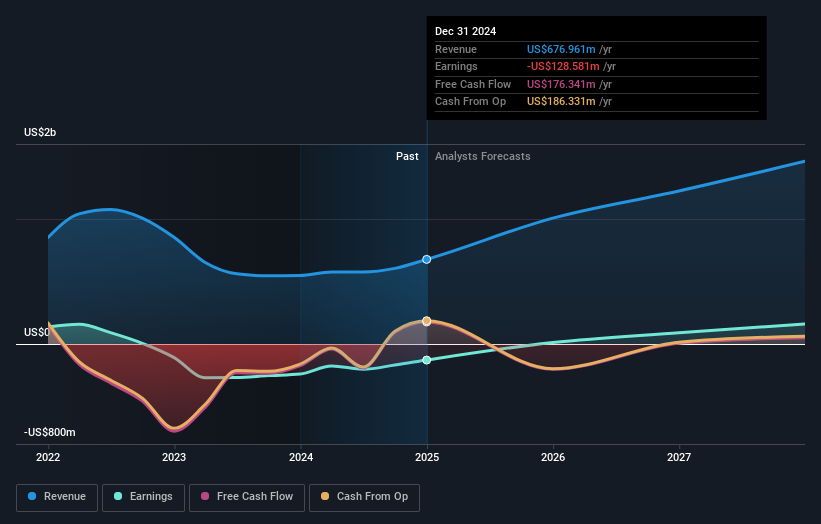

Upstart Holdings is positioned for robust growth, with revenue expected to increase by 21.5% annually, surpassing the U.S. market's rate of 12.7%. Earnings are anticipated to grow significantly at 58.5% per year over the next three years, outpacing the broader market's average growth rate of 18.5%. Recent insider activity shows more substantial buying than selling over the past three months, while partnerships with multiple credit unions expand its lending reach despite current profitability challenges and legal issues.

Turning Ideas Into Actions

- Get an in-depth perspective on all 173 Fast Growing US Companies With High Insider Ownership by using our screener here.

- Interested In Other Possibilities? We've found 8 US stocks that are forecast to pay a dividend yeild of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.