Insmed (INSM) Is Down 16.8% After Reaffirming 2026 BRINSUPRI and ARIKAYCE Revenue Guidance

Insmed Incorporated INSM | 0.00 |

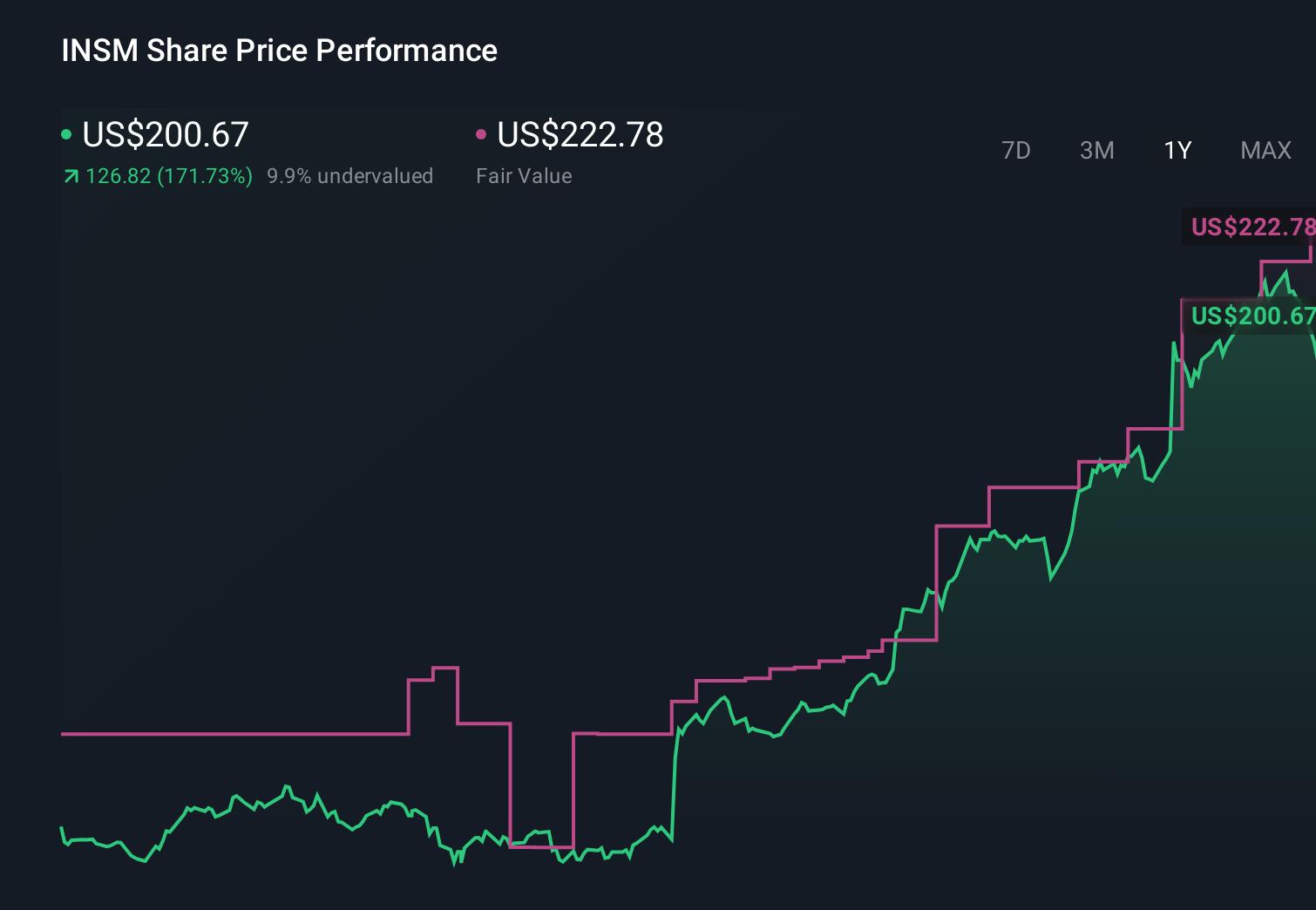

- Insmed Incorporated recently reported first-quarter 2026 results showing a narrower net loss of US$163.56 million and reiterated 2026 revenue guidance for BRINSUPRI of at least US$1 billion and ARIKAYCE of US$450 million to US$470 million.

- The company is also set to showcase six presentations from its respiratory portfolio at ATS 2026, highlighting both new clinical data and its role in addressing underdiagnosis of bronchiectasis through an independently run quality improvement initiative.

- We’ll now examine how Insmed’s reaffirmed 2026 revenue guidance for BRINSUPRI and ARIKAYCE influences the company’s existing investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Insmed Investment Narrative Recap

To own Insmed today, you need to believe that BRINSUPRI and ARIKAYCE can underpin a respiratory-focused rare disease franchise while the company narrows losses and manages safety and reimbursement risks. The reaffirmed 2026 revenue guidance for both drugs, alongside a smaller quarterly net loss, supports the existing thesis but does not materially change the key near term catalyst of BRINSUPRI execution or the ongoing risk that payer pushback or safety issues could temper real world uptake.

The upcoming ATS 2026 presentations look most relevant here, as they showcase new data on ARIKAYCE, post hoc insights on BRINSUPRI and real world bronchiectasis experience, all of which sit close to the heart of Insmed’s catalyst path. In particular, the ENCORE and ASPEN related readouts, together with the bronchiectasis underdiagnosis initiative, speak directly to how large and durable the addressable markets for these two drugs might actually become.

Yet against that opportunity, the safety profile of ARIKAYCE in real world use is something investors should be aware of...

Insmed's narrative projects $4.0 billion revenue and $979.9 million earnings by 2029.

Uncover how Insmed's forecasts yield a $212.50 fair value, a 83% upside to its current price.

Exploring Other Perspectives

Before this update, the most optimistic analysts were assuming revenue could reach about US$5.2 billion and earnings US$1.9 billion by 2029, so if you lean on that view you are effectively embracing a far more bullish catalyst set than the baseline, particularly around faster BRINSUPRI adoption and ARIKAYCE expansion, and this latest guidance reaffirmation may either reinforce or test how comfortable you really are with those expectations.

Explore 4 other fair value estimates on Insmed - why the stock might be worth just $204.75!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Insmed research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Insmed research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Insmed's overall financial health at a glance.

Want Some Alternatives?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 15 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.