Insmed (INSM) Is Up 6.8% After Strong ENCORE Data Boost ARIKAYCE’s MAC Expansion Prospects

Insmed Incorporated INSM | 162.43 | -1.47% |

- Insmed recently reported positive topline Phase 3b ENCORE results showing that adding once-daily ARIKAYCE to standard multidrug therapy improved respiratory symptoms and culture conversion rates in largely treatment-naïve MAC lung disease patients, with a safety profile consistent with prior experience.

- The company now plans supplemental regulatory filings in the U.S. and Japan in the second half of 2026, aiming to expand ARIKAYCE’s label from a refractory niche into the much larger population of patients with newly diagnosed MAC lung infections.

- Next, we will examine how the ENCORE data and planned MAC label expansion could reshape Insmed’s investment narrative and growth optionality.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 26 best rare earth metal stocks of the very few that mine this essential strategic resource.

Insmed Investment Narrative Recap

To own Insmed, you have to believe that brensocatib’s commercialization can support the company while ARIKAYCE evolves from a refractory niche into a broader MAC franchise. The ENCORE data strengthens the case for ARIKAYCE’s long-term role but does not change the near term focus on a successful U.S. brensocatib launch and the risk that payer access or regulatory timing could constrain that rollout.

Among recent developments, Insmed’s addition to the FTSE All-World Index in March 2026 stands out alongside ENCORE, as it may increase visibility just as investors reassess the balance between the brensocatib launch catalyst and execution risks on multiple new indications.

Yet behind the strong ENCORE headlines, investors should also be aware of the possibility that payer pushback on brensocatib reimbursement could...

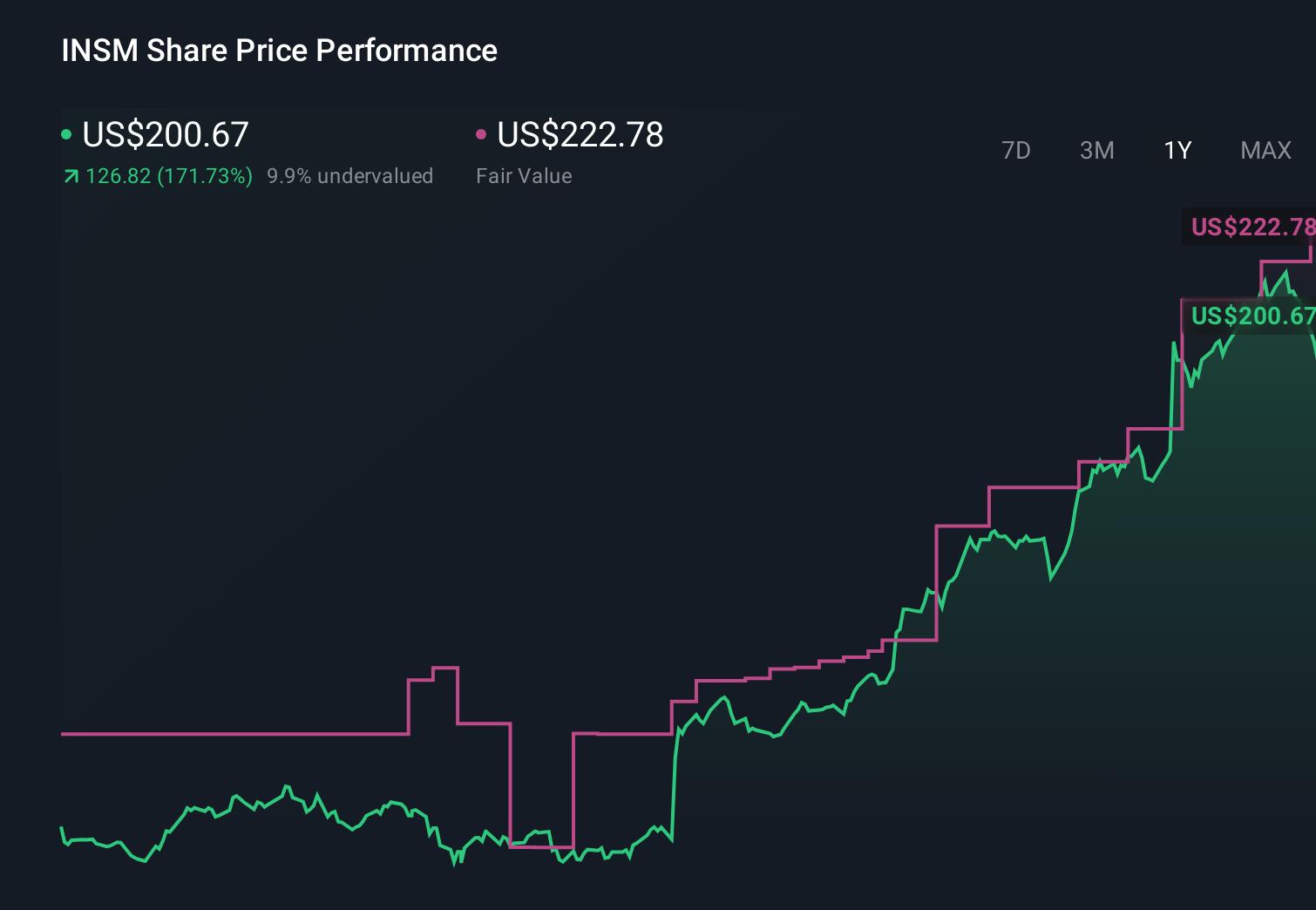

Insmed's narrative projects $3.9 billion revenue and $908.7 million earnings by 2029. This requires 85.3% yearly revenue growth and about a $2.2 billion earnings increase from -$1.3 billion today.

Uncover how Insmed's forecasts yield a $213.00 fair value, a 47% upside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span from about US$213 to over US$21,000 per share, showing just how far apart individual views can be. Against that backdrop, the anticipated U.S. launch of brensocatib as a key catalyst highlights why it can help to weigh several different opinions before forming a view on Insmed’s prospects.

Explore 4 other fair value estimates on Insmed - why the stock might be a potential multi-bagger!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Insmed research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Insmed research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Insmed's overall financial health at a glance.

Ready For A Different Approach?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

- Find 60 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.