Inspire Medical Systems (INSP) Is Down 18.8% After Cutting 2026 Outlook And Filing Share Offering – Has The Bull Case Changed?

Inspire Medical Systems, Inc. INSP | 0.00 |

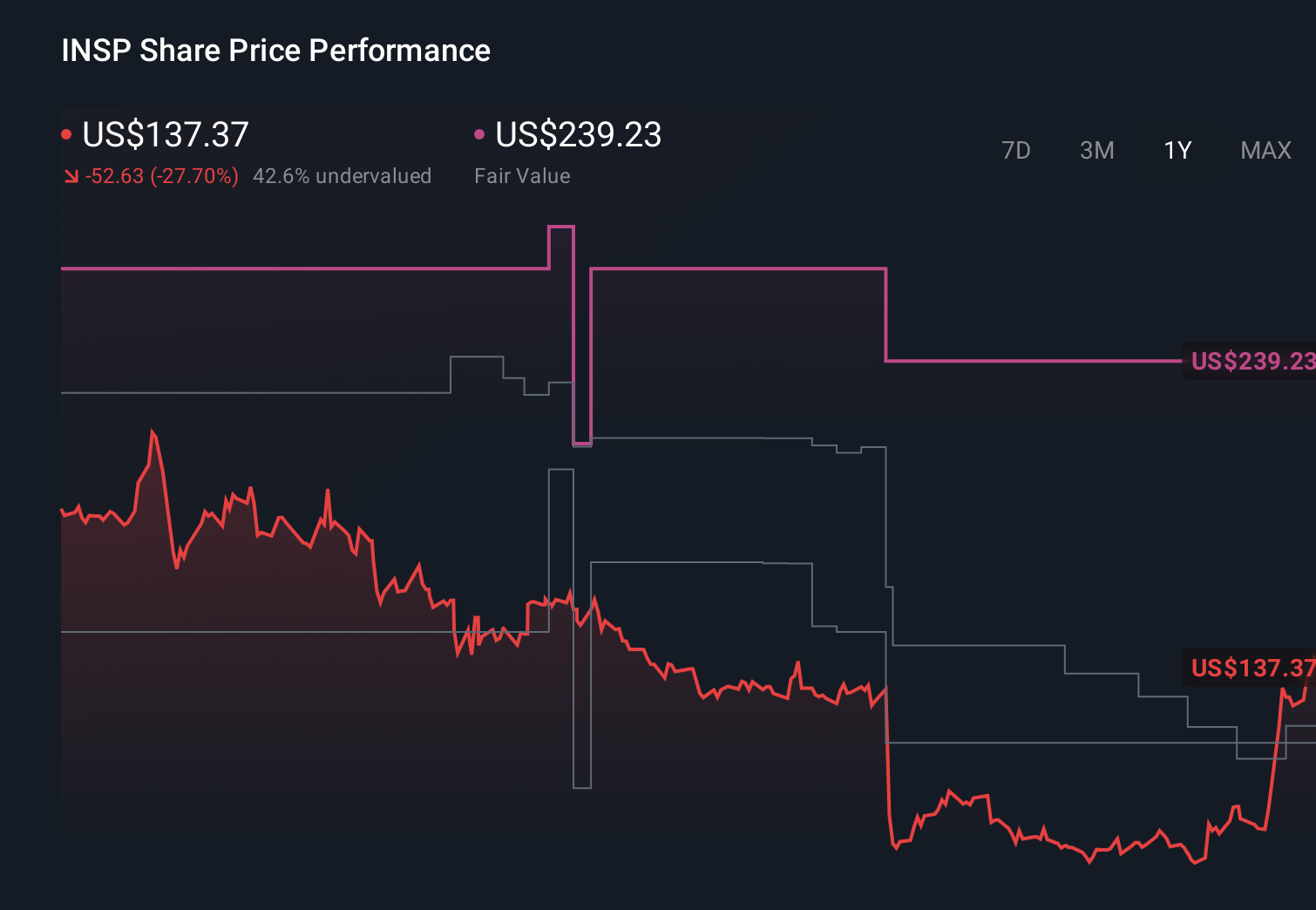

- Inspire Medical Systems recently reported first-quarter 2026 results, with sales of US$204.58 million but a shift from net income to an US$11.29 million net loss, and subsequently filed a US$118.82 million shelf registration for 2,600,000 common shares tied to an ESOP-related offering.

- A key development for investors is the company’s revised 2026 outlook, which now calls for US$825 million to US$875 million in revenue, a 4% to 10% decline versus 2025, alongside expected diluted EPS of US$0.07 to US$0.62 amid ongoing coding and reimbursement uncertainty.

- We’ll now examine how the reduced 2026 revenue guidance and reimbursement uncertainty interact with Inspire Medical’s prior investment narrative and assumptions.

Capitalize on the AI infrastructure supercycle with our selection of the 39 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Inspire Medical Systems Investment Narrative Recap

To own Inspire Medical Systems, you need to believe its implantable OSA therapy and Inspire V transition can outlast coding and reimbursement uncertainty. Right now, the biggest near term catalyst is clarity on coverage and payment for Inspire V, while the key risk is that payers remain slow or restrictive, keeping procedure volumes and margins under pressure. The latest guidance cut and first quarter loss directly highlight how central that reimbursement risk has become.

The new US$118.82 million shelf registration for 2,600,000 common shares, tied to an ESOP related offering, matters because it sits against a backdrop of weaker 2026 revenue guidance and a recent share price decline. For investors focused on catalysts, it adds another moving part to the story at a time when confidence already hinges on how quickly reimbursement issues for Inspire V can be worked through and whether earnings can stabilize.

Yet even with a clear medical need, investors should be aware that reimbursement and coding shifts could still materially affect Inspire’s growth potential and valuation...

Inspire Medical Systems' narrative projects $1.1 billion revenue and $97.5 million earnings by 2029. This implies 8.0% yearly revenue growth and a $47.9 million earnings decrease from $145.4 million today.

Uncover how Inspire Medical Systems' forecasts yield a $79.42 fair value, a 74% upside to its current price.

Exploring Other Perspectives

Before this setback, the most optimistic analysts were modeling roughly US$1.4 billion of revenue and US$157 million of earnings by 2028, so you can see how sharply opinions may diverge if reimbursement risk proves more persistent than that bullish path assumed.

Explore 9 other fair value estimates on Inspire Medical Systems - why the stock might be worth just $51.73!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Inspire Medical Systems research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Inspire Medical Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Inspire Medical Systems' overall financial health at a glance.

Want Some Alternatives?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.