Intapp And 2 Additional Stocks That May Be Priced Below Estimated Value

Klaviyo, Inc. Class A KVYO | 0.00 |

The United States market has shown impressive performance, rising 1.6% over the last week and climbing 28% in the past year, with earnings forecasted to grow by 17% annually. In light of these conditions, identifying stocks that may be priced below their estimated value can offer opportunities for investors seeking potential growth at a reasonable cost.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Workday (WDAY) | $157.23 | $311.80 | 49.6% |

| Uranium Energy (UEC) | $13.59 | $26.26 | 48.3% |

| ServiceNow (NOW) | $135.86 | $263.36 | 48.4% |

| Rayonier (RYN) | $20.54 | $40.26 | 49% |

| Merck (MRK) | $115.17 | $228.62 | 49.6% |

| Live Oak Bancshares (LOB) | $37.36 | $74.21 | 49.7% |

| Intapp (INTA) | $26.03 | $50.27 | 48.2% |

| First Merchants (FRME) | $39.53 | $76.26 | 48.2% |

| FB Financial (FBK) | $51.91 | $101.61 | 48.9% |

| AbbVie (ABBV) | $212.93 | $417.04 | 48.9% |

We'll examine a selection from our screener results.

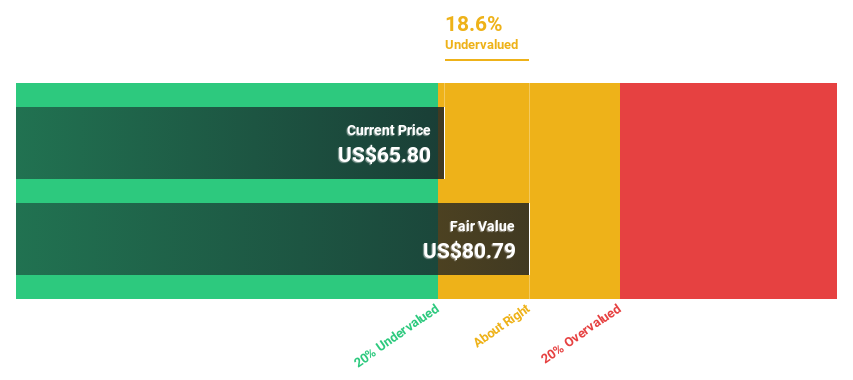

Intapp (INTA)

Overview: Intapp, Inc., operating through its subsidiary Integration Appliance, Inc., offers AI-powered solutions across the United States, the United Kingdom, and internationally with a market cap of approximately $1.78 billion.

Operations: The company's revenue comes from its Software & Programming segment, which generated $560.31 million.

Estimated Discount To Fair Value: 48.2%

Intapp is trading at US$26.03, significantly below its estimated future cash flow value of US$50.27, indicating it may be undervalued based on discounted cash flows. Recent client adoptions of Intapp's DealCloud and AI enhancements in Intapp Time suggest strong demand for its solutions, potentially supporting future growth. While revenue growth is forecasted at 13.6% annually, slower than 20%, the company's expected profitability within three years and high return on equity projection bolster its investment appeal.

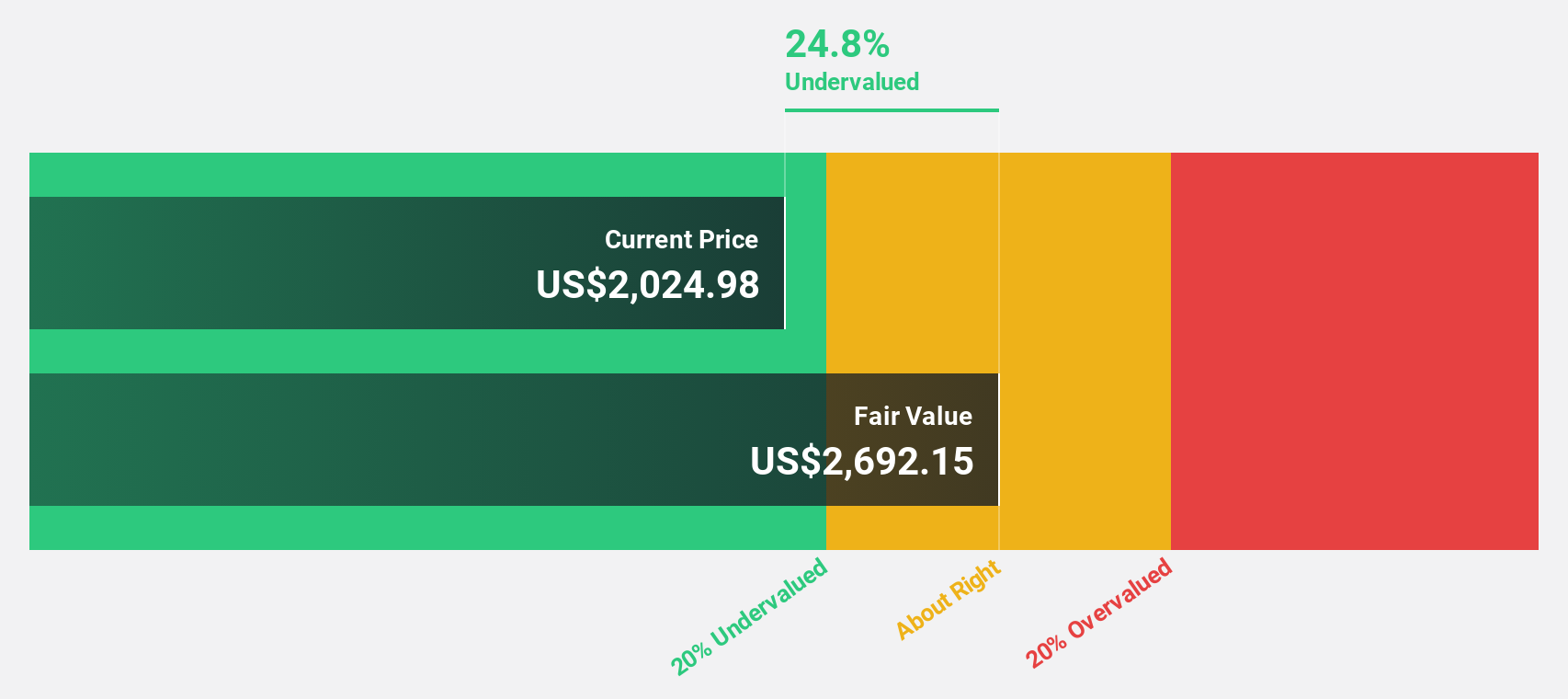

MercadoLibre (MELI)

Overview: MercadoLibre, Inc. operates online commerce platforms in Brazil, Mexico, Argentina, and internationally with a market cap of $85.96 billion.

Operations: The company generates revenue of $31.80 billion from its Internet Software & Services segment across various regions including Brazil, Mexico, and Argentina.

Estimated Discount To Fair Value: 42.9%

MercadoLibre, trading at US$1730.98, is undervalued compared to its future cash flow estimate of US$3030.07. Despite a decline in net profit margin from 9.2% to 6%, the company's earnings are projected to grow significantly at 26.94% annually, outpacing the broader US market's growth expectations. Revenue is also expected to increase by 19.9% per year, and analysts agree on a potential stock price rise of 28.1%.

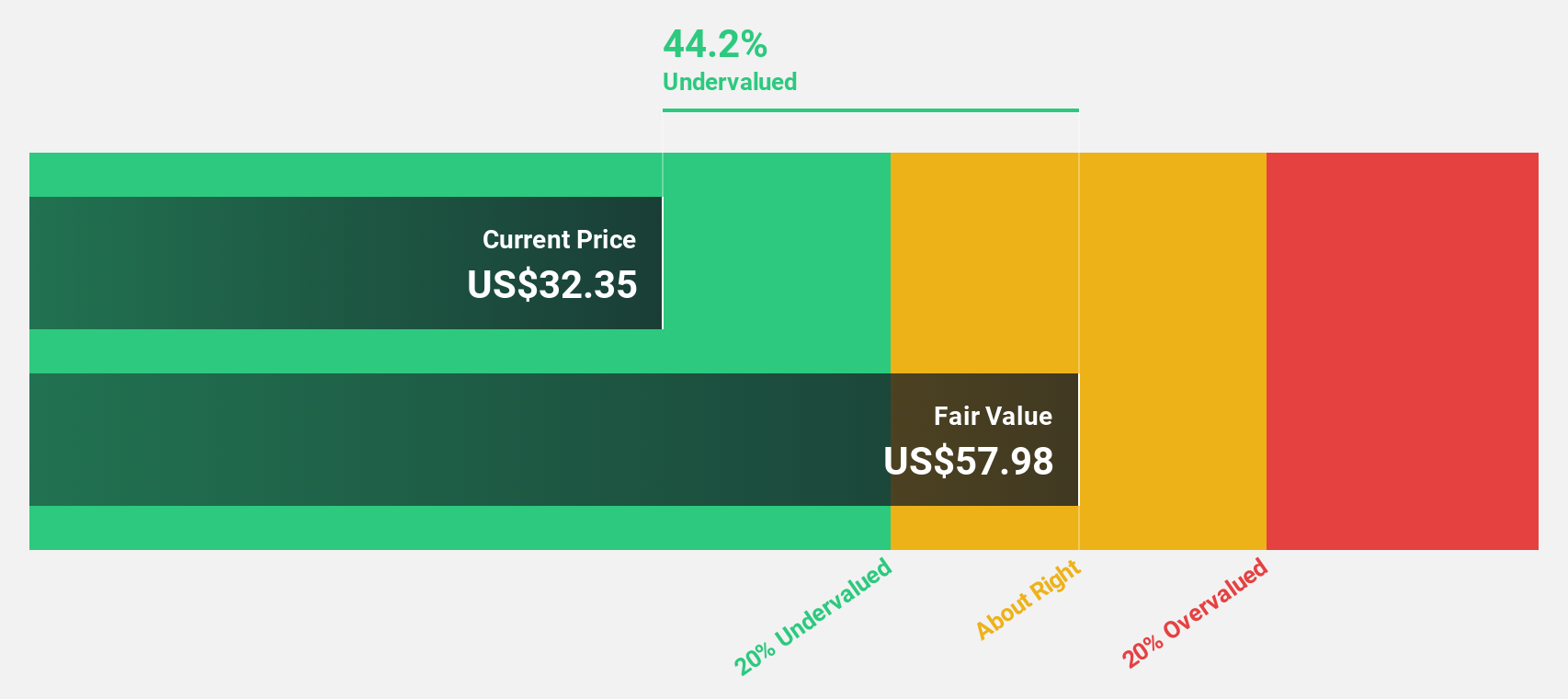

Klaviyo (KVYO)

Overview: Klaviyo, Inc. offers a cloud-based software-as-a-service platform globally, with a market cap of approximately $4.74 billion.

Operations: Revenue Segments (in millions of $): The company generates revenue primarily from its Internet Software segment, totaling $1.31 billion.

Estimated Discount To Fair Value: 42.4%

Klaviyo, trading at US$18.36, is significantly undervalued compared to its estimated future cash flow value of US$31.87. The company has demonstrated strong earnings growth, with a forecasted annual increase of 82.39%, and recently reported a positive net income of US$9.04 million for Q1 2026, reversing a loss from the previous year. Despite recent volatility in share price and executive changes, Klaviyo's strategic integrations and product innovations support its robust financial outlook.

Key Takeaways

- Get an in-depth perspective on all 137 Undervalued US Stocks Based On Cash Flows by using our screener here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.