Intapp (INTA): Evaluating Valuation After Q1 Results, Wider Net Loss, New Guidance, and Share Buyback Completion

Intapp, Inc. INTA | 25.04 25.04 | -2.53% 0.00% Pre |

Intapp (INTA) just reported first quarter results showing higher revenue compared to last year, but also posting a larger net loss. The company also shared fresh guidance for the next quarter and completed a major share buyback.

Intapp’s shares have rebounded impressively in the past month, with a 16% share price return following the release of Q1 results and the completion of a $50 million buyback. Despite short-term volatility, the company’s three-year total shareholder return of 97% highlights its long-term growth story. Investors are now watching to see if momentum returns after a challenging year.

If you’re looking to find stocks with strong growth potential and high insider participation, now’s an ideal moment to broaden your search and discover fast growing stocks with high insider ownership

With shares trading about 33% below the average analyst price target and annual revenue up over 12%, the key question now is whether Intapp presents a compelling value or if the market has already priced in the company’s future growth potential.

Most Popular Narrative: 24.6% Undervalued

According to the latest narrative, Intapp's fair value sits well above the current share price. This has fueled renewed debate on what could drive a major re-rating for the stock. Analysts have factored in new product launches, recent acquisitions, and a strengthened profitability outlook as key ingredients behind their calculation.

Intapp's recent investments in AI capabilities, including the launch of Intapp DealCloud Activator and the transformed Intapp Time product, are designed to drive client engagement and operational efficiencies. These innovations are expected to bolster revenue by enhancing product appeal and encouraging cloud adoption among existing and potential clients.

Want to unpack the ambitious assumptions behind this valuation spike? The most closely watched narrative is betting on profit margin shifts, bold revenue targets, and cloud-powered transformation. Curious how these pieces fit together and what future milestones are built in? Discover exactly what could propel Intapp’s value far beyond today’s share price.

Result: Fair Value of $57.13 (UNDERVALUED)

However, increased reliance on external partners and a difficult cloud transition could still threaten profit margins and slow Intapp's ambitious growth outlook.

Another View: Multiples Say Caution

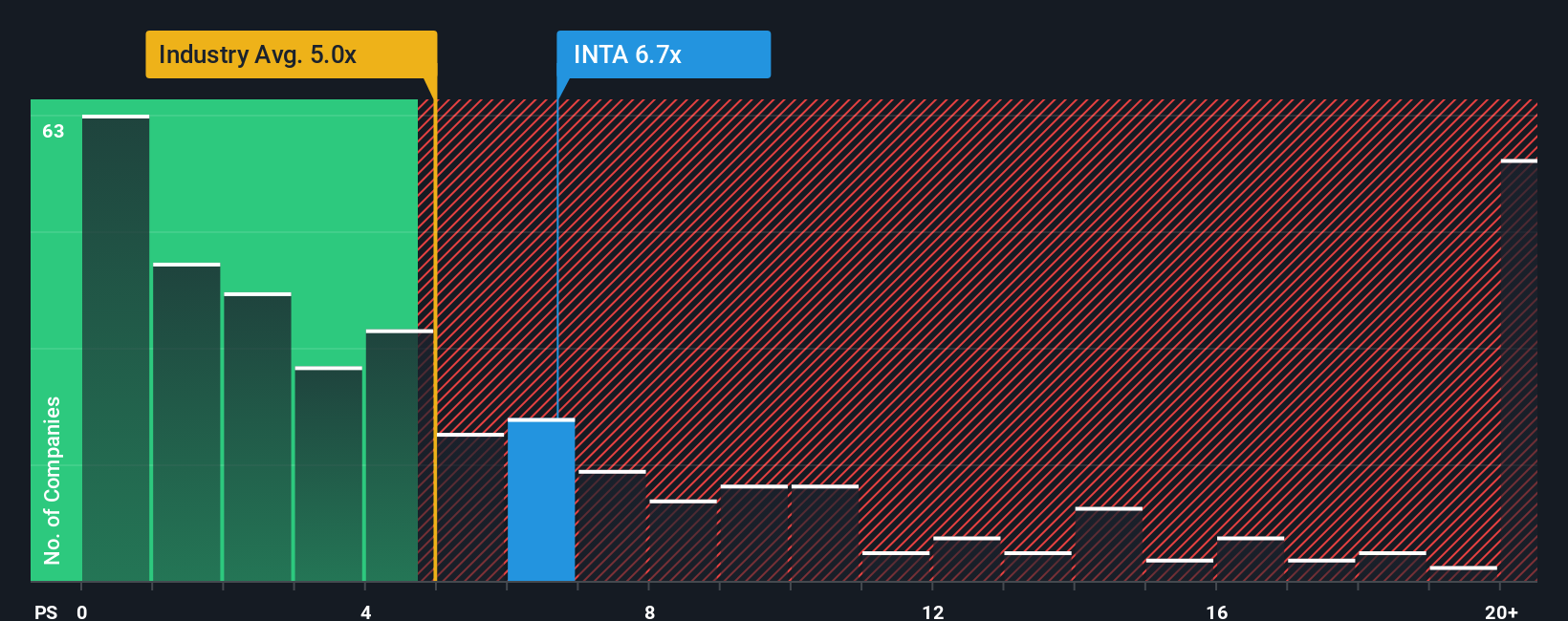

While analysts see Intapp as undervalued based on their growth forecasts, our market ratios suggest the opposite. Intapp trades at 6.7 times sales, which is well above the US Software industry average of 4.7 and its direct peer group at 6.2, as well as the fair ratio of 5.1. This premium could signal optimism, but it also means greater downside if results disappoint. Will the market’s expectations stay this high?

Build Your Own Intapp Narrative

If you’d rather test these numbers for yourself or challenge the prevailing consensus, you can analyze the data and craft a custom narrative in minutes, all with our Do it your way.

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Intapp.

Looking for More Investment Ideas?

Don’t let valuable opportunities slip through your fingers just because you stopped at one company. Use the right tools to uncover your next great investment move with Simply Wall Street’s expert-built screeners:

- Uncover strong cash-flow bargains by checking out these 906 undervalued stocks based on cash flows, and see which businesses could be poised for a re-rating.

- Target breakthrough trends in healthcare technology and get ahead of the curve with these 31 healthcare AI stocks as artificial intelligence transforms patient care and diagnostics.

- Lock in steady income by reviewing these 16 dividend stocks with yields > 3%, featuring top-yielding companies with a history of rewarding their shareholders.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.