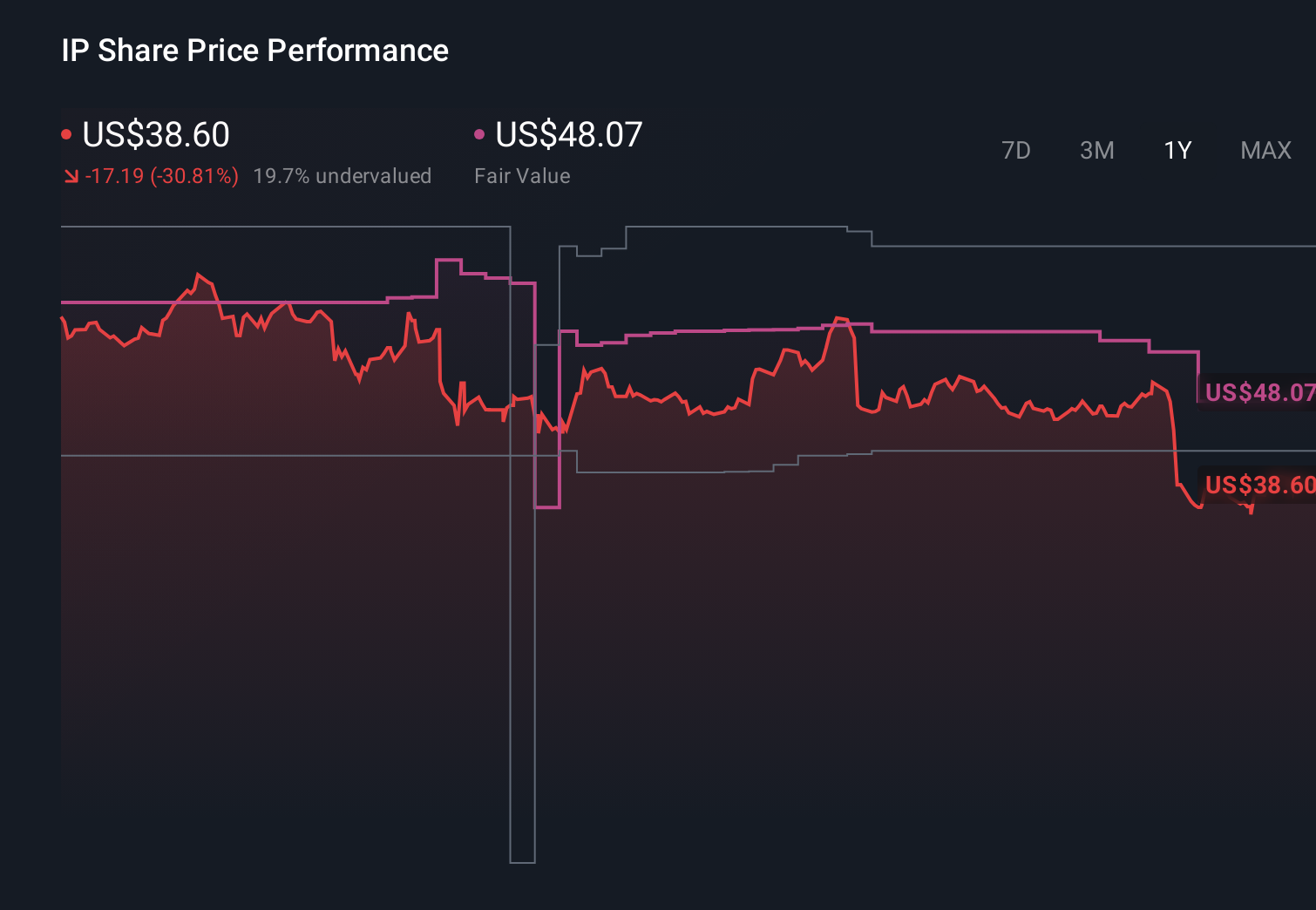

International Paper (IP) Is Up 5.1% After Closing Four Plants To Streamline Network Efficiency – Has The Bull Case Changed?

International Paper Company IP | 0.00 |

- International Paper recently announced plans to cease preprint operations at its Richwood, Kentucky facility and close plants in Aurora, Illinois; Elk Grove, California; and Barrington, New Jersey by the end of the third quarter of 2026 as part of a North American network optimization.

- The company aims to sharpen its cost position and expand capacity for sustainable packaging while transitioning affected customers to other regional facilities and providing support to displaced employees.

- Next, we’ll examine how these plant closures and network optimization efforts may influence International Paper’s investment narrative and turnaround prospects.

We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

International Paper Investment Narrative Recap

To own International Paper, you need to believe its shift toward higher value, fiber-based packaging and mill upgrades can eventually turn current losses into sustainable profitability. The announced North American plant closures fit into that wider optimization effort, but they do not fundamentally change the near term catalysts around cost-out execution or the key risk that complex asset closures and reliability projects could stumble, keeping margins and cash flow under pressure.

The most relevant recent update alongside these closures is International Paper’s decision to invest about US$225,000,000 in a new automated corrugated packaging facility in Rankin County, Mississippi. Together, shutting less efficient plants and building a modern site illustrate how the company is reshaping its footprint, which could reinforce the cost and reliability improvements that underpin its turnaround plan while also adding execution and capital intensity risk along the way.

Yet behind these efficiency gains, investors should be aware that...

International Paper's narrative projects $26.2 billion revenue and $1.7 billion earnings by 2029.

Uncover how International Paper's forecasts yield a $39.36 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting revenues around US$26,800,000,000 and earnings near US$2,200,000,000 by 2029, but the latest plant closures highlight how views on mill reliability and long term capital needs can differ sharply, and you should consider whether that bullish story still fits your own expectations.

Explore 4 other fair value estimates on International Paper - why the stock might be worth just $39.36!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your International Paper research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free International Paper research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate International Paper's overall financial health at a glance.

Looking For Alternative Opportunities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Capitalize on the AI infrastructure supercycle with our selection of the 51 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 30 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.