Intuitive Machines (LUNR) Valuation In Focus After New NASA Lunar Imaging Contracts

Intuitive Machines LUNR | 0.00 |

NASA imaging contracts put Intuitive Machines (LUNR) in focus for lunar infrastructure investors

Intuitive Machines (LUNR) has drawn fresh attention after being selected as prime contractor for NASA’s Lunar Reconnaissance Orbiter Camera and the ShadowCam instrument under two three year contracts totaling US$20.0 million.

Despite the 12.82% decline in the 1 day share price return to US$38.21, recent momentum has been strong, with a 49.14% 30 day share price return and a 247.05% 1 year total shareholder return suggesting sentiment has shifted sharply since earlier in the year.

If this surge in interest around lunar infrastructure has your attention, it could be worth widening your watchlist with 33 robotics and automation stocks

With Intuitive Machines now tied more closely to NASA and trading at US$38.21, questions turn to value: is a 1-year return above 200% leaving limited upside, or are markets only starting to price in future growth?

Most Popular Narrative: 66.1% Overvalued

At a last close of $38.21 versus a narrative fair value of $23.00, the most followed valuation story on Intuitive Machines argues the stock is well ahead of its fundamentals according to sorkdhkddlek.

Balancing High-Growth Potential with Capital Dilution Intuitive Machines (LUNR) has successfully shifted from a high-risk startup to a Lunar Infrastructure Prime, backed by a $943M backlog and a strategic pivot toward high-margin data services via the Lanteris acquisition. While the trajectory toward positive Adjusted EBITDA in 2026 is clear, the current stock price reflects a "perfection premium" that overlooks recent share dilution.

Read the complete narrative. Read the complete narrative.

This narrative leans heavily on rapid revenue expansion, a shift toward recurring lunar data services, and a richer margin profile that together underpin the $23.00 fair value call.

Result: Fair Value of $23.00 (OVERVALUED)

However, recent capital raises that expanded the share base, along with any setback in turning projected revenue into profitable contracts, could quickly challenge this overvaluation story.

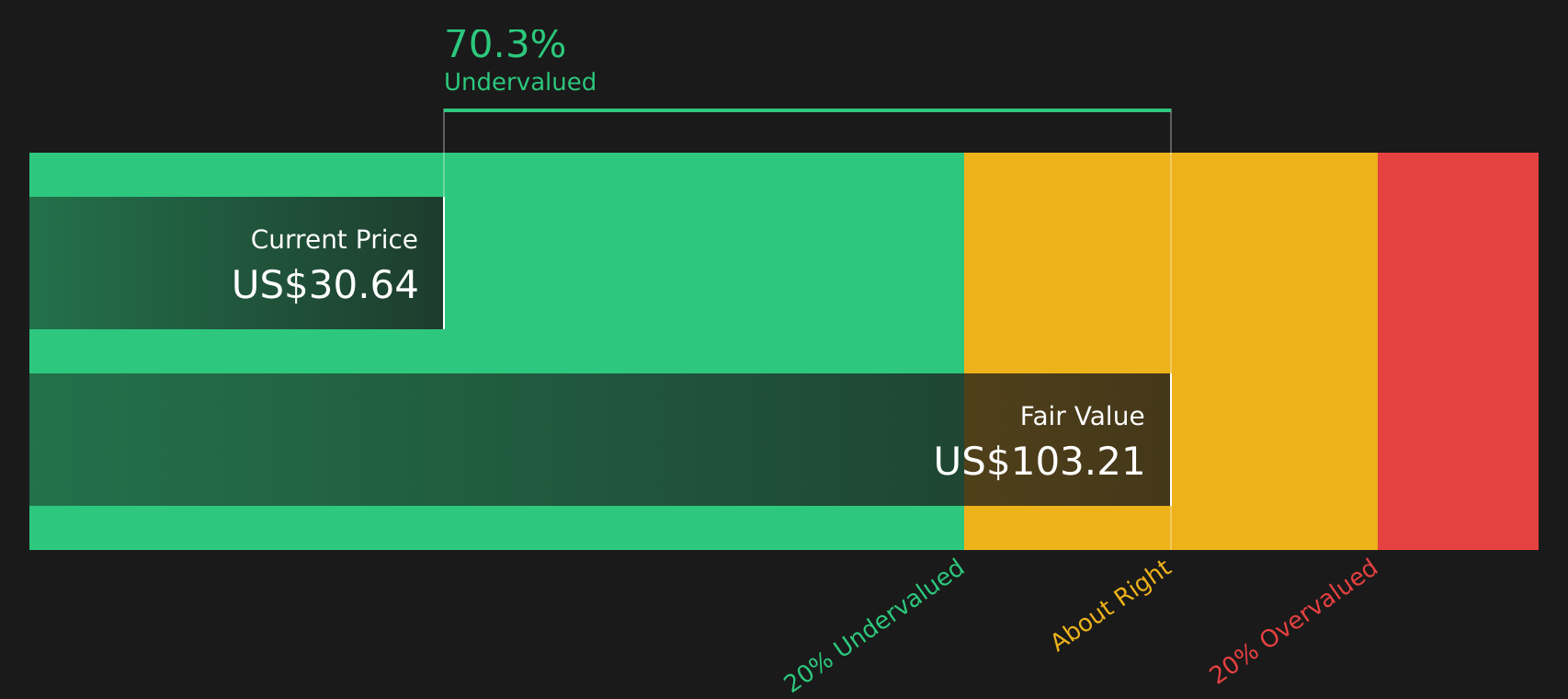

Another View: DCF Points the Other Way

While the popular narrative leans on a revenue multiple and lands at a fair value of $23.00, the SWS DCF model points in the opposite direction, with an estimate of $104.41 per share. One method flags rich pricing, and the other signals a discount, so which story do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Intuitive Machines for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on value and sentiment running hot, it makes sense to move quickly, pull up the numbers yourself, and stress test both sides of the story using 2 key rewards and 3 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that suit your style, so keep widening your search with focused, data driven screeners.

- Spot potential value opportunities early by scanning companies that score well on quality and price using the 47 high quality undervalued stocks

- Prioritise resilience by filtering for businesses with strong finances through the solid balance sheet and fundamentals stocks screener (45 results)

- Hunt for lesser known opportunities that still show solid fundamentals by checking the screener containing 22 high quality undiscovered gems

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.