Intuitive Surgical (ISRG) Could Be 20% Undervalued After Its Quarterly Beat

Intuitive Surgical, Inc. ISRG | 0.00 |

Intuitive Surgical (ISRG) is back in focus after a strong quarterly report, with revenue and earnings ahead of expectations, supported by higher procedure volumes and early uptake of its new da Vinci 5 system.

The strong quarter and launch momentum for da Vinci 5 have helped Intuitive Surgical’s share price post a 1-day return of 5.87% and a 7-day share price return of 5.27%. However, the year-to-date share price return is still down 24.19% and the 1-year total shareholder return is down 21.76%. Recent strength therefore comes after a weaker stretch, with longer term 3 and 5-year total shareholder returns of 28.59% and 34.42% respectively, suggesting more moderate gains over time.

If Intuitive Surgical’s recent move has you looking at other healthcare robotics opportunities, it is worth scanning the market using our screener of 29 robotics and automation stocks.

So with Intuitive Surgical posting solid quarterly beats yet still trading well below recent highs, should you see today’s valuation as a potential discount on a leading robotics platform, or as a price that already reflects expectations for its future performance?

Most Popular Narrative: 20% Undervalued

At a last close of $426.01 versus a fair value narrative of $532.46, Intuitive Surgical is framed as undervalued, with that gap explained through specific growth, margin and valuation assumptions in the narrative.

Over the next 5 years I calculate with (actual values from 18.01.26, price/shr at 533 USD): Revenue Growth p.a.: 12% (currently at 14.7%). We saw the peak of revenue growth with nearly 15%. Now even 12% is ambitious, but with the subscription-like revenues from spare parts and software licences, based on a still growing base of installed systems, it appears realistic. Profit Margin: 30% (currently at 28.6%), because spare parts in general have more margin than system sales, and the sales out of spare parts is still growing. Future P/E: 50 (currently at 69). High P/Es are typical for fast growers, but over time the P/E is expected to go down; I use 50 for the next 5 years and 40 for 10 years. Interest rate: 6.77% (same as current).

This narrative on Intuitive Surgical rests on a specific blend of steady revenue expansion, improving margins from recurring instruments and a premium future earnings multiple. It raises the question of which mix of growth and profitability assumptions is contributing most to that fair value estimate and how sensitive the outcome is if any of them change.

Result: Fair Value of $532.46 (UNDERVALUED)

However, this fair value story for Intuitive Surgical could be tested if procedure growth or recurring revenue trends soften, or if the assumed premium future P/E fails to hold.

Another View: Intuitive Surgical Through a P/E Lens

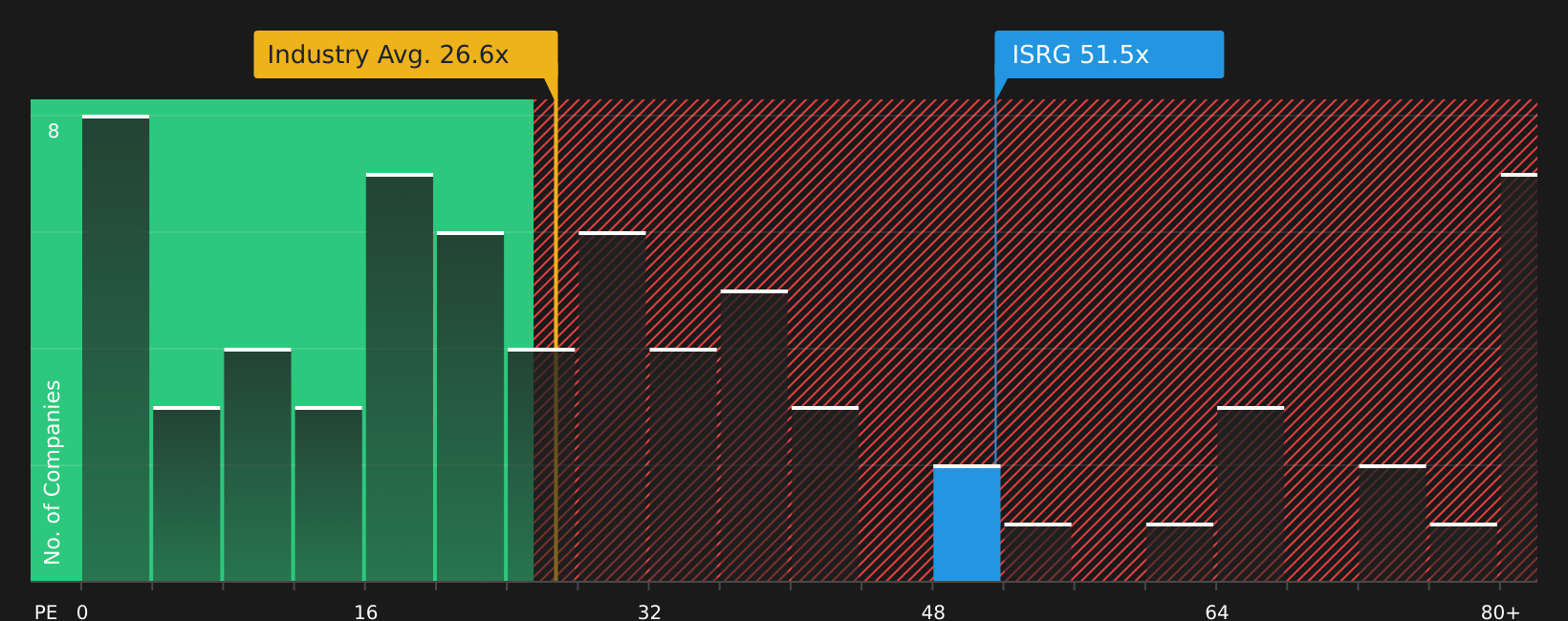

While one narrative frames Intuitive Surgical as around 20% undervalued, the market is currently paying a P/E of 50.6x, versus 26.5x for the US Medical Equipment industry and 26.3x for peers, and a fair ratio of 34.1x. That premium suggests downside risk if sentiment cools. Which story do you trust more?

Next Steps

With sentiment split between premium risks and fair value optimism around Intuitive Surgical, it makes sense to move fast and review the underlying numbers yourself. To see which factors are driving the upbeat case, take a closer look at the 4 key rewards.

Looking for more investment ideas beyond Intuitive Surgical?

If Intuitive Surgical has sharpened your focus on quality opportunities, do not stop here. Use the Simply Wall St Screener to uncover more targeted ideas across the market.

- Target higher quality at better prices by reviewing companies screened as 44 high quality undervalued stocks and see which ones deserve a place on your watchlist.

- Prioritise resilience by checking out 74 resilient stocks with low risk scores so you are not caught off guard by fragile balance sheets or inconsistent track records.

- Get ahead of the crowd with the screener containing 18 high quality undiscovered gems and spot stocks the wider market may not be focusing on yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.