IonQ’s SkyWater Deal Tests Vertically Integrated Quantum Platform Ambitions

IonQ, Inc. IONQ | 0.00 |

- IonQ (NYSE:IONQ) has agreed to acquire U.S. chip manufacturer SkyWater Technology in a deal valued at approximately $1.8b.

- The company plans to use the acquisition to build what it describes as the quantum sector's first fully vertically integrated, full stack platform.

- The transaction is intended to bring semiconductor production in house and support government and other highly regulated end markets.

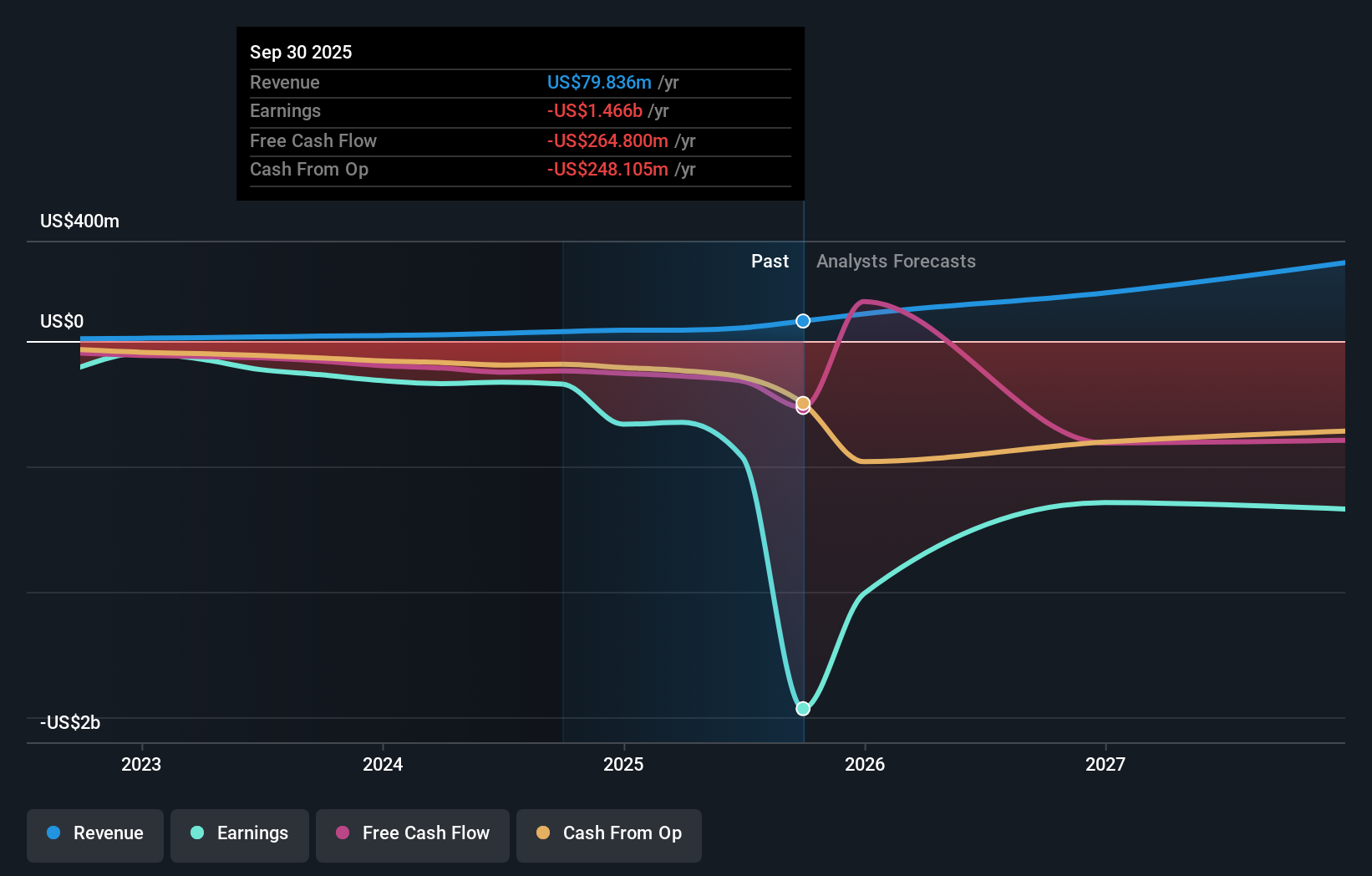

IonQ comes into this move with its shares at $45.8 and a 3 year return of 862.2%, along with a 281.7% return over 5 years. Over the past year the stock is up 15.8%, while year to date it shows a 2.1% decline and a 5.2% decline over the last week, highlighting the volatility in sentiment around NYSE:IONQ.

By combining quantum hardware design with domestic chip fabrication, IonQ is positioning itself as a full stack quantum provider that controls more of its own supply chain. For investors, this raises questions about execution risk, the integration of a capital intensive business such as semiconductor manufacturing, and the timing and extent of any impact on commercial quantum offerings and contracts.

Stay updated on the most important news stories for IonQ by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on IonQ.

IonQ’s plan to buy SkyWater for about US$1.8b would pull chip manufacturing directly into its quantum-computing stack, which could reduce design-to-tape-out times and give more control over cost and security, especially for government, aerospace and defense customers. For you as an investor, this points to IonQ trying to secure a chip supply that is tailored to its own trapped-ion architecture rather than relying on third-party foundries that might also be serving rivals such as IBM, Google and Microsoft-linked hardware partners.

IonQ’s “gorilla” narrative put to the test

The deal lines up closely with the existing IonQ narratives that frame the company as building a broad quantum platform across computing, networking, sensing and security, supported by a large cash “war chest.” Moving from a fabless model that relied on SkyWater as a partner, to owning the foundry outright, is a concrete step toward the vertically integrated, Nvidia-style playbook described in prior narratives and could be viewed as an attempt to widen that technology and supply-chain moat.

Risks and rewards investors should weigh

- ⚠️ Integration risk: combining a capital intensive semiconductor foundry with IonQ’s existing quantum-focused operations could keep losses high if costs run ahead of new revenue.

- ⚠️ Dilution and funding: the cash and stock structure, plus IonQ’s history of shareholder dilution, means existing holders may see their ownership share reduced if more equity is issued to support the enlarged group.

- 🎁 Vertical control: owning a trusted, U.S.-based fab with government accreditations may help IonQ secure long-duration contracts in sensitive sectors and tighten its position against peers like IBM and Alphabet’s quantum units.

- 🎁 Roadmap alignment: management expects the deal to accelerate testing of larger quantum processing units around 2028, which, if executed well, could reinforce IonQ’s technical differentiation.

What to watch from here

From here, it is worth tracking closing progress on the SkyWater deal, any updates to IonQ’s quantum hardware roadmap, and how management talks about profitability and capital needs once the foundry is consolidated. If you want to see how this fits into the longer-term story that other investors are debating, check community narratives on IonQ’s dedicated page.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.