Iridium Communications (IRDM) Draws A $54 Offer, Is The Stock Now Overvalued?

Iridium Communications Inc. IRDM | 0.00 |

Iridium Communications (IRDM) is back in focus after Rocket Lab agreed to acquire the company in a cash and stock deal valued at about $6 billion, which implies a price of roughly $54.00 per Iridium share.

That offer has arrived after a powerful run in Iridium Communications’ stock, with a year to date share price return of 196.11% and a 90 day share price return of 57.31%, even though the 3 year total shareholder return is down 7.75% and the 1 year total shareholder return sits at 68.52%. This suggests momentum has picked up recently as investors reassess the company’s prospects and risk profile in light of the Rocket Lab deal and ongoing IoT product and partnership announcements.

If this kind of move has you looking for what else might be setting up for a re-rating, it could be worth scanning 20 top founder-led companies

The question now is whether Iridium Communications’ surge toward the Rocket Lab offer mostly reflects improving fundamentals and IoT traction, or whether sentiment around the pending deal is doing most of the heavy lifting on price.

Most Popular Narrative: 38.9% Overvalued

Compared with the latest Simply Wall St fair value estimate of $37.88, Iridium Communications at a last close of $52.59 is priced well above what the most followed narrative implies. This puts the current market reaction to the Rocket Lab offer in sharp focus.

Rapidly expanding adoption of satellite-based IoT, autonomous systems, and remote monitoring, coupled with the rollout of new Iridium Certus IoT products and NTN Direct services, positions Iridium to benefit from the ongoing explosion of global device connectivity, underpinning long-term recurring revenue and higher-margin service growth.

Want to understand why this growth story still produces a lower fair value than today’s price? The narrative leans on rising margins, steadier cash generation and a richer future earnings multiple. Curious which assumptions really move the needle in that model and how they stack up against the latest Rocket Lab terms? The full breakdown joins the dots.

Result: Fair Value of $37.88 (OVERVALUED)

However, there are still clear weak spots, including slowing IoT service momentum and rising competition in direct to device offerings, which could challenge Iridium Communications’ upbeat narrative.

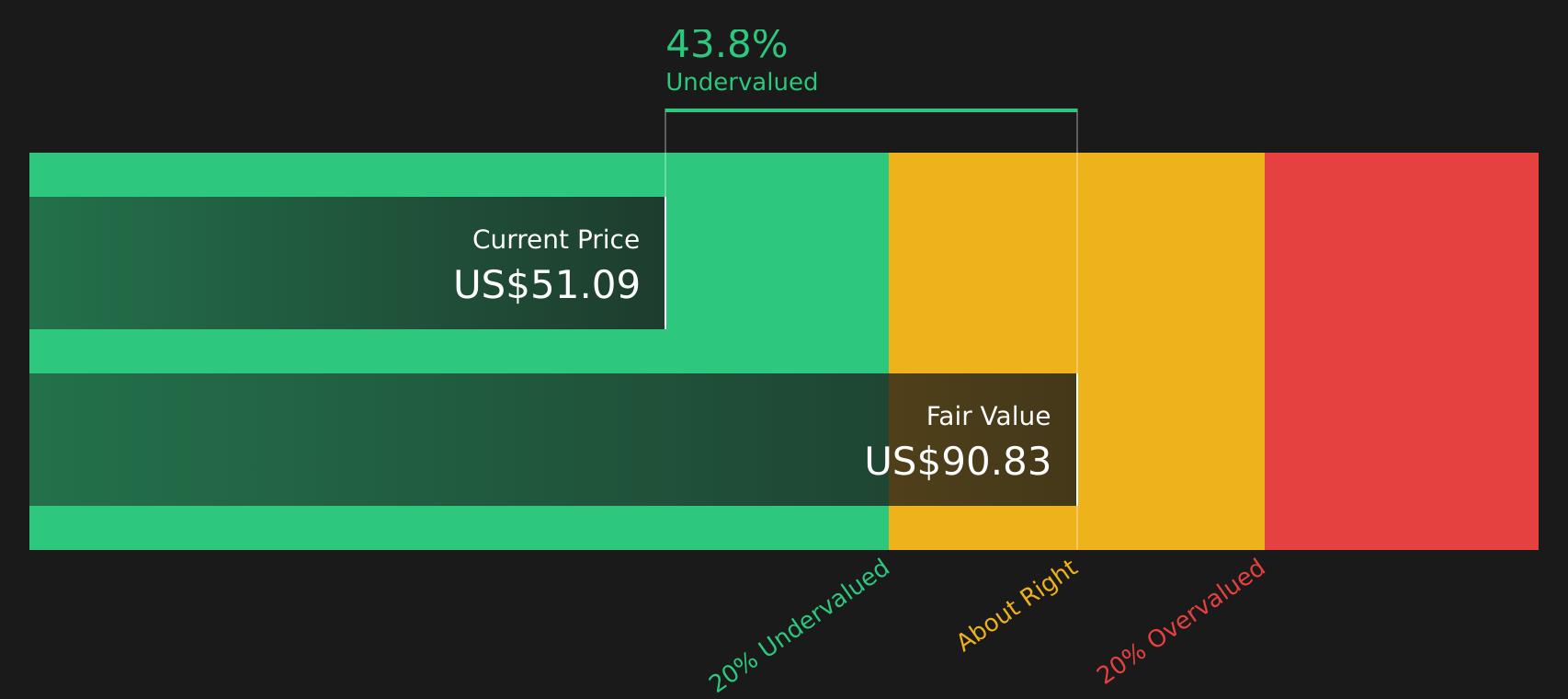

Another View: Iridium Communications Through a Cash Flow Lens

The first narrative around Iridium Communications leans on analyst targets and earnings multiples that suggest the stock is priced well above a $37.88 fair value. Yet our DCF model tells a very different story, indicating a future cash flow value of $90.06 per share, well above the current $52.59 price. That split raises a simple question: which signal do you trust more, the cash flows or the consensus?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Iridium Communications for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the split mood in this Iridium Communications story has you undecided, it is worth acting soon and weighing the trade off between caution and optimism using the same tools investors are already using to assess its 2 key rewards and 2 important warning signs via 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Iridium Communications?

If Iridium Communications has sharpened your focus on opportunity and risk, do not stop here. Use the Simply Wall St screener to keep upgrading your watchlist.

- Target resilient cash generators by scanning companies with the solid balance sheet and fundamentals stocks screener (47 results).

- Hunt for mispriced opportunities by reviewing the 41 high quality undervalued stocks before others catch on.

- Prioritize capital preservation by assessing companies in the 74 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.