Iridium (IRDM) Stock Looks Strong On Cash Flow But Rich On Earnings

Iridium Communications Inc. IRDM | 0.00 |

Iridium Communications has become a valuation puzzle after a powerful run, with a Discounted Cash Flow (DCF) intrinsic value estimate pointing to meaningful upside while broader checks and market multiples suggest the stock is not obviously cheap.

- Year to date, Iridium Communications is up 208.8%, which puts extra focus on whether today’s price already reflects much of the good news in the story.

- The agreed US$8b cash and stock acquisition by Rocket Lab can anchor expectations for future cash flows, while integration risks and deal approval uncertainty may cap how much value investors are willing to pay for the stock today.

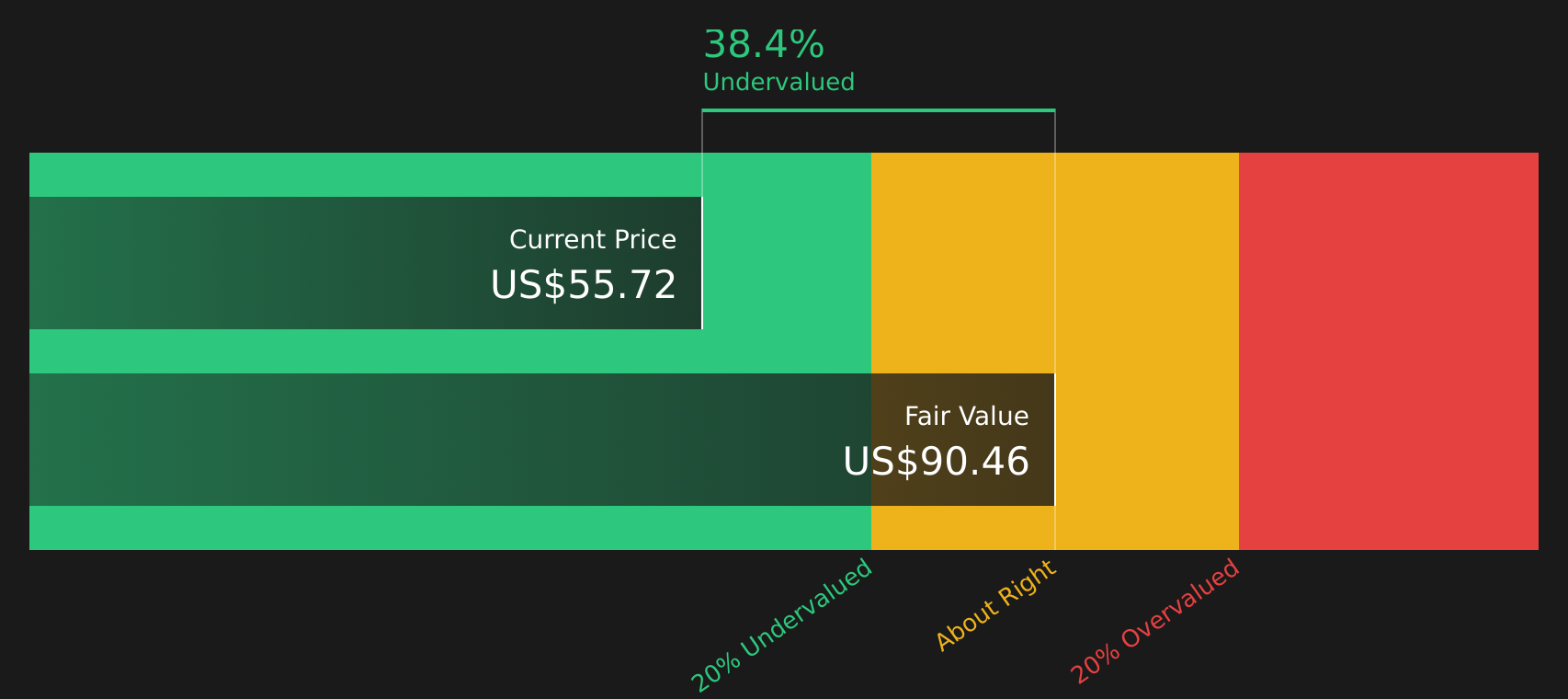

- The stock passes only 2 of 6 valuation checks on Simply Wall St’s framework, which leans toward Iridium Communications not being a clear bargain overall, even though the DCF suggests it is undervalued by 37.6%.

For investors, the debate is whether Iridium Communications’ current price offers enough margin of safety when the DCF points to undervaluation but the low score and richer multiples point the other way.

Is Iridium Communications Still Cheap on Cash Flow?

The Discounted Cash Flow (DCF) model values Iridium Communications by projecting its future cash generation and discounting it back to today. On this measure, Iridium Communications is treated as a business with positive, growing cash flows, with latest twelve month free cash flow of about $323.0 million feeding into a 2 Stage Free Cash Flow to Equity model. That stream of cash flows produces an estimated intrinsic value of about $87.85 per share in $.

Compared with the current share price implied by Rocket Lab’s agreed $8b cash and stock offer, which values Iridium Communications at $81 per share, the DCF suggests the stock is 37.6% undervalued. The Rocket Lab acquisition announcement helps explain why the market is willing to pay up for Iridium Communications. However, the DCF still indicates additional value supported by projected cash flows beyond the deal terms.

Overall, the Discounted Cash Flow (DCF) work up indicates Iridium Communications screens as undervalued relative to its estimated intrinsic worth.

Our Discounted Cash Flow (DCF) analysis suggests Iridium Communications is undervalued by 37.6%. Track this in your watchlist or portfolio, or discover 43 more high quality undervalued stocks.

Is Iridium Communications Getting Expensive on Earnings?

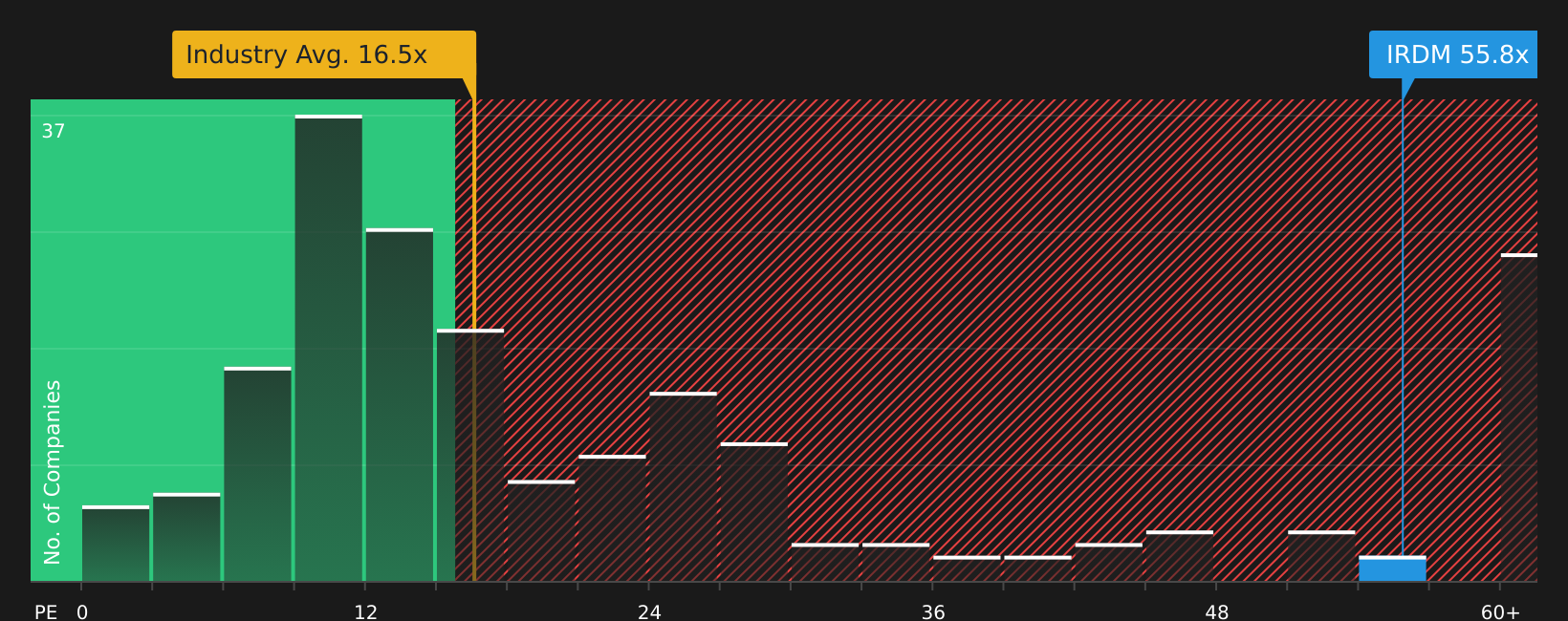

The P/E ratio is a useful cross check for Iridium Communications because earnings are a key focus for many satellite and telecom investors. On this lens, Iridium Communications trades at about 54.9x earnings, compared with an industry average Telecom P/E of roughly 16.7x and a peer group average near 8.9x. That already places the stock on a substantial premium to both its broad sector and more direct peers.

The tailored fair P/E multiple for Iridium Communications, which adjusts for factors such as profitability, size and risk, is estimated at about 19.9x. The current 54.9x therefore sits far above the level this framework would usually ascribe, indicating that investors are paying a high price for each dollar of earnings despite the DCF suggesting upside to intrinsic value. The gap indicates that the expectations built into the earnings multiple are demanding.

On a P/E basis, Iridium Communications currently appears overvalued relative to both sector benchmarks and its modelled fair multiple.

The Iridium Communications Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Iridium Communications pick up where this valuation puzzle leaves off by spelling out which future paths for growth, margins and earnings would need to play out for the stock to be worth materially more or less than today's price. They sit within the Community page for Iridium Communications' stock. Rather than relying on a single multiple or model output, each narrative lays out the assumptions behind its fair value so you can compare them with the company’s reported results over time.

One of the top community narratives on Iridium Communications: 45% overvalued

"Accelerating shifts to lower-value plans, slowing IoT growth, adoption delays, rising competition, and heavy investment requirements threaten Iridium's revenue growth, margins, and long-term financial health."

Do you think there's more to the story for Iridium Communications? Head over to our Community to see what others are saying!

The Bottom Line

For Iridium Communications, the Discounted Cash Flow (DCF) work suggests meaningful intrinsic value support, yet the market multiple view points to an overvalued stock on earnings. That split reflects a cash flow profile that screens attractive against a P/E that bakes in high expectations versus peers. With the broader valuation checks still weak despite a positive DCF signal, the key question is whether Iridium Communications can deliver the growth, margins and cash generation implied by today’s earnings multiple, or whether the current premium is the market correctly pricing in execution and integration risks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.