Is 3M’s Restructuring Driving Real Value After a 38% Stock Surge?

3M Company MMM | 145.70 | +0.32% |

If you're holding 3M stock or considering jumping in, you already know it's not just another ticker. In the past year, shares have soared 38.4%, and that's after a robust 13.3% pop over just the last week. Even looking back five years, 3M has delivered more than 56% total return. Clearly, something is propelling the stock, whether it's shifting investor sentiment or reactions to recent headlines.

It’s not just market momentum fueling the latest spike. Recent news around 3M’s restructuring plans and ongoing portfolio adjustments have shown the company is serious about streamlining operations and unlocking growth. Investors seem to be taking notice, with risk perceptions evolving as these changes unfold. The longer-term trend, marked by an 88.2% gain in just three years, hints at a business that’s both resilient and capable of surprising the market, often when it counts.

With the stock closing most recently at $171.60, many are asking the million-dollar question: Is 3M undervalued, overvalued, or somewhere in between? Based on our value score system, 3M is currently undervalued in 2 out of 6 checks, a score of 2. But, as with all things valuation, the answer isn’t as simple as running down a checklist. Let’s dig into the different ways investors assess 3M’s worth, and why there might be an even smarter approach still to come.

3M scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: 3M Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future cash flows and then discounting those back to today’s dollars. In simple terms, it asks what all of 3M’s expected future free cash flows are worth right now.

For 3M, analysts project free cash flow to rise from its most recent level of $1.25 Billion to as much as $4.90 Billion by 2029. The DCF considers both these near-term expert projections and, for years beyond 2029, Simply Wall St extrapolations. Over the next ten years, free cash flow is expected to follow a steady upward trajectory, driven by restructuring efforts and potential growth opportunities.

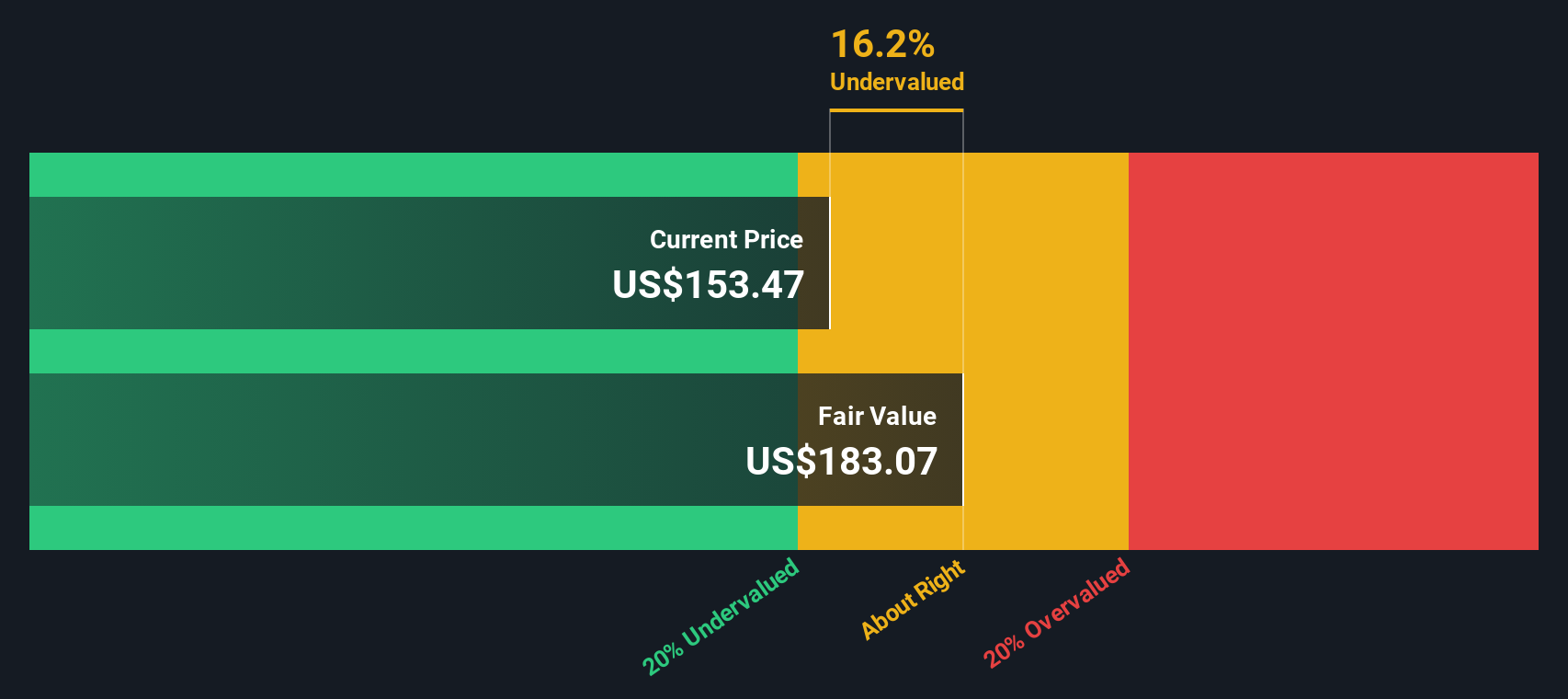

Based on this model, 3M’s estimated intrinsic value per share comes out to $193.68. At the latest closing price of $171.60, this suggests 3M stock is trading at an 11.4% discount to fair value, meaning the market is undervaluing the company’s future cash-generating potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests 3M is undervalued by 11.4%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: 3M Price vs Earnings (PE)

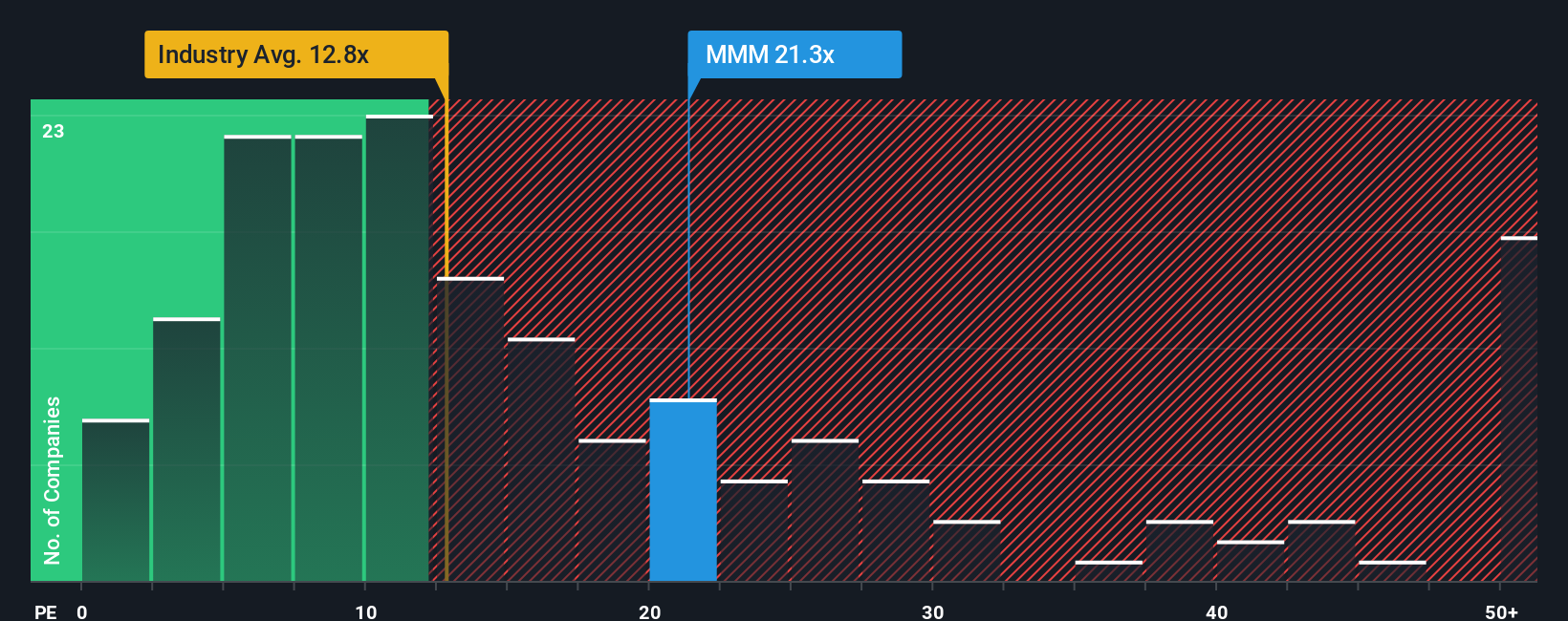

The Price-to-Earnings (PE) ratio is a popular and practical way to value profitable companies like 3M because it directly links a company’s share price to its per-share earnings. It’s a quick reality check for investors: are you paying a reasonable price for each dollar of earnings? The “right” PE ratio isn’t set in stone, as it depends heavily on expectations for a company’s growth, as well as the perceived risks. Higher growth and lower risk typically justify a higher PE, while slower growth or higher risk lead investors to expect a lower multiple.

3M currently trades at a PE of 26.8x, which is a bit above its peer average of 26.2x and markedly above the Industrials sector average of 12.9x. This might raise eyebrows, but not all companies (or industries) are created equal. That is where the concept of a “Fair Ratio” comes in. Simply Wall St’s proprietary Fair Ratio for 3M is 31.7x, calculated using an in-depth formula that takes into account the company’s earnings growth outlook, profit margins, size, industry dynamics, and specific risk factors.

By weighing all these fundamentals, the Fair Ratio offers a more precise target than a simple comparison to peers or sector averages. In 3M’s case, the Fair Ratio is quite close to its current PE, suggesting the market price is generally in line with what would be expected for a business with its characteristics and prospects.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your 3M Narrative

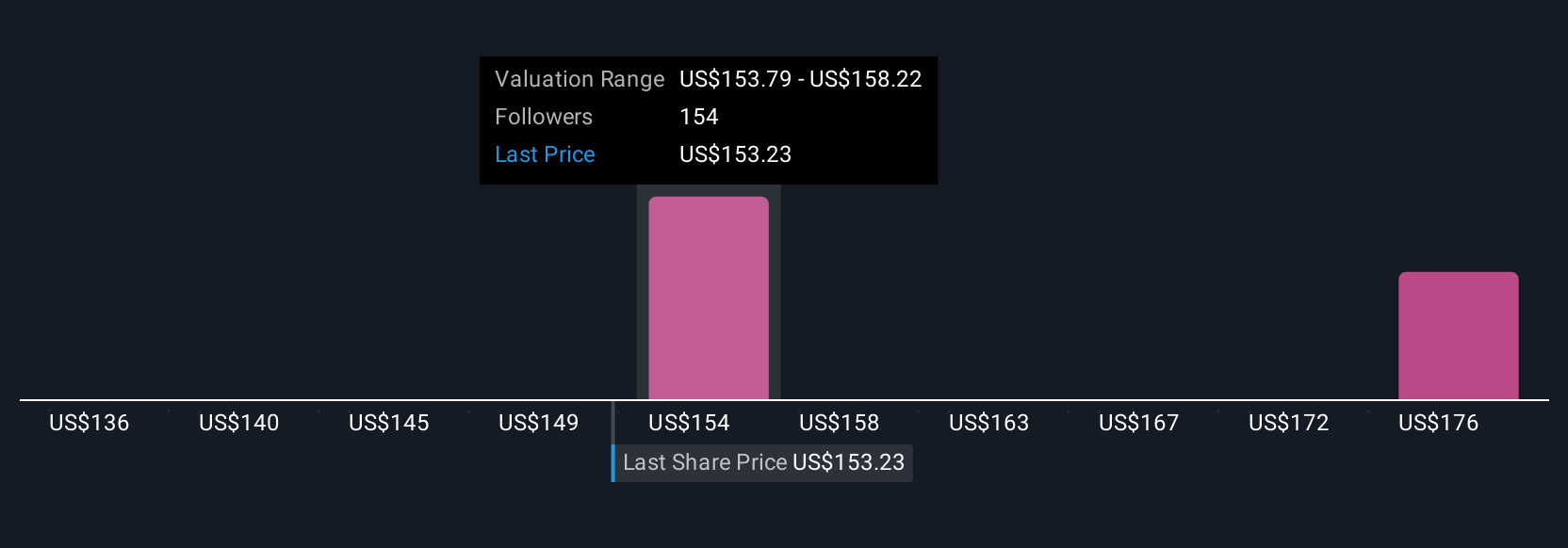

Earlier we mentioned that there’s an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is your personal story and convictions about a company like 3M, anchored in numbers, but shaped by your view of its future, such as what you believe revenue, earnings, and margins could be. Simply put, Narratives connect the company’s story to a financial forecast, and then to your own estimate of fair value.

Narratives are easy to use and available to everyone on Simply Wall St’s Community page, where millions of investors share perspectives. By building your Narrative, you clarify why you think the stock is a buy, sell, or hold, comparing your fair value against the current price and adjusting your stance as new news or earnings emerge. Narratives update automatically as key facts change, giving you a dynamic, real-time way to keep your thinking relevant and actionable.

For example, two different investors looking at 3M today could reach very different Narratives. One may be optimistic about innovation and margin expansion, arriving at a fair value above $187.00, while another, focused on ongoing legal and operational risks, might see a fair price closer to $101.00.

Do you think there's more to the story for 3M? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.