Is Activist Push For Oncor Spin Off And New Debt Deal Altering The Investment Case For Sempra (SRE)?

Sempra SRE | 0.00 |

- In early June 2026, activist investor Voss Capital publicly urged Sempra to unlock shareholder value by pursuing a tax-free spin-off of its majority-owned Texas utility, Oncor, while Sempra also completed a US$1.00 billion senior unsecured floating-rate note offering due January 7, 2028.

- By pushing for an Oncor separation that would isolate California wildfire exposure and simplify Sempra’s three-part structure, Voss Capital is directly challenging how the company balances growth, risk, and capital allocation across its regulated utilities and infrastructure businesses.

- We’ll now examine how Voss Capital’s proposed Oncor spin-off could reshape Sempra’s investment narrative around regulated growth, risk concentration, and capital deployment.

Find 46 companies with promising cash flow potential yet trading below their fair value.

Sempra Investment Narrative Recap

To own Sempra, you need to believe in the long-term value of regulated utility and infrastructure assets in California and Texas, despite regulatory, wildfire and capital-intensity pressures. The Voss Capital campaign to spin off Oncor, alongside Sempra’s new US$1,000,000,000 floating-rate note due 2028, does not yet change the key near-term catalyst around how management prioritizes capital across utilities and LNG, or the central risk from potential regulatory and wildfire-related outcomes in California.

Among recent developments, Voss Capital’s push to separate Oncor is most directly tied to today’s debate, because it concentrates attention on Texas rate base growth, regulatory changes and how much risk investors want tied to California wildfire exposure. How Sempra responds could influence perceptions of its ability to fund planned utility and LNG capital spending while preserving balance sheet flexibility and supporting its stated earnings guidance range over the next few years.

Yet investors should also be aware that California wildfire and policy risks could still materially affect...

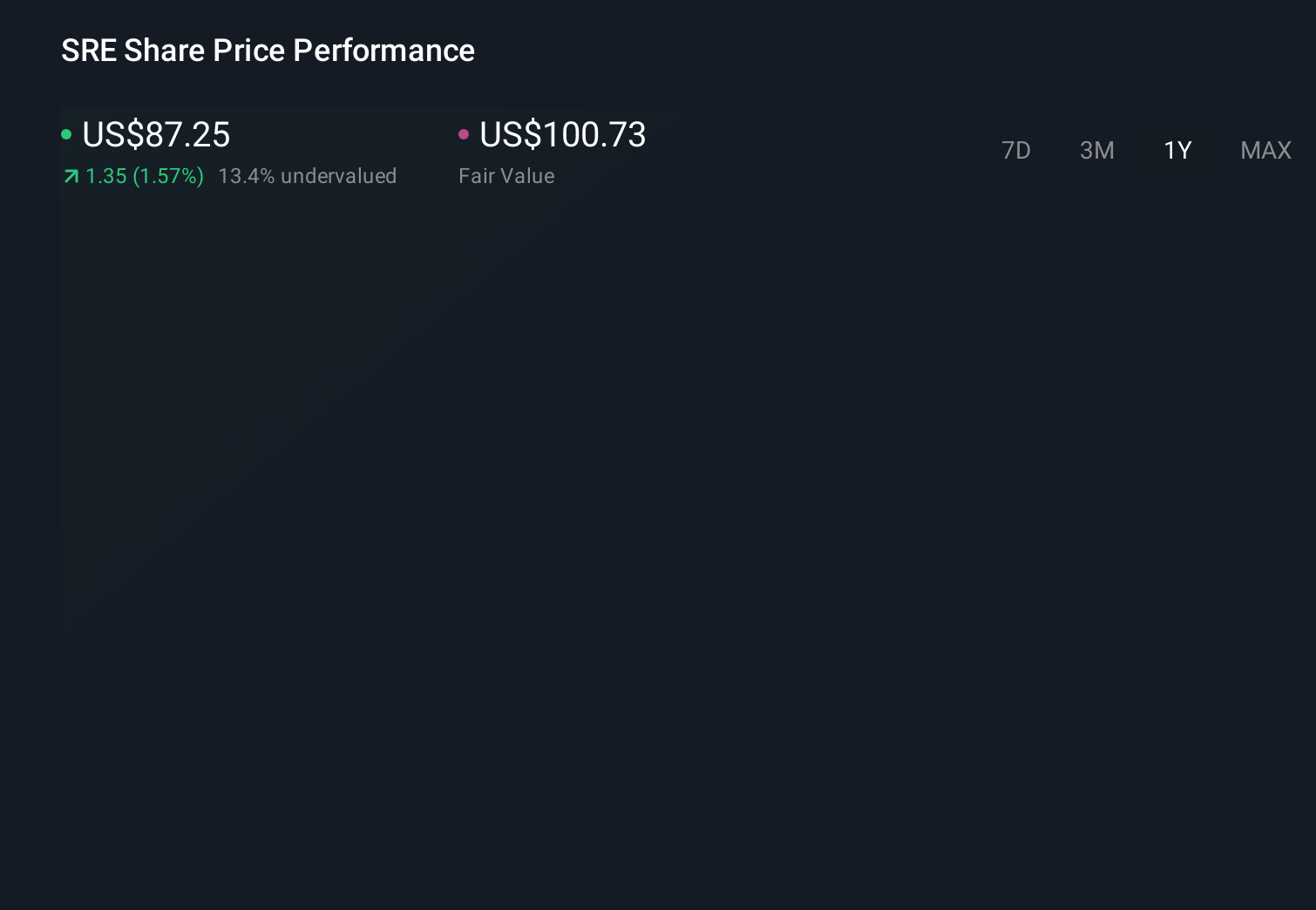

Sempra's narrative projects $14.3 billion revenue and $4.1 billion earnings by 2029.

Uncover how Sempra's forecasts yield a $103.62 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span roughly US$51 to US$104 per share, showing how far apart individual views can be. Against that backdrop, the debate over separating Oncor from Sempra’s California wildfire exposure gives you very different possible paths for future earnings resilience, so it is worth examining several of these perspectives before deciding what you think the business is really worth.

Explore 2 other fair value estimates on Sempra - why the stock might be worth 44% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Sempra research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Sempra research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sempra's overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.