Is AerCap Holdings (AER) Still Attractively Priced After Doubling Over Five Years?

AerCap Holdings NV AER | 139.18 | -0.56% |

- If you are wondering whether AerCap Holdings at around US$141.84 is still reasonably priced or already stretched, you are asking the right question for this stock.

- The share price has been flat over the past month, with a 0.0% 30 day return, but the longer term picture includes a 48.0% 1 year return and a very large 5 year gain of about 2x.

- Recent investor attention has focused on AerCap's role as a major aircraft lessor, especially in the context of fleet renewals, aircraft trading activity, and ongoing discussions around airline capacity and financing. These themes have kept the stock in the conversation as markets reassess risk and potential across aviation related names.

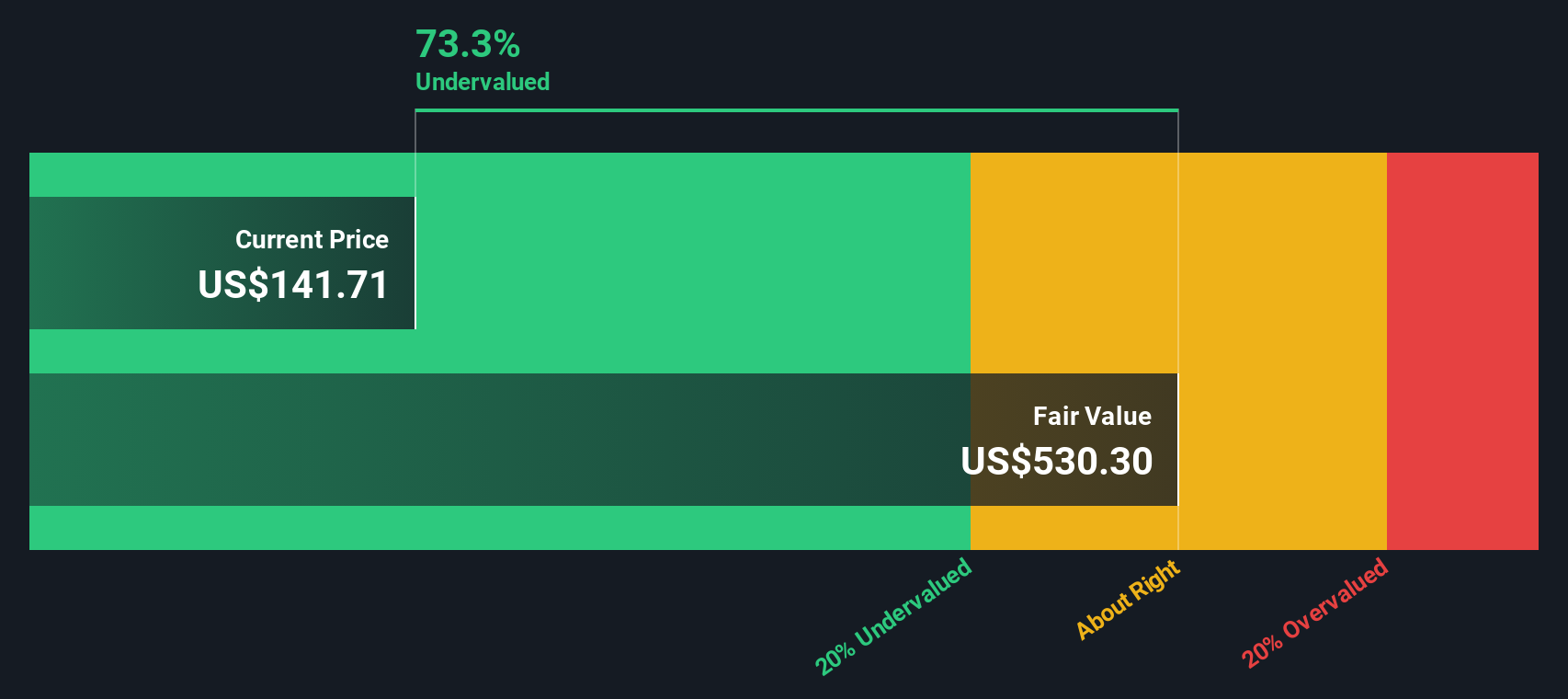

- On Simply Wall St's checklist, AerCap scores 5 out of 6 for being undervalued. This gives it a valuation score of 5. Next we will look at how different valuation methods line up for the stock, before circling back at the end to a broader way of thinking about its value story.

Approach 1: AerCap Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business might be worth today by projecting its future cash flows and discounting those back to a present value using a required rate of return.

For AerCap Holdings, the model used is a 2 Stage Free Cash Flow to Equity approach. On a last twelve month basis, the company reported free cash flow of about $819 million outflow. Looking ahead, analysts have an estimate of $1.96 billion in free cash flow for 2026, with further years projected by Simply Wall St using its own assumptions.

Those projections imply free cash flow of about $16.22 billion in 2035, with each future year discounted back to reflect risk and the time value of money. Adding these discounted cash flows together produces an estimated intrinsic value of about $530.30 per share.

Against a current share price around $141.84, the DCF output suggests the stock trades at roughly a 73.3% discount to that intrinsic value, which screens as materially undervalued on this model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests AerCap Holdings is undervalued by 73.3%. Track this in your watchlist or portfolio, or discover 887 more undervalued stocks based on cash flows.

Approach 2: AerCap Holdings Price vs Earnings

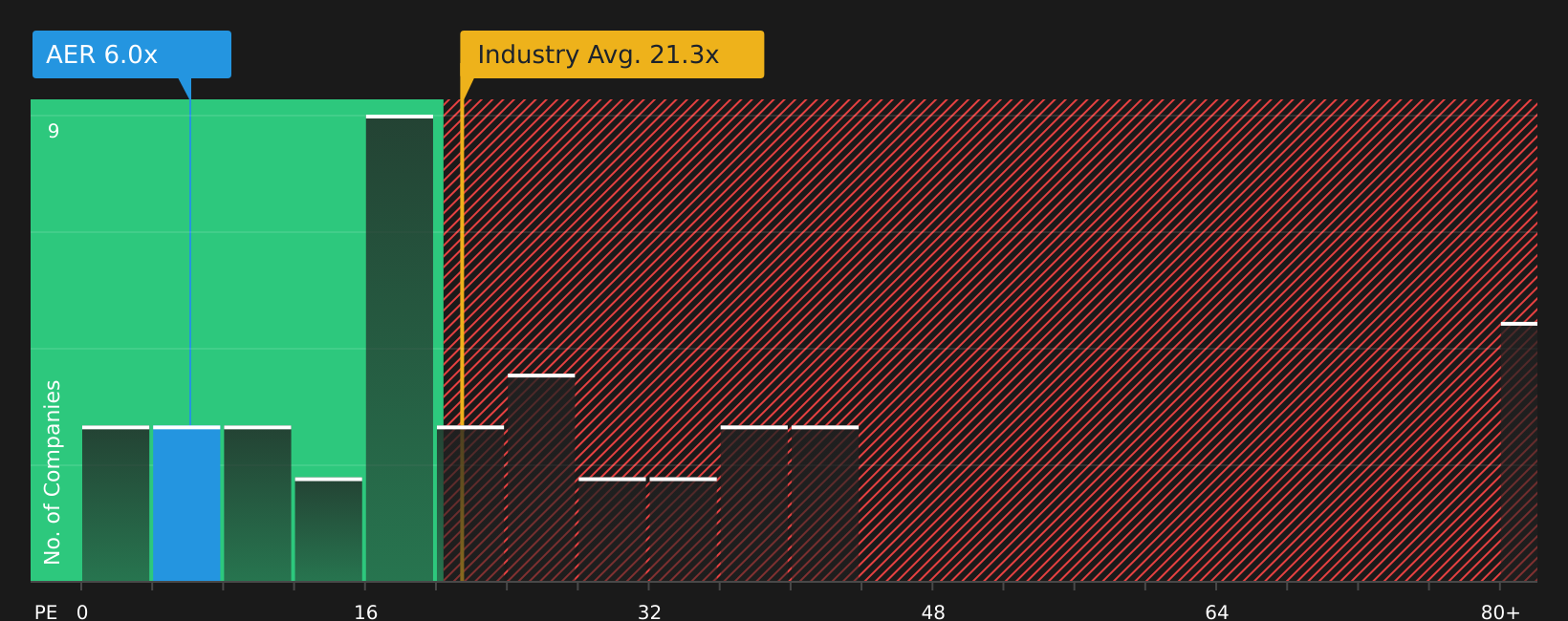

For a profitable company like AerCap Holdings, the P/E ratio is a straightforward way to connect what you pay per share with the earnings the business is currently generating. Investors typically look for a P/E that reflects both how fast earnings might grow and how much risk they are taking on, so higher growth or lower risk can justify a higher P/E, while slower growth or higher risk usually points to a lower “normal” range.

AerCap currently trades on a P/E of about 6.2x. That sits well below both the Trade Distributors industry average of roughly 22.2x and a peer group average of about 29.3x. Simply Wall St also calculates a “Fair Ratio” for AerCap of 11.0x. This is a proprietary estimate of what the P/E could look like given factors such as earnings growth, profit margins, industry, market cap and company specific risks.

Because the Fair Ratio incorporates those fundamentals, it can be more tailored than a simple comparison against broad industry or peer averages. Setting AerCap’s current 6.2x P/E against the 11.0x Fair Ratio suggests the shares are pricing in a lot of caution relative to that model.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1439 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your AerCap Holdings Narrative

Earlier we mentioned that there is an even better way to think about valuation. On Simply Wall St's Community page you can use Narratives, where you set out your story for AerCap Holdings, link that story to your own revenue, earnings and margin assumptions, and see how that flows through to a fair value that you can compare with the current price. This then updates automatically as new news or earnings arrive and can look very different from one investor to the next. For example, one AerCap narrative currently anchors on a fair value of about US$151 per share, while more cautious narratives sit closer to the current price, reflecting different views on aircraft supply, capital deployment and long term cash flows.

Do you think there's more to the story for AerCap Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.