Is AerCap Holdings (AER) Undervalued After Its Latest Aircraft Deliveries?

AerCap Holdings NV AER | 0.00 |

Recent aircraft deliveries put AerCap Holdings in focus

AerCap Holdings (AER) is back in the spotlight after announcing deliveries of new Airbus A321neo aircraft to Azerbaijan Airlines and GE powered Boeing 787-9 aircraft to Thai Airways.

These transactions highlight AerCap Holdings' role in supplying newer generation jets to airline customers that are updating fleets for efficiency and passenger appeal. For investors, the deliveries also provide a current reference point for evaluating the scale of AerCap's leasing platform and its relationships with major carriers.

Recent deliveries of Airbus A321neos and Boeing 787-9s come as AerCap Holdings trades at US$148.81, with a 30-day share price return of 6.76% and a 1-year total shareholder return of 28.44%, alongside a very large 5-year total shareholder return that signals sustained momentum.

If you are comparing AerCap Holdings with other opportunities in capital-heavy sectors, it can help to broaden the search and see what stands out in 20 top founder-led companies

With AerCap Holdings delivering new aircraft to airlines and the stock at US$148.81 after a 28.44% 1-year total return, investors may be asking whether AER is still undervalued or whether future growth is already priced in.

Most Popular Narrative: 10.1% Undervalued

The most followed narrative on AerCap Holdings pegs fair value at $165.50 per share versus the last close of $148.81, setting up a clear valuation gap for investors to assess.

Prudent capital allocation, supported by a strong balance sheet and ongoing deleveraging, positions AerCap to capture opportunities in sale leasebacks and organic fleet growth as OEM deliveries ramp up, driving revenue and earnings upside while containing interest expense.

Want to see what is sitting behind that fair value for AerCap Holdings? The narrative leans heavily on earnings power, margin reset, and a higher future earnings multiple. Curious which assumptions matter most and how they tie back to today’s share price? The full story joins those moving parts into one valuation view.

Result: Fair Value of $165.50 (UNDERVALUED)

However, AerCap Holdings' story can change quickly if aircraft supply shifts to oversupply or if key airline customers run into financial trouble that affects lease payments.

Another view on AerCap Holdings’ value

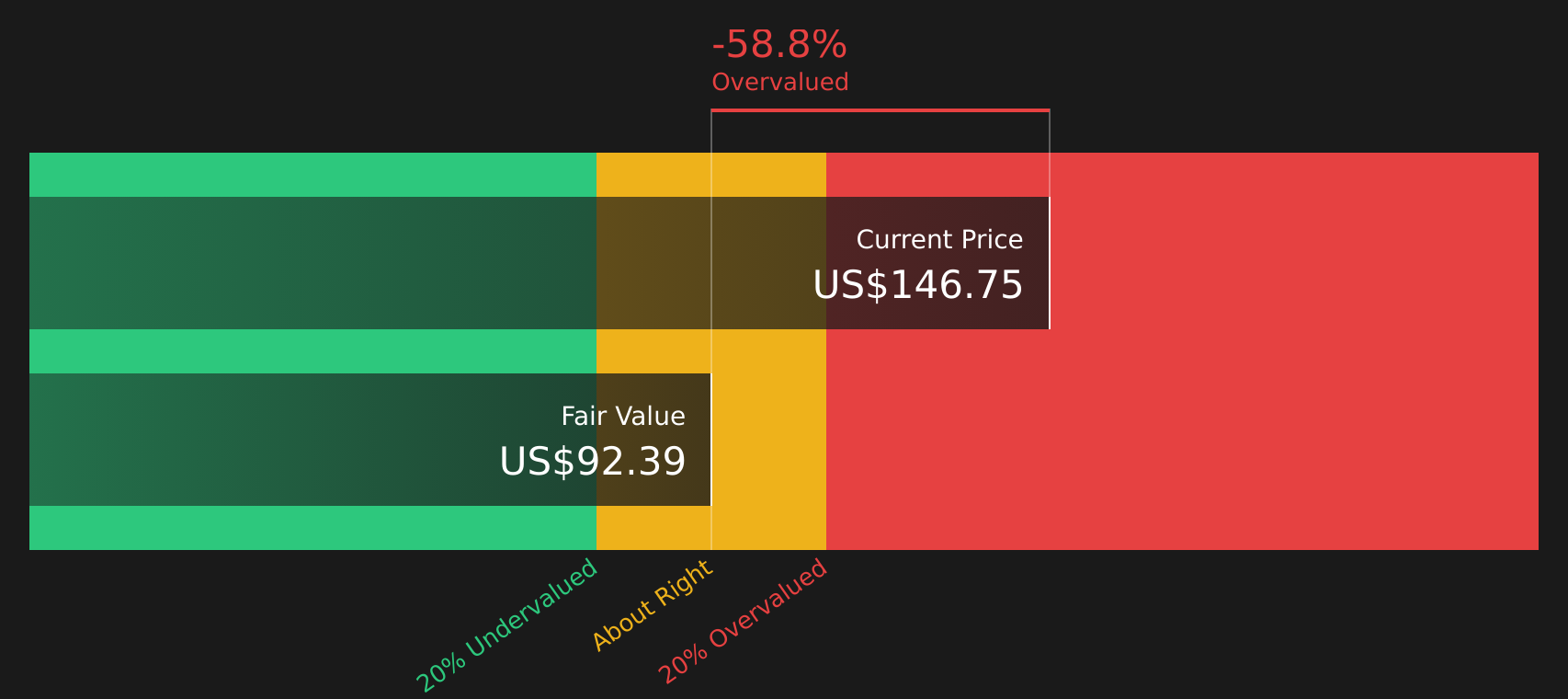

While the AerCap Holdings narrative points to a fair value of US$165.50 per share, the SWS DCF model presents a more cautious picture, with an estimate of US$92.53 per share that suggests the stock is trading well above its implied future cash flow value. Which story do you think fits AerCap best?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out AerCap Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals around AerCap Holdings leave you unsure, it can help to review the data directly and decide what matters most to you, including the 3 key rewards and 4 important warning signs.

Looking for more investment ideas beyond AerCap Holdings?

If AerCap Holdings has you thinking more broadly about opportunities, do not stop here. New ideas elsewhere could be the difference between a good portfolio and a great one.

- Target potential mispricings by scanning for companies that combine quality fundamentals with attractive valuations using the 44 high quality undervalued stocks.

- Strengthen your income stream by focusing on companies with higher yields and resilient payouts through the 8 dividend fortresses.

- Dial down portfolio risk by concentrating on businesses with sturdier profiles using the 70 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.